For most, inflation is easily taken for granted as something with only a very relative impact on their everyday lives. Because the swells or dips in buying power don’t happen all at once, it’s hard to appreciate how severely those changes in the dollar strength impact everything from the cost of bread and employee wages to how funds or expenses are distributed through the economy.

But inflation does determine those things, and it holds more sway over everyday life than most would ever imagine. Unfortunately, a recent research report titled “Inflation and Its Impact on Real Estate” commissioned by Unison Investment Management, posits that the current measure of inflation might be significantly flawed, and homeowners, the middle class and the economy at large are paying for it.

What’s Real Estate Got To Do With It?

First, a primer on inflation:

Inflation is an increase in price of a good or service over a period of time, typically dictated by scarcity somewhere in market (excessive demand or limited supply). The U.S. government’s Bureau of Labor Statistics (BLS) aims to accurately measure the economy’s rate of inflation in order to guide monetary and fiscal policy to moderate its effects.

The BLS does this do this with the help of the Consumer Price Index (CPI), which is a measurement of the price of a group of basic goods and — this is the important bit — housing, which accounts for over 40 percent of the index. These figures are all weighted against factors like consumer income and wage growth as well as comparative measures like price changes in a basket of goods or other living expenses over time.

As a result, the CPI is ostensibly tailored to reflect and reinforce home value within an economic environment. That also means that real estate prices can move needle on inflation pretty substantially, which can have some alarming consequences if actual home values don’t match up to the rest of the CPI’s basket of goods.

According To My Calculations…

It’s this gap between how home value is calculated as a portion of CPI and the actual rate of inflation that the Unison report aims to address. Because, due to decades of shifting factors in the economy, the way the government calculates inflation has changed over the years. However, those changes have not always been made comprehensively enough to consistently reflect the actual rate of inflation.

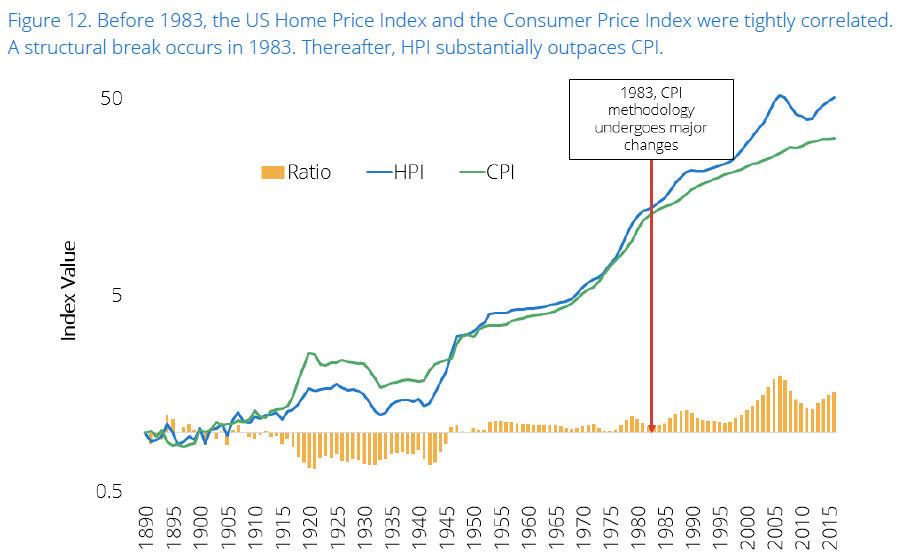

Basically, housing market inflation was first measured based on five factors (property taxes, insurance, maintenance and repairs, house prices, and mortgage interest costs). Because of inconsistencies primarily tied to the outsized influence of mortgage rates on the figure, the BLS changed their formula in 1983 to track housing inflation via Owners’ Equivalent Rent (OER), the amount a house is worth based on the rental value of comparable properties.

Essentially what this means is that the CPI now calculates housing value in terms of rental value rather than as an investment or a piece of equity. According to the report, while this provides a more stable read on the value of a home without the influence of extenuating or time-sensitive influences, it also skews the cost of real estate in terms of how property serves renters (as housing) rather than how it serves homeowners (as equity).

A Tale Of Two Indices

What this comes down to, and what the report aims to show, is that this 1983 change set off a divergence in the efficacy of the CPI’s inflation gauge with respect to housing costs and the rate of increase in the actual value of a house. The report illustrates this by comparing the CPI to the S&P’s Case–Shiller Home Price Index (HPI), which is calculated based on records of repeat sales of the same properties over time.

Below is chart from the report showing this post-’83 split in the indices, which reveals a huge difference in the influence of housing inflation on total inflation as measured by the CPI.

Despite how heavily housing is weighted in the CPI, actual inflation in the real estate market has seemingly stopped registering in the BLS’s methodology. What the report argues this signifies is that, rather than reflect inflation in the housing market as it might relate to homeowners/buyers, CPI instead places an unrepresentative emphasis on rental costs over equity. As a result, increases in rental costs can be, and are, dampened in the overall CPI by decreases in home prices due to OER’s proportion of the index’s calculations (as shown in the chart below).

While this all might seem complex, the takeaway is that the CPI — the government’s main inflation gauge — might not be an entirely accurate measure of economic inflation in general, and could actually be a specifically lousy one when it comes to the cost and value of housing.

The report shows how this issue comes to a fore when it compares the BLS’s numbers on cost of living, which calculated a 31 percent increase in housing expenses for renters between 2005-2015 when the actual increase is at 40 percent. The report argues that this overemphasis on rental expenses entirely ignores actual real estate value and, as a result in recent years, kept inflation artificially low against rising home values.

The report points to the BLS’s inflation gauge as a growing pain point in U.S. monetary policy, one that could severely hamper the economy if home values aren’t better reflected in the CPI. You can download the whole report to read more about the research team’s findings and further research into possible solutions or considerations into measuring inflation.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.