Ten times — that's the average number of times an American worker will change employment during his lifetime. Are you close to that figure? You might even find yourself self-employed at one or several points during your working life. When one job ends and another begins, a new retirement plan does too.

If you have changed jobs often, you’ve likely accumulated several retirement packages throughout the years. If you haven’t already, consider consolidating those assets for better management and flexibility in financial strategy.

What Is An IRA/401(k)?

The Employee Retirement Income Security Act (ERISA) of 1974 was an incentive for individuals to establish individual retirement accounts (IRAs) on their own.

Corporations began the process of replacing costly defined benefit plans like pensions with 401(k) defined contribution plans. Tax-qualified accounts have since become safe harbors protected from the eroding tides of taxes on earnings.

As an incentive for individuals to establish retirement accounts on their own, deposits to ERISA qualified accounts are deductible from current income for tax purposes.

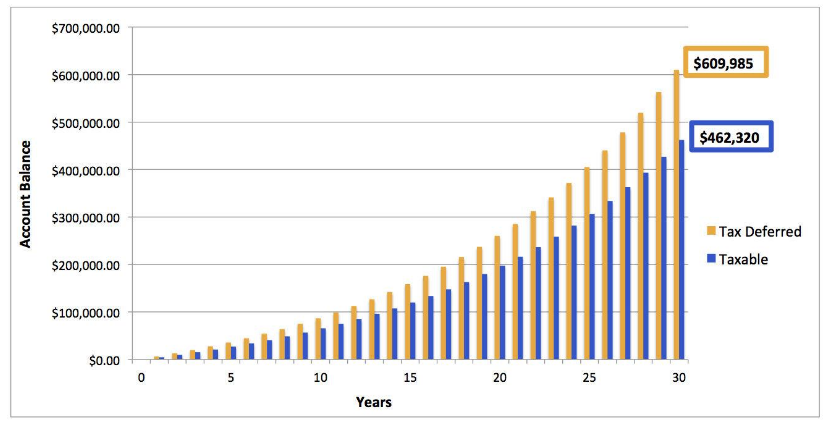

While tax-deductibility is a powerful incentive to fund a retirement account, by far the greatest benefit of ERISA-qualified accounts is the allowance for tax-deferred growth. Investment earnings are not taxed when the source of those earnings is held inside an ERISA-qualified account.

$3,000 per year @ 10%

What is an IRA Transfer?

There are two ways of moving retirement funds from one custodian to another — direct transfer or rollover of a distribution.

A transfer is easiest and quickest if that option is available. A transfer occurs between two similarly registered qualified retirement accounts. Assets held in a brokerage account are easily transferred to another brokerage account.

Transferred assets move directly from one custodian to another via ACATS without ever leaving a tax-qualified account. Bank-to-bank transfers can be efficient because the sender and receiver are regulated by the same government agency and can only hold assets insured by the Federal Deposit Insurance Corporation (FDIC).

What is an IRA Rollover?

Retirement assets held in a corporate retirement plan like a 401(k) cannot be transferred, and so must be withdrawn. A payout from a qualified account is called a distribution and must be re-deposited or “rolled over” into another ERISA-qualified account within 60 days to avoid a tax penalty.

If you’re younger than 59½ and you take the funds out of your account, you’ll be penalized 10% on top of ordinary income taxes. That 60 days could be used to fund a short term need such as a real estate transaction or mortgage refinance. Rollover assets can also be split between receiving accounts or re-deposited at different times as long as the account holder has documentation.

How to Initiate a Transfer

Whether retirement funds can be moved between qualified accounts depends on what the assets are and where the assets are being held. IRAs at brokerage firms and banks can be moved via direct electronic transfer.

The receiving firm, at your signed request, initiates the transfer and takes responsibility for following up on its progress. Transfers are often delayed when the receiving firm cannot hold assets to be sent and forces liquidation.

For that reason, select the receiving firm wisely.The chosen firm will provide, either online or in-person, a standard ACATS transfer form. The account holder must sign for the transfer and provide a recent account statement. A direct transfer of an IRA can take two weeks to one month. When the transfer is complete, it will appear on your statement.

How to Initiate a Rollover

Distribution must be rolled over within 60 days, but the time of response by an ex-employer’s benefits department will vary by company.

The two-step rollover process begins when you contact your employer’s benefits department, retirement plan administrator or investments manager. With the paperwork particular to that company, the account holder must ask for a total distribution and that no taxes be withheld.

The retirement account holder will then have 60 days from the date on the check to re-deposit to another ERISA qualified account. The IRS will report the amount of that distribution to the retirement account holder on form 1099-R.The tax preparer reports that amount on line 15a of IRS form 1040 and then enters zeroes on line 15b as the taxable amount of that distribution.

Comparing Rollovers and Transfers

| Action | Contact | Responsibility | Reason | Paperwork | Timeframe | Contact |

Direct Transfer |

| Receiving firm | IRA to IRA | Receiving firm via ACATS | Two weeks to one month | Receiving firm |

Distribution Rollover |

| Sending firm and account holder |

| Proprietary to sending firm | Maximum 60 days | Sending firm |

Final Thoughts

Statistically, it’s likely that you’re not saving enough for retirement, nor did you start your retirement savings early enough.

You must fully take advantage of tax-deferral to the maximum extent available. Take the deduction from this year’s taxes, defer taxes on invested funds for decades, rollover or transfer for as long as possible without paying income taxes, pay income taxes only when necessary and especially when the individual’s rate is lower.

Want to learn more about retirement planning? Check out Benzinga's guides to the best places to rollover your 401k, the best individual retirement accounts and the best roth IRAs.