- Canaccord Genuity raises Coinbase target to $240, highlighting Q4 beat and positive ETF developments.

- Wedbush and Needham boost Coinbase targets to $200 and $220, citing robust earnings and alt-coin volume.

- See the 6X seasonal strategy set to target this fall’s biggest opportunities. Details here →

Wall Street analysts offered their takes on Coinbase Global Inc COIN post fourth-quarter beat. The stock price climbed following the analyst ratings.

Canaccord Genuity analyst Joseph Vafi maintained Coinbase with a Buy and raised the price target from $140 to $240.

On Thursday, Coinbase reported fourth-quarter revenue of $953.8 million, which beat the consensus of $822.4 million. The EPS of $0.51 beat the consensus loss of $(0.01).

The analyst stated that since Coinbase’s third-quarter report, the digital assets industry has seen significant developments, including the approval of spot BTC ETFs and a rise in cryptocurrency prices.

In the fourth and early first, Coinbase’s business model thrived amid increased volatility and trading volumes, expanding partnerships and achieving solid profitability, likely gaining market share, Vafi noted.

The launch of spot BTC ETFs in January, with Coinbase as the custodian partner for 8 of the 11 approved ETFs, is seen as a positive development despite potential competition for trading volumes, per the analyst.

This move, along with Coinbase’s market leadership and accounts with over a third of the most significant global hedge funds, is expected to drive momentum in its business.

Vafi projects first-quarter revenue of $981.99 million.

Wedbush analyst Moshe Katri maintained Coinbase with an Outperform and raised the price target from $180 to $200.

Katri said that Coinbase delivered results that significantly surpassed expectations, demonstrating the company’s robust earnings capability with over $14.00 in CEPS for the calendar year 2021.

These outcomes effectively counteract concerns raised about Coinbase, showing no significant fee compression since its IPO, no cannibalization from ETFs, a decrease in reliance on retail and trading fees alongside growth in Value-Added Services (VAS) and institutional engagement, and a more favorable legislative and regulatory climate.

Coinbase has seen positive flows from retail and institutional segments, benefiting from ETFs, expanded into 11 new markets—now covering approximately 70% of the global Total Addressable Market (TAM)—and is making progress in developing its derivatives trading, which constitutes 75% of all crypto trading.

Katri projects a first-quarter revenue of $955 million.

KeyBanc analyst Alex Markgraff reiterated a Sector Weight rating.

The analyst noted that the stronger-than-anticipated results were driven by an increase in transaction revenue due to higher volumes, a favorable mix, and a significant rise in subscription and services revenue, particularly from rewards, surpassing internal projections.

Transaction revenue through mid-February has run about 21% higher than the fourth quarter’s level, with subscription and services revenue forecasted to be about 19% higher at the midpoint for the first quarter of 2024, despite conservative estimates.

Markgraff projects first-quarter revenue of $1.08 billion.

Needham analyst John Todaro reiterated a Buy with a price target of $220, up from $180.

Alt-coin share of volume increased to the highest levels in fiscal 2023 at 71%, which assuages concerns that Coinbase is too reliant on BTC volume in an environment where low-cost BTC ETFs now exist, Todaro said. He does not expect fee compression in alt-coin trading.

Retail volume came in much more robust than the consensus expected while narrowly missing his estimate ($30 billion estimate vs. $29 billion actual), indicating retail quickly bounced back as crypto prices increased in the fourth quarter. Todaro projects a first-quarter revenue of $1.2 billion.

Oppenheimer analyst Owen Lau had an Outperform rating and a price target of $200. He projects a first-quarter revenue of $1.01 billion.

With several catalysts ahead, including further adoption of spot Bitcoin, Lau noted that ETF, halving, potential approval of ether ETF, Fed’s rate cut, and resolution of the SEC lawsuit, COIN can improve its fundamentals and deliver profitability over the next two years, barring a macro downturn and lumpy mark-to-market treatment.

Goldman Sachs analyst Will Nance maintained a Sell rating with a price target of $170, up from $124.

Shares have outperformed, a trend Nance finds justified due to the significant increase in retail volume and improved trading revenue dynamics, likely to influence future projections positively.

Consequently, he adjusted his revenue and EBITDA forecasts upwards to align with the current market environment and the dynamics between retail volume and take rate, which were uncertain before this quarter.

Management’s focus on crypto payments in 2024 is promising for widespread crypto adoption, which he noted as a credible long-term use case.

Coinbase has shown commendable execution on several product initiatives, including supporting 8 of the 11 BTC ETFs, expanding its Coinbase Prime product, and scaling its Base ledger and derivatives platform.

However, the analyst noted market conditions, such as crypto prices and volatility, will be the primary drivers of Coinbase’s performance, with broader use cases emerging more gradually.

In the long term, Coinbase stands to benefit significantly from broader crypto adoption, with its global presence, scale, and commitment to compliance positioning it to gain market share within the crypto ecosystem.

JP Morgan analyst Kenneth B. Worthington upgraded to a Neutral rating with a price target of $95, up from $80.

The re-rating reflected the ecosystems’ price appreciation and more positive ETF flows. Worthington projects a first-quarter revenue of $1.08 billion.

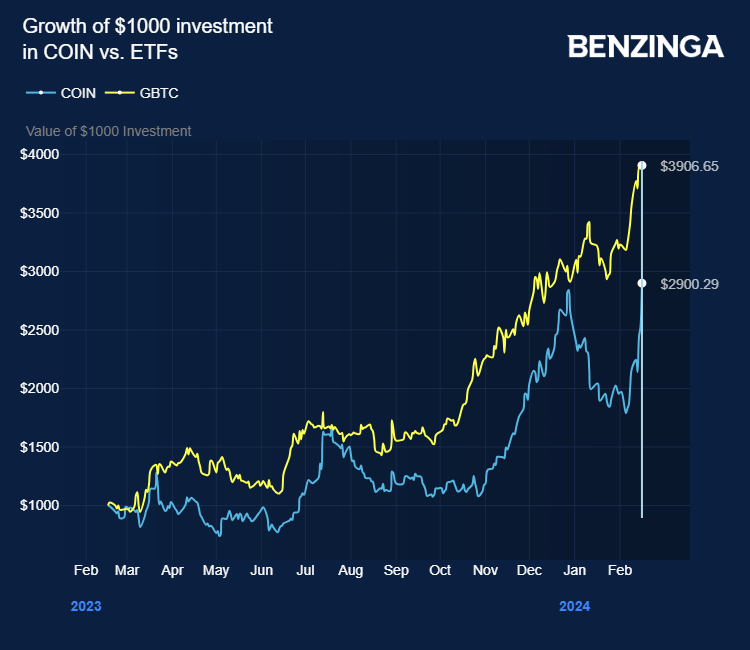

Price Action: COIN shares traded higher by 13.70% at $188.35 on the last check Friday.

Photo via Company

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.