A credit card can be an invaluable financial tool. It can help you make larger purchases without a handful of cash. A credit card can also help you budget more effectively and build up your credit portfolio.

You have to apply to be eligible for a credit card, but a credit card application isn’t as intimidating as it might seem. Follow our step-by-step guide to increase your approval chances as you apply for a credit card.

Why You Might Need a Credit Card

Credit Cards Are Safer than Carrying Cash

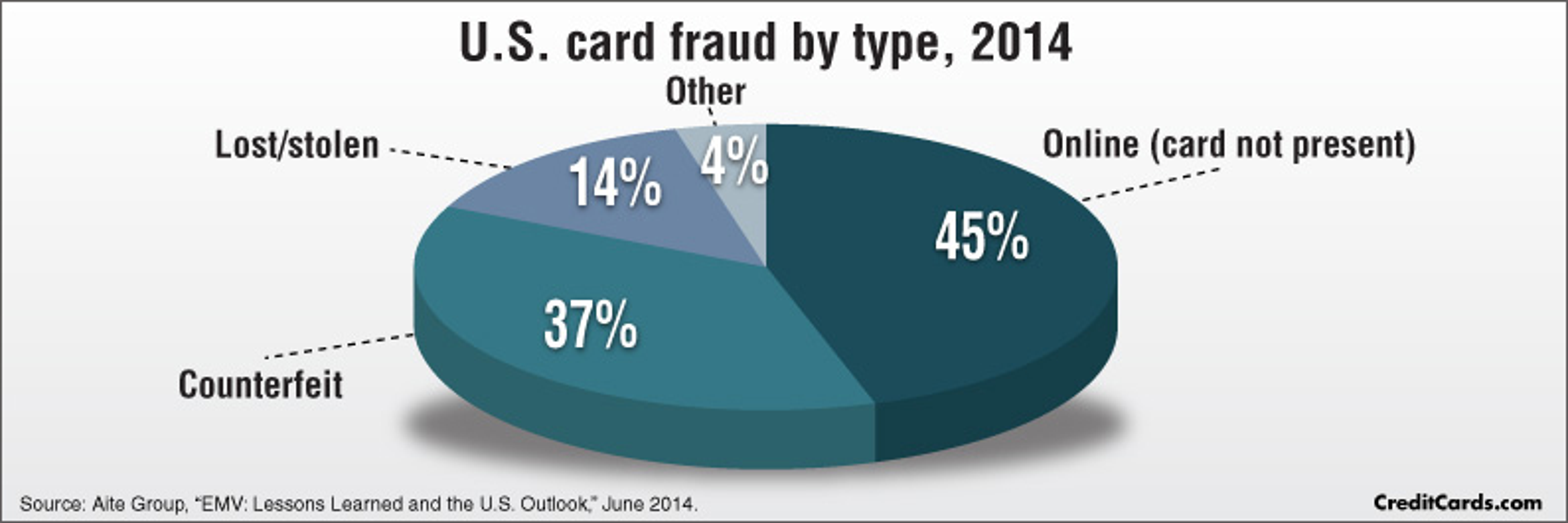

If you lose a stack of cash and someone else picks it up and decides to spend it, there is little you can do to recover your money. Credit cards, on the other hand, are much more difficult to steal and use. Credit card usage leaves a “paper trail” of charges police can use to track down the culprit.

And most credit card providers don't hold you liable for fraudulent charges to your account — if your card is stolen and used without your consent, your creditor will reverse the charges and get you your money back.

International travelers in particular are often advised to carry as little cash as possible and opt for credit cards instead.

Some Companies Require You to Pay with a Credit Card

Gone are the days of “cash only” signs in restaurants and clothing stores — today’s retailers are all about plastic. It eliminates the possibility of accepting counterfeit bills and allows consumers to buy the store’s products online.

Businesses that require a deposit or hold for damage (like hotels, hostels and car rental companies) typically only accept credit cards as payment.

Credit Cards Help You Build Credit

A consumer with no credit history is a total risk to lenders. Think of what you may want to purchase in the future. If you want to buy a house or a car, lenders will look into your credit history.

About 35% of your credit score is calculated using your payment history. Paying your credit card bills on time and in full every month raises your credit score and makes you a more appealing candidate for special offers and loan approval in the future.

What to Consider Before You Apply for a Credit Card

Your Current Credit Score

Consumers with bad credit or no credit can be a liability for a credit card company. If you have bad credit on your record, studies have shown that you are less likely to make payments on your cards.

If you have no credit, you are a total risk for the credit card company. No credit means there is no data to offer clues into your spending and repayment habits. It’s much less expensive for credit cards companies to refuse credit to those with shaky credit than it is to chase down payments, so don’t be surprised if your questionable credit gets in the way of your applications.

Luckily, a lack of credit or bad credit is not a permanent condition. You may qualify for a secured credit card, which is a special type of card that requires you to pay a deposit as collateral before your credit card company extends you a line of credit.

If you’re a college student, inquire about student credit cards, which are specifically designed with low lines of credit for young people who have not yet had the opportunity to build up the credit they’d need to be approved for a standard card.

Limit the Number of Credit Cards You Apply for

When you apply for a card, credit card companies will do something called a “hard inquiry” on your credit report. These show up on your credit report as inquiries. And if you have too many hard checks on your report, your credit score may suffer. Limit the number of credit cards that you apply for to avoid racking up too many hard inquiries on your account.

Some major banks may offer a pre-qualification process that runs a soft check on your credit to tell you if you’re likely to be approved or not before applying. Unlike hard checks, soft checks will not have an effect on your credit score. Ask about pre-qualification checks if you think that you might be denied by your creditor of choice.

You Can Build Credit Without Opening a Credit Card

If you’re only interested in opening a credit card to build your credit profile, know that there are plenty of other ways to build credit besides opening a credit card:

- You can become an authorized co-user on another person’s credit card without actually using the card.

- You can also take out and pay back a small personal loan from your bank or credit union.

- Contact your landlord and request that your rent payments be reported to the major credit bureaus.

How to Apply for a Credit Card

Step 1: Understand Your Current Credit Situation

The 1st step to finding the right credit card for your needs is to know your credit score and understand what’s on your credit report. You are entitled to one free pull of your credit report from each of the 3 major credit reporting bureaus once every 12 months.

Request and read your credit report thoroughly and make sure that there are no errors on your account that might lower your score. Know your credit score and where you fall on the spectrum. Credit card companies usually consider the classifications to be as follows:

If you have a good or excellent credit score, you'll have more options when it comes to credit card company selection, rewards, cash back, airline miles and more. You can also usually be approved more quickly and see lower interest rates compared to someone who has a lower credit score.

Step 2: Raise Your Credit Score

If you have bad credit, your credit card options will be limited. Take a few months to improve your score to help increase your chances of being approved and lower the interest rates you have to pay.

Some steps you can take to raise your credit score include:

- Keep a low balance on any credit cards you already have open. You may want to schedule automatic monthly minimum payments on your accounts so you don’t have to worry about forgetting when a bill is due.

- Continue making regular payments on your auto loan, student loan, mortgage or any other debts that you have. If possible, pay more than the minimum payment each month.

- Avoid closing open credit card lines, even if you don’t use them. Closing a credit card reduces your line of available credit, which can hurt your score. If the temptation of having the credit card is too much for you to avoid spending, put the card in a locked desk drawer where it’s out of sight or leave it with a trusted family member or friend.

- If you have fair credit and an account that’s new, your credit score will improve just as a matter of time; account age is responsible for about 15 percent of your credit score composition.

Looking for more tips on improving your credit score? Check out our new year’s guide to leaving bad credit behind.

Step 3: Compare Offers and Choose Where to Apply

Research credit card offers based on your credit score. Some of the factors you’ll want to consider when comparing credit cards include:

Interest Rates

Note that some creditors may provide low introductory interest rates that are only valid for a limited number of months after you open the card. After the introductory period is over, the interest rate may rise significantly. Be sure to ask a representative about the difference between introductory interest rates and standard APRs before you commit yourself to an application.

Rewards and Bonuses

From cash back to free airline miles to reward points, most major credit cards have unique loyalty systems. Compare a few reward systems and decide which bonuses appeal to you.

Annual Fees

Some credit cards charge an annual fee on top of interest payments, though many credit cards do not. Annual fees range from $50 to $500 depending on the benefits offered by the creditor.

International Fees

If you travel out of the country often, ask a representative about what types of fees are charged if the card is used while abroad.

After you’ve chosen the credit card that fits your needs, apply online or through your local bank or credit union. You must disclose information on your income, your Social Security number and your employment status on your application. Most companies now provide instant approval if you apply online but some may take between five and 10 days to offer you a decision.

Apply for Your Card Today

If your credit application is rejected, don’t give up hope! Most major banks and creditors allow their representatives to negotiate if an applicant is denied. If you have proof of income and documentation of a recent financial hardship (like an unexpected medical bill or a costly automobile collision), your creditor of choice might be willing to work with you by issuing you a secured credit card at first.

Though secured credit cards have strict spending limits when they are issued, they can become an unsecured card in as little as 6 months with regular on-time payments. Don't be intimidated by card applications. Narrow your list of desire cards, apply and use your credit card to your advantage today.

About Sarah Horvath

Sarah is an expert in the insurance, investing for retirement and cryptocurrency space.