If you’ve just found out that someone has bequeathed you a home or another type of inheritance, it’s time to also learn what it can mean for your responsibility as a taxpayer.

If you've recently lost a loved one or are helping someone who has, we recognize this can be a challenging time. Understanding the process and getting organized are important first steps.

What’s the Inheritance Tax?

Inheritance tax is a tax that beneficiaries need to pay on assets bequeathed to them upon the death of the owner of those assets. The decedent could be a spouse, parent, sibling, friend, relative, a loved one or even an unknown person or entity. In most cases, if you receive an inheritance, you’ll likely be subject to an inheritance tax. However, there are exceptions to the rule.

The tax implications of inheritance are different from a windfall you might receive — for instance, taxes are different on a sizable bonus or a Powerball win. For tax purposes, the government considers those as ordinary income, and you may owe federal, state and local income tax on your earnings. Inheritance is not income, and therefore not subject to income tax.

The inheritance tax is also different from the estate tax because payment of the latter comes from the deceased’s estate before any disbursements are made to beneficiaries of the estate. Inheritance taxes, on the other hand, are due upon receipt of the inheritance by individual beneficiaries and calculated on the value of the assets bequeathed to each beneficiary.

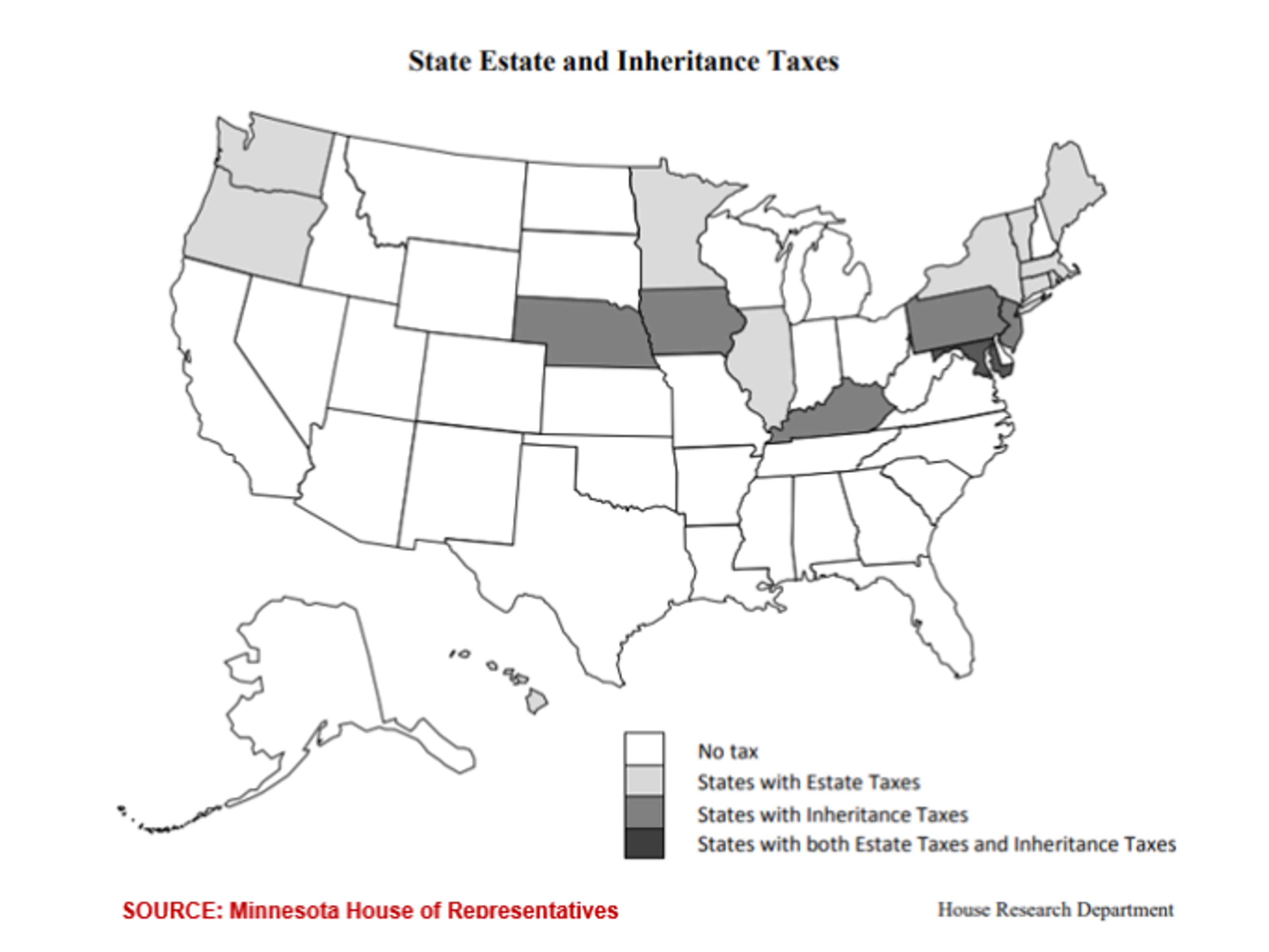

Which States have the Inheritance Tax?

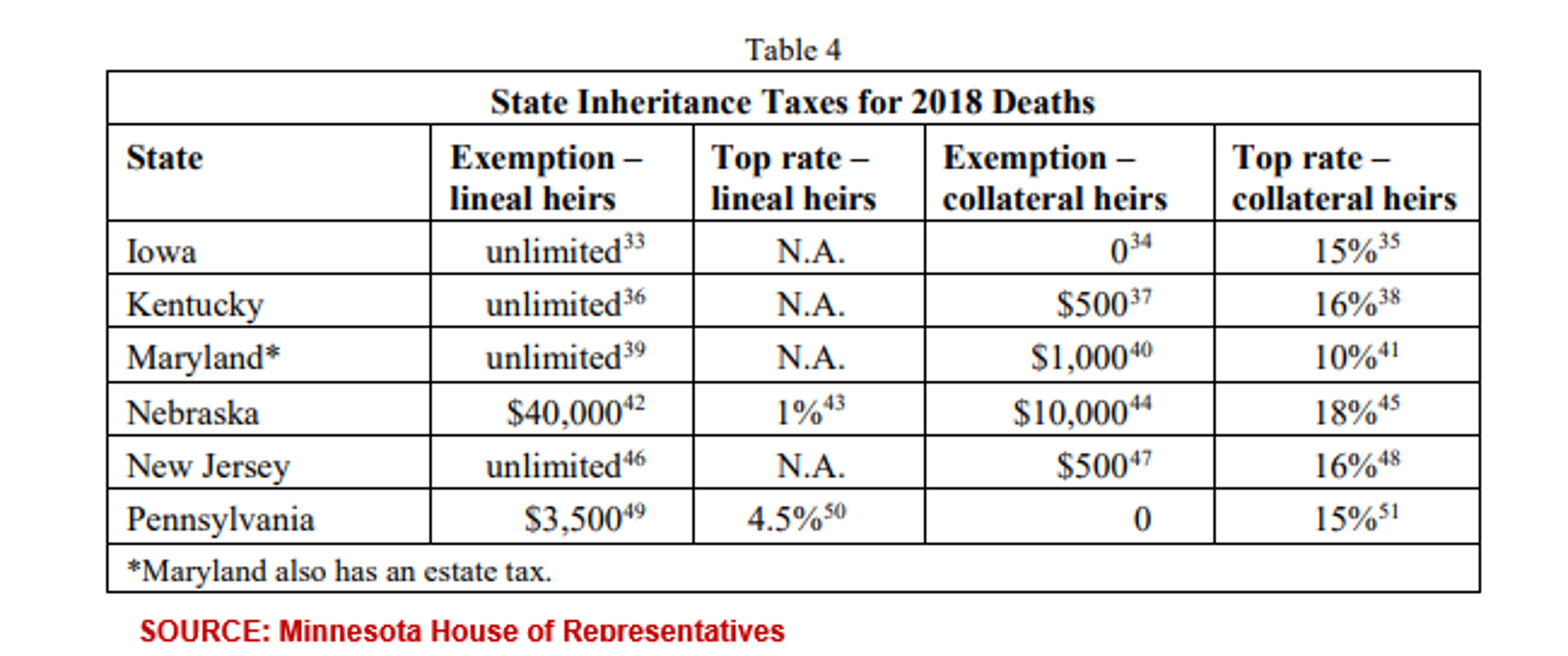

Eleven states had an inheritance tax in 2001. Since then, five of those states (Connecticut, Indiana, Louisiana, New Hampshire and Tennessee) have repealed their inheritance tax statues. Only six states impose an inheritance tax, and one — Maryland — levies both estate as well as inheritance tax.

Among the six states that do have an inheritance tax, the applicable tax rates differ. There are also inter-state differences with respect to exemptions granted to lineal heirs and collateral heirs. Even where states might have similarities in how they exempt specific classes of beneficiaries (for instance, siblings) each state may apply different standards to whether such exemptions should also extend to the spouses of those heirs.

How Much is the Inheritance Tax?

The rate of inheritance tax differs from state to state and may vary based on the amount of the inheritance, decedent’s resident status (resident or nonresident) and the beneficiary’s class (spouse, sibling, religious institution, qualified charity, etc.).

Typically, lineal heirs (children, grandchildren and parents) are either exempt from the tax or have a lower tax rate than collateral heirs (cousins, aunts, uncles, nephews, nieces

Here are a few quick facts:

- Each state has different tax classes applicable to various types of beneficiaries.

- States also differ in how they treat the same type of beneficiary. For instance, one state might exempt or have a lower rate for a sibling compared to another.

- Surviving spouses are exempt from paying inheritance tax in all six states.

- Some states may offer unlimited exemptions to some beneficiaries, and only limited exemptions for others.

- The top tax rate for lineal heirs ranges between 1% and 4.5%.

- The top rate for collateral heirs ranges from 10% to 18%.

These differences have an impact on how the amount of inheritance tax paid by a beneficiary. For instance, the state of New Jersey exempts the first $25,000 of an inheritance by the sibling (Class C) of a decedent, while Iowa offers no such exemptions for sibling (Class B) inheritance. An Iowa resident inheriting up to $25,000 from a sibling will pay tax amounting to $625 + 6% of amounts exceeding $12,500.

While it is the responsibility of the beneficiary to ensure that you pay your share of the inheritance tax owed, sometimes the estate of the deceased picks up the tab. Because the inheritance tax can sometimes be substantial, some individuals and families make provisions for dealing with the tax in their wills so they don’t burden their beneficiaries.

Inheritance Tax Filing Tips

The federal government does not have an inheritance tax, but each of the six states that do impose it have different state inheritance laws that govern how the tax is determined, calculated and paid. If you have received an inheritance or are responsible for filing taxes on behalf of a deceased benefactor, here are some tips that may help you:

Tip 1: Get Your Paperwork Together

Before you file your taxes following an inheritance, make sure you have all the paperwork related to any of the following income that the final returns of your benefactor did not cover:

- Employee compensation

- Benefit plan distributions

- Bonuses

- Partnership income

- Gain on disposal of inherited assets (including stocks and property)

- Royalties

- Interest and dividends on stocks and bonds

Although the actual assets might not be taxable unless they exceed the exemption limits specified by your state inheritance tax laws, you need this documentation so you can properly report all income received on inherited assets subsequent to receiving the inheritance.

If you have received an inheritance, some of the best tax software tools have features that can help you guide when you file your taxes.

Tip 2: Figure Out the Best Way to File

Generally, it’s the responsibility of the executor of your benefactor’s will who must file taxes on behalf of the deceased. However, where no such person exists (for example, there may be no executor appointed to oversee the distribution of the inheritance), the beneficiaries are responsible for filing those tax returns. You may even file as a surviving spouse or qualifying widow/widower.

Consult IRS Form 1041 for additional filing guidelines.

When filing your inheritance tax forms, there may be an opportunity for you to reduce the amount of tax you pay on inherited property that you disposed of. It all hinges on what you elect as the “basis” of the properties’ value. You could choose the fair market value (FMV) on the date of death of the decedent or choose an alternate method (elected in Form 706) that values the property six months post the date of death. Carefully weighing which “basis” to use could reduce your taxes significantly.

If you withdraw from your own as well as an inherited IRA, each of which has a separate “basis,” then you need to prepare two Form 8606s when filing your taxes. This will help you determine what portion of those distributions are taxable and which aren’t. As a beneficiary, you could potentially claim an estate tax deduction on distributions that you may have received from an inherited traditional IRA.

Another element you might need to be aware of is when dealing with Income In Respect of a Decedent (IRD). IRD refers to untaxed income which a decedent earned or had a right to receive during his/her lifetime. IRD is taxed to the beneficiary that inherits this income.

If you’ve never prepared your own taxes before, it might be a good idea to learn what’s involved in filing taxes before you proceed.

Tip 3: Understand Other Credits and Deductions

Most states exclude inheritances of up to a certain amount from the inheritance tax. Before filing your taxes, make sure you are aware of the exemption limits applicable for your state.

If you inherit assets from an IRA account, you don’t pay any taxes until you withdraw the money. Since those withdrawals are “other” income for your tax determination, you can offset that income against other eligible credits and deductions.

If you sell an inherited property for gain, that appreciation is taxable as capital gains. However, you can deduct selling expenses, such as realtor’s commissions and listing fees, from your gains.

Tip 4: Prepare Your Estate the Right Way

If you plan to leave an inheritance to someone, a great tax-effective way to deal with such transfers is through a trust structure. Putting assets from your estate into trust allows them to pass on to beneficiaries without probate-related taxes and expenditures.

If you hold assets such as a cottage or family home in joint ownership with a child or sibling, the death of one owner can trigger a massive capital gains tax for the beneficiary, especially if the owners held it over a long period of time. Revocable trusts might be a better vehicle to house such assets.

If you have a sizable estate that you intend your beneficiaries to inherit upon your passing, it might be more tax-efficient to give away some of the intended inheritance while you are still living. There is a fixed amount that you can gift to your future beneficiaries — the threshold is $15,000 per individual each year.

By giving away some of your estate during your lifetime, you not only get to see your loved ones enjoy part of your estate, it also reduces the overall value of your estate, which can subsequently reduce estate and inheritance taxes upon your passing.

Beware of “Tax-Free” Inheritance

One final word of caution for beneficiaries who live in states without an inheritance tax, or who are exempt from paying the tax under their states’ inheritance tax laws: Your inheritance might still come with a tax tab attached!

While the inheritance comes to you with no strings attached, any income or earnings such as dividends, interest, rental income etc. from such tax-free inheritance is taxable, both at state and federal levels. Additionally, if you decide to dispose of the inheritance (shares in a publicly-traded company or real estate), the proceeds received might also be subject to capital gains taxes.

If your state imposes an inheritance tax, it might be advisable to learn how to file state taxes before filing your tax returns this year.