HSA? HMO? PPO? Signing up for health insurance is difficult if you don't know the terminology or understand the different types of plans. We’ve created a simple step-by-step guide that will teach you how to get health insurance. Learn how to choose and purchase the right plan and get more important information on how health insurance works.

How To Get Health Insurance

Step 1: Enroll in Your Employer’s Sponsored Health Care Plan

If your employer offers health insurance coverage, your first stop on the road to enrollment should be your HR department.

Most employers provide coverage to full-time employees and many also cover a large percentage of premium costs – some employers even cover the entirety of their employee’s premium as long as they maintain full-time employment status.

If you have insurance available through your employer but you’d still like to search for an alternative plan, you may do so, but outside plans will usually be much more expensive because you will be required to pay the entirety of your premium.

Step 2: Wait for a Period of Open Enrollment or Consider Applying for Special Enrollment

If you do not have access to health insurance through your employer, you will have to wait until the end-of-the-year open enrollment period to secure coverage through the Affordable Care Act.

You can browse specific plans available on the marketplace when open enrollment begins, but until then, researching the differences between network types can be a useful first step to help you enroll more quickly when the period opens.

There are a few special circumstances that can allow you to enroll outside of the standard open enrollment period. If you’ve recently lost your job, have had a baby, someone in your household has died or you’ve gotten married or divorced, you may qualify for special enrollment.

To apply or learn more, visit HealthCare.gov and complete an application.

Step 3: Visit the Marketplace to View Your Specific Plan Options

Once open enrollment begins, visit HealthCare.gov and enter your zip code to be redirected to your state’s site or to view the federal marketplace.

The marketplace will show you a complete list of plans available in your area and you can apply for enrollment directly through HealthCare.gov. You’ll want to carefully consider which plan type is best for you and your family.

If you live in an urban area, you may be able to save costs by choosing an EPO if the EPO’s network extends throughout your city. If you live in a more rural area or you must travel long distances to see your health care providers, a PPO can offer you a larger network and broadens your options for providers who take your insurance plan.

If you don’t mind having your primary care physician choose specialists on your behalf, an HMO plan can be an affordable option. If you already have a primary care physician and you’d like to keep seeing him or her, make sure to call to ask what insurance plans he/she accepts – you don’t want to enroll in a new plan only to find out that your doctor is out of network.

Overview: How Does Health Insurance Work?

The cost of healthcare and medical treatment is very high in the United States. Health insurance helps to protect you from the financial ruin that can come with getting adequate healthcare in America, especially with chronic or severe illness or accidents and injuries.

The 3 terms you need to remember when finding the right health insurance plan are:

- Deductible,

- Coinsurance percentage

- Out-of-pocket limit.

A deductible is the amount of money you’ll to pay each year toward your medical bills before your insurance “kicks in” and starts to pay. For example, if you come out of the emergency room with a $10,000 bill and your deductible is $1,000, you would pay $1,000 and your insurance provider would cover the remaining amount.

After you’ve reached your deductible, you’re only responsible for paying your coinsurance, which is a percentage of the total cost of treatment. For example, let’s say you’ve reached your deductible and your emergency room bill equals $10,000. If your plan has a 5% coinsurance agreement, you’ll be required to pay 5% of $10,000 while your insurance provider covers the remainder.

You will pay your coinsurance percentage until you reach your out-of-pocket limit, which is the limitation on the total amount of money you’ll have to pay towards your medical care. Once you’ve exhausted your annual out-of-pocket limit, your insurance will cover 100% of your medical expenses.

Your health insurance plan may have limited coverage for certain expenses, and your employer may offer you dental insurance and vision insurance or benefits to fill in these gaps. If your employer does not cover your insurance, you can also purchase independent dental and vision packages.

What to Consider Before You Get a Policy

There are multiple types of health insurance plans. Some of the most common include:

Health Maintenance Organization Plans (HMOs)

HMO plans are the most common type of health insurance plan. HMO plans limit coverage to certain health care providers who work for or are contracted by the organization issuing the plan except in the event of an emergency.

HMO plan providers usually require you to live or work within a specific jurisdiction to maintain coverage. Some HMO plans require that you get a referral from your primary care provider before seeking treatment from a specialist.

Preferred Provider Organization Plans (PPOs)

PPO plans offer more flexibility than HMO plans. PPOs still have networks of preferred providers (and you’ll pay less if you use a preferred provider) but they also offer fewer restrictions on seeing out-of-network health care providers.

The best health insurance plans are usually PPO plans because they provide more flexibility when it comes to choosing your care providers, though premiums are usually higher when compared with HMOs and other types of plans.

Exclusive provider organization plans (EPOs)

EPO plans completely limit usage to physicians, specialists, and hospitals within the plan’s network except in the event of an emergency. EPO plans are common employee plans for health care and hospital employees.

Catastrophic Plans

Catastrophic plans are a special type of health insurance plan exclusively available to men and women under the age of 30.

Catastrophic plans usually cover preventive screenings and vaccinations but have extremely high coinsurance rates and usually only kick in in the event of a very costly accident or the onset of a sudden and serious medical condition. Catastrophic plans can be useful if you’re just getting started in your career and are relatively healthy.

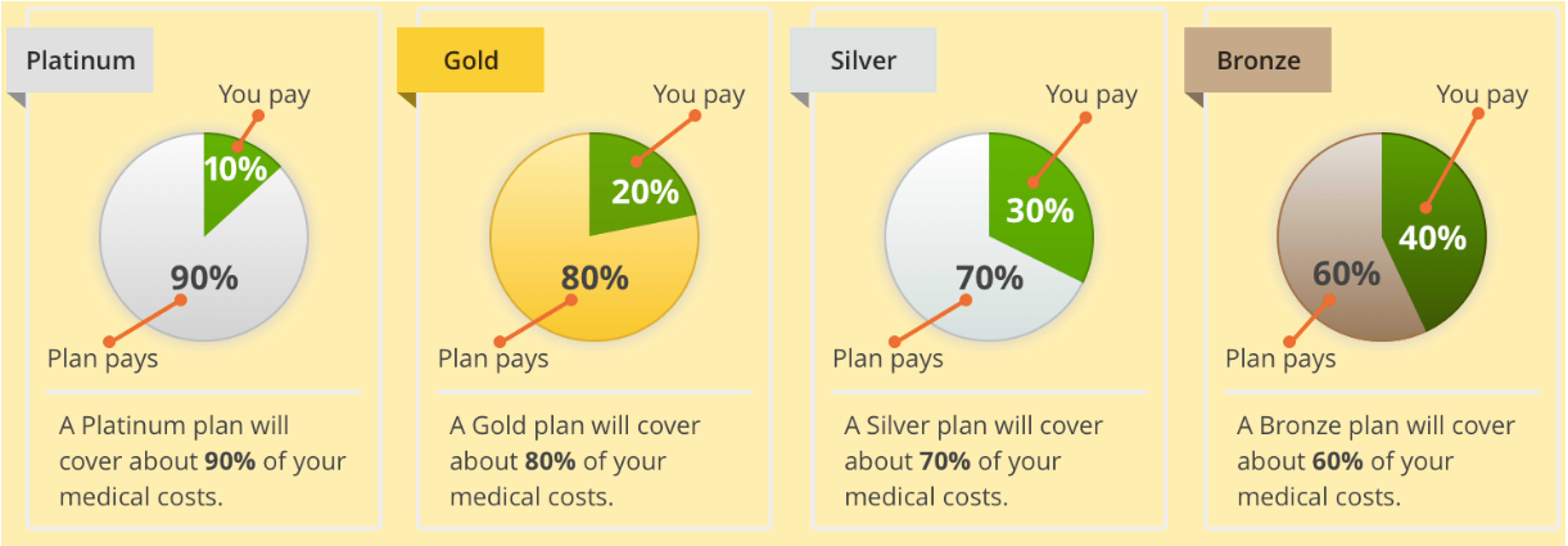

In addition to the multiple types of health insurance networks, there are also four unique tiers usually offered by each network. The Affordable Care Act (ACA) also classifies plans by metal tiers. Tiered plans include:

- Platinum: Platinum plans typically cover about 90% of your medical costs with a 10% coinsurance percentage.

- Gold: Gold plans typically cover 80% of your medical costs with a 20% coinsurance percentage.

- Silver: Silver plans typically cover 70% of your medical costs with a 30% coinsurance percentage.

- Bronze: Bronze plans typically cover 60% of your medical costs with a 40% coinsurance percentage.

As a general rule, the lower the coinsurance percentage, the more you will be expected to pay in monthly premiums and vice-versa.

Are Parents Required to Provide Health Insurance Until Age 26?

Under the ACA, you are allowed to stay on your parents’ health insurance until you turn 26. If you are under the age of 26 and you do not have health insurance available to you through your employer, chances are that you are still covered by your parents’ plan.

If you are on your parents’ insurance and you have insurance through your employer, your work insurance is your primary insurance and your parents’ insurance is your secondary insurance until you turn 26. You can enroll in an ACA-sponsored plan only during open enrollment dates.

If you do not have insurance available through your employer or your parents, you can enroll in a plan under the Consolidated Omnibus Budget Reconciliation Act (COBRA), a subsection of the ACA. However, you can only purchase a COBRA plan during periods of open enrollment except in extenuating circumstances.

Remember, too, some children (even as young adults) may obtain employment that allows them to purchase employer-sponsored health insurance and remove themselves from their parents’ coverage. At the same time, adult children 26 and under may return to their parents’ health insurance when needed.

Final Steps to Health Insurance Coverage

Your current health situation and the needs of your family will largely dictate which type of plan is right for you.

Some health insurance plans cover a large percentage of the costs associated with pregnancy and delivery, and others offer comprehensive benefits for those who have special mental health needs.

Don’t be afraid to request a phone call with a representative from an insurance network you’re considering to make sure that the plan offers coverage for your most important health concerns.

Looking to learn more about health insurance? Check out Benzinga’s guides to the best health insurance companies, the best vision insurance companies and the best dental insurance companies.

Frequently Asked Questions

Is health insurance required?

The federal mandate has been lifted, but some state have enacted their own mandates. Consider Medicare if you cannot afford traditional insurance.

What does health insurance cover?

Health insurance covers routine care, preventative exams, emergency room visits, prescriptions and much more. Review your policy to learn exactly what your health insurance covers.

About Sarah Horvath

Sarah Horvath is a highly respected freelance senior copywriter specializing in insurance content. With a wealth of experience, she is recognized as one of the top insurance copywriters in the industry. Sarah’s expertise encompasses various aspects of insurance, including home warranties, life insurance, health insurance, and more. Her insightful articles and guides are regularly featured on major finance sites, providing invaluable information to readers seeking to navigate the complexities of insurance policies. Known for her clear, concise writing style and comprehensive understanding of insurance products, Sarah is dedicated to empowering individuals with the knowledge they need to make informed decisions about their insurance coverage.