The global economy has been hard hit by coronavirus lockdowns and Russia is no exception. The International Monetary Fund forecasts a 5.5% contraction of Russia’s growth in 2020, which would be the economy’s worst performance since the 7.8% contraction in 2009.

Unlike the downturns that came on the heels of oil price declines in 2008-09 and 2014-15, this time around Russia’s central bank is reacting in a very different manner. In 2009 and 2015, the ruble plunged alongside oil prices. As the currency weakened, inflation picked up and the Central Bank of the Russian Federation (known as the Bank of Russia) raised short-term borrowing costs significantly in order to bring inflation back down. This time, however, the Bank of Russia is cutting interest rates and might, on Friday June 19, cut its official rate to a post-Soviet record low (Figure 1).

Trending Investment Opportunities

Figure 1: Unlike the last two downturns, this time Russia’s central bank has been cutting rates

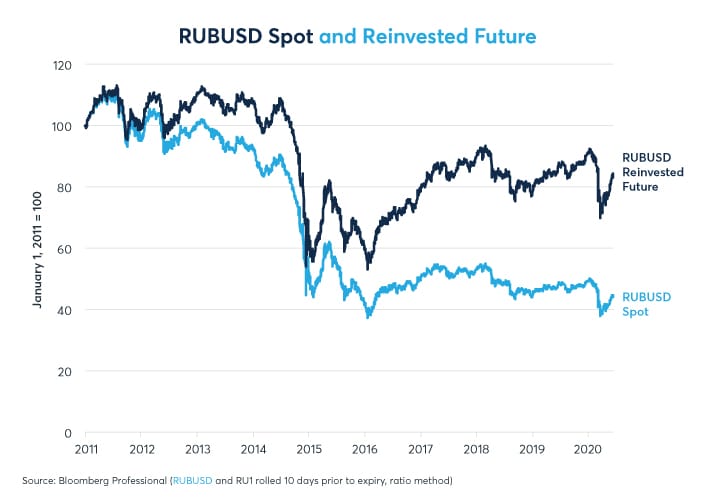

Russia’s central bank has been able to cut rates largely because the ruble (RUB) has been much more stable in the face of weaker growth this time around than in the past. During the 2008 global financial crisis, RUB fell by 37% versus the US dollar (USD). During the 2014-16 oil price rout, the ruble fell by 61% versus USD. So far in 2020, the peak-to-trough selloff in RUBUSD amounted to 26.5% and RUB has since rebounded sharply. As of June 11, it was only 12% below its recent January 15, 2020 peak. Indeed, in recent years, RUB has shown much less reaction to changes in commodity prices than it has in the past (Figure 2).

Figure 2: RUBUSD hasn’t fallen as much as the commodity price decline might have suggested it would

Part of the ruble’s recent resilience stems from the nature of the global crisis itself. In 2014-16, the global economy was doing relatively well except for commodity producers, especially oil exporters. By contrast, in 2020, everyone seems to in the same boat. Thus, the problems afflicting the Russian economy in 2020 mirror those in the US, Europe and elsewhere.

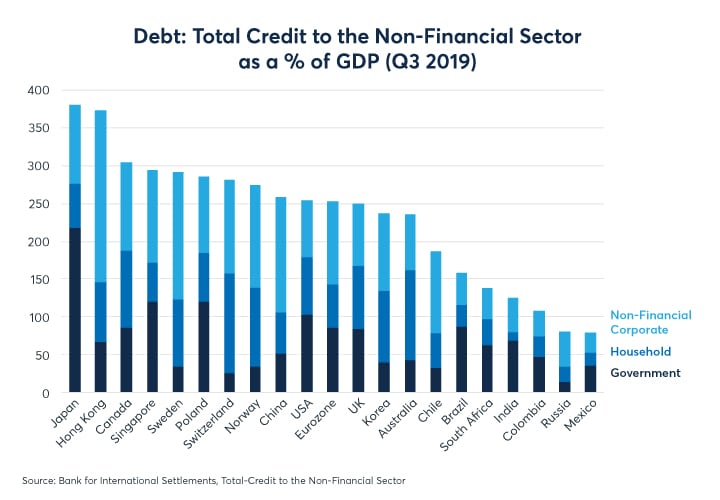

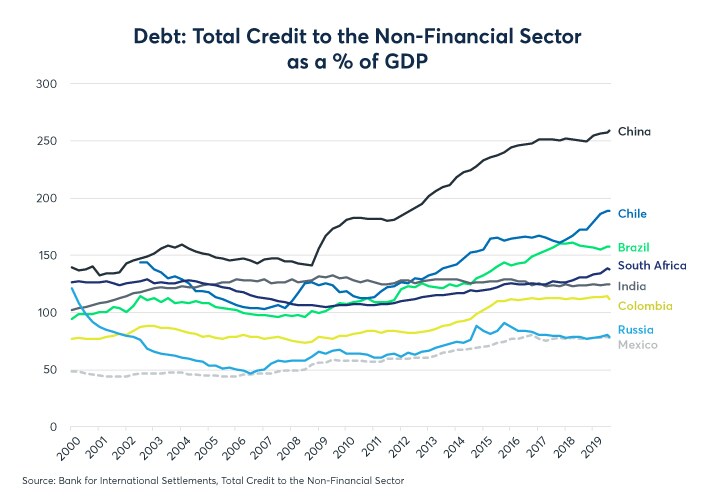

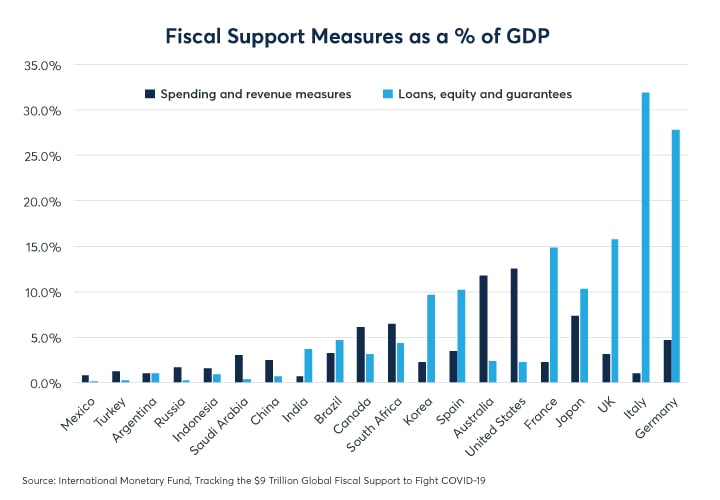

Additionally, in 2008, memories of Russia’s 1998 debt default were rekindled. When the global economy ran into trouble the last time, investors were quick to sell emerging market currencies as they did other risky assets. Investors spent little time differentiating one currency from another, including the ruble. In sharp contrast, memories of the 1998 Russian debt default have largely faded in 2020. While developed economies have loaded up on debt during the past two decades, Russia has steadily deleveraged and now, along with Mexico, has among the world’s lowest debt levels (Figure 3 and 4). Moreover, with Russia’s interest rates still far above zero, its central bank has the option to cut rates to stimulate growth. In many other economies where rates are stuck near zero, stimulus has taken the form of unprecedently large fiscal stimulus, something that Russia has largely avoided so far (Figure 5).

Figure 3: Russia is among the world’s least indebted countries

Figure 4: Russia is one of the few countries with a lower debt-to-GDP ratio in 2020 than in 2000

Figure 5: Zero-interest-rate countries have little choice other than to borrow more to boost growth

The paradox of debt and interest rates is that the more debt a country has, the more likely it has extremely low-interest rates. If one had an extremely simple model of interest rate markets, one might imagine that increasing debt supply would push down the price of debt and therefore push interest rates higher. However, as we demonstrated in our study of the debt paradox (see the article here), the opposite seems to be true. The more debt a nation has, the more likely it is to have extremely low-interest rates for the simple reason that low rates make it possible to cope with high debt burdens.

The COVID-19 pandemic has added a new dimension to this. Nearly all nations (and regions like the Eurozone) with high debt burdens have near-zero interest rates. Some, like the eurozone, Switzerland and Japan, even have negative interest rates. Although their central banks can use quantitative easing, yield curve targeting, forward guidance, buying of credit products and other measures to combat the economic downturn, monetary policy is of limited use. As such, many of the high-debt countries seemed to have reached the conclusion that the solution to the coronavirus downturn is more debt. Concern about ever higher debt levels may explain, in part, why the ruble and certain other emerging market currencies have been much more resilient so far in 2020 than they were in 2008-09.

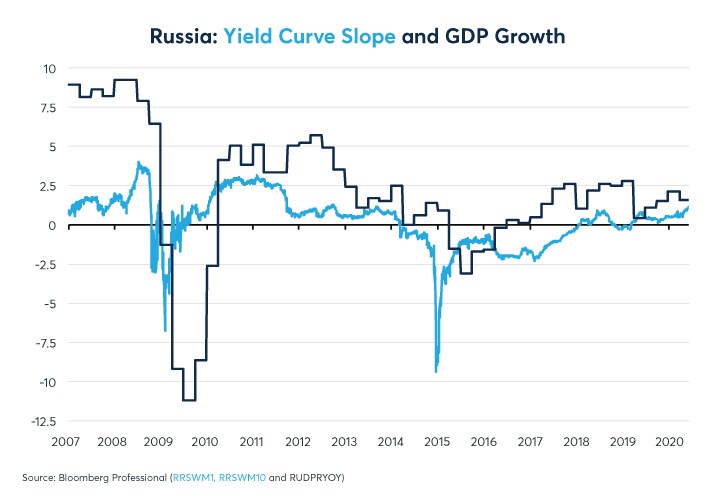

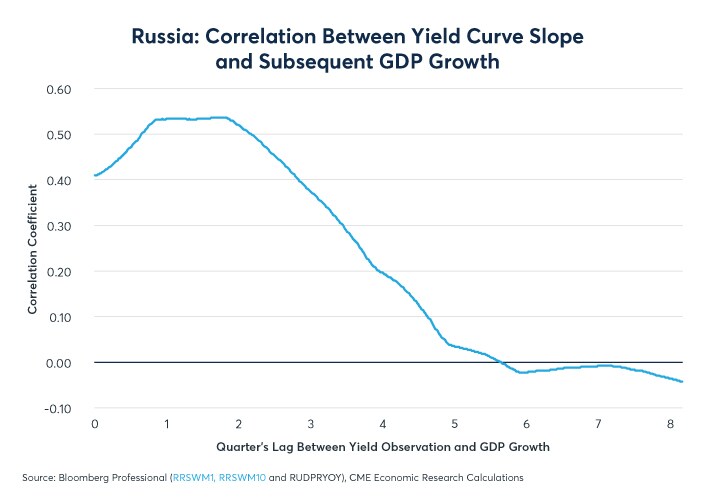

As Russia’s central bank cuts rates, it has been gradually steepening the yield curve. As of mid-June, Russia’s 1Y10Y yield curve was the steepest that is been since 2011, although with a 106 basis point (bps) spread between one-year and 10-year rates, it’s a long way from its steepest level ever (Figure 6). Depending upon the behavior of Russia’s long-term interest rates, further cuts to short-term rates might steepen the yield curve even more. If so, that would most likely be good news for the Russian economy. Over the past 13 years, there has been a strong positive correlation between the slope of Russia’s yield curve and subsequent GDP growth (Figure 7) – though, this time around, the course of the pandemic both in Russia, and globally, will play a big role as well.

Figure 6: Russia’s 1Y10Y yield curve is at its steepest since 2011

Figure 7: Over the past 13 years, yield curve slope has correlated positively with subsequent growth

Even with lower interest rates, depositors in Russia will enjoy about a 5% spread over depositors in the US and Europe. The cumulative impact of such interest rate gaps can become extremely large over time. For example, had one stuffed one hundred dollars’ worth of rubles in a sock in January 2011, those rubles would currently be worth about $44. By contrast, had one deposited $100 worth of rubles in a bank in Moscow in January 2011, with the accumulated interest, it would be worth about 82% as much as if one had placed the $100 in a US bank account (Figure 8). The more central banks cuts interest rates towards US and European levels, however, the smaller that buffer is likely to become. When it comes to rate cuts, Bank of Russia’s main limitation on cutting rates further may be continued low rates of inflation. So long as inflation doesn’t pick up and RUB remains relatively stable, the central bank may feel little need to tighten policy.

Figure 8: Accumulated interest rate differentials make a big difference to currency investors over time

Finally, Russia has so far spent about 2% of GDP on fiscal support aimed at fighting the impact of the coronavirus lockdowns. With public debt amounting to only 15.5% of GDP, the Russian government retains substantial borrowing capacity should it choose to deploy it.

Bottom Line

- Low inflation and a stable currency may allow for further rate cuts in Russia

- Russia has among the world’s lowest debt levels

- Positive interest rates allow Russia to stimulate growth with monetary rather than fiscal policy

- Watch Russia’s yield curve as an indicator how fast Russia’s recovery might be

To learn more about futures and options, go to Benzinga’s futures and options education resource.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.