The European Central Bank (ECB) announced that demand for Euro-denominated international bonds and loans increased 40% in 2024, reaching levels not seen since the global financial crisis.

Euro-denominated bonds issued by US firms, known as "Reverse Yankees," surged to nearly $95 billion last year, compared to $60 billion in 2023, the ECB said in a recent report. Firms seeking cheaper capital, driven by a growing interest rate disparity across the Atlantic, fueled the increase.

"There is evidence of a link between shifts in invoicing currency patterns in global trade and geopolitical alignments," ECB President Christine Lagarde said in the opening remarks of the report published on June 11. "New challenges to the euro's international role have also emerged, including initiatives promoting the global use of cryptocurrencies."

Despite this resilience in international finance, the euro has lost its longstanding position as the second-largest foreign reserve asset. Gold, which surged in both price and official holdings in 2024, has replaced it.

Central banks purchased more than 1,000 tons of gold, double the decade average, driving their share of global reserves to 20%, compared to the euro's 16%.

Gold's strong demand over the last three years reflects the growing global mistrust of fiat currencies. Ongoing geopolitical tensions have increased the risks of fiscal deficits and monetary debasement, given the plans such as Readiness 2030, which sees €800 billion in defense spending.

ECB Policy Focuses on Cutting Rates, Growth

In response to Eurozone inflation at just 1.9%, the ECB has halved its benchmark rate over the past year, with its policy rate now standing at 2%. Services inflation has cooled from 4% to 3.2%, while goods inflation remains subdued at 0.6%.

"In our mission we have price stability but we also know that there cannot be price stability without financial stability," Lagarde said in a recent interview for CGTN. "So, we are very focused on monitoring the potential risks, the uncertainty that abounds around the European economy, to anticipate any further consequences and be able to respond. But at this point in time, we have stabilized prices at the level that we were expecting."

Still, with economic growth expectations downgraded and inflation projected to dip further in 2026, the ECB faces the risk of deflationary pressures re-emerging, an echo of the post-2010 euro crisis period.

Further appreciation of the euro could threaten exports and further reduce inflation, potentially prompting additional rate cuts. Meanwhile, the ECB has continued to push for deeper capital market integration and the rollout of a digital euro to bolster the currency's global standing.

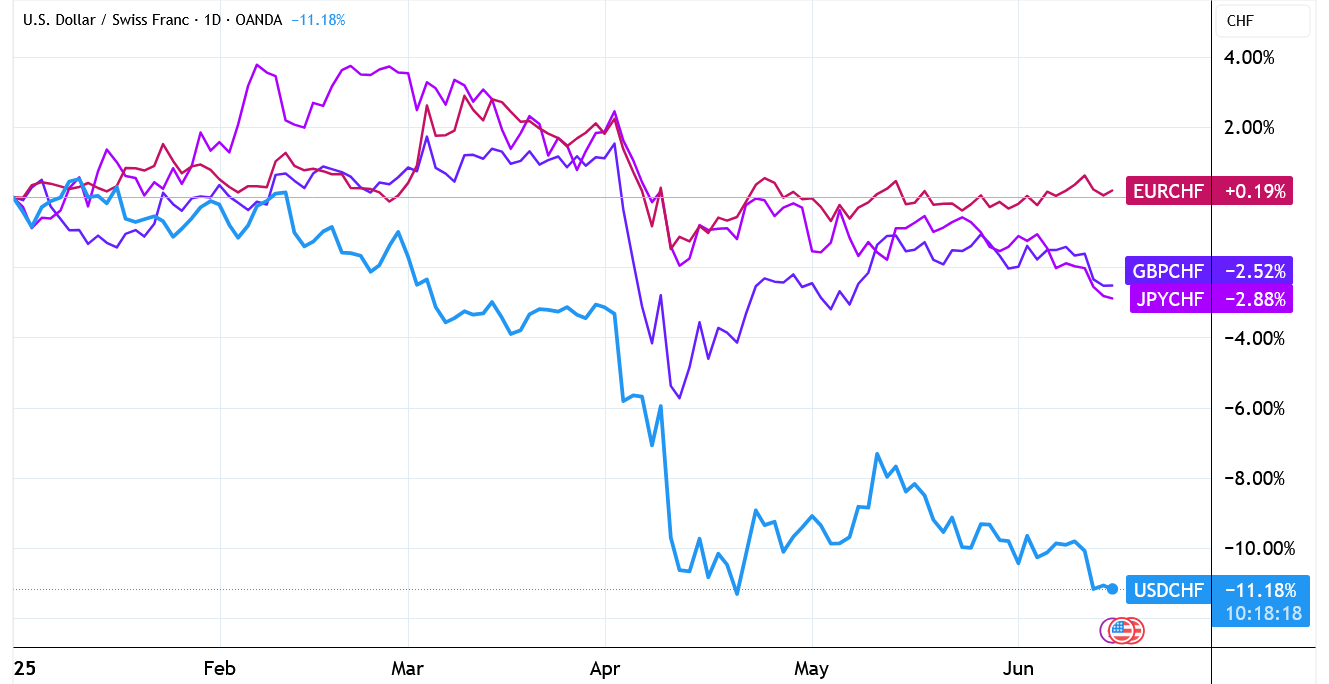

Swiss Franc's Safe Haven Strength Raises Policy Dilemma

The Swiss franc is once again proving to be Europe's haven. As geopolitical risks surge, particularly with the latest conflict between Israel and Iran, the franc's attractiveness has continued to grow. Yet, strengthening the currency comes with challenges.

In May, Switzerland returned to deflation for the first time since 2021, with consumer prices falling 0.1% year-over-year. Declines were widespread, from transport to household goods, pushing inflation back to the lower edge, or below, of the Swiss National Bank's (SNB) 0–2% stability target.

With the franc appreciating, the SNB is under pressure to act. Its next monetary policy meeting on June 19 is expected to deliver another 25 basis point cut, taking the policy rate to zero.

By September, the rate could fall to -0.25% or even -0.75%, reintroducing the controversial era of negative interest rates. The SNB employed negative rates from 2015 to 2022.

Meanwhile, short-dated Swiss government bonds have entered the territory of negative yields. The two-year yield touched as low as -0.225% on June 3, and nearly a quarter of the outstanding Swiss government debt yields less than zero.

That development shows that the strength of the Swiss franc isn't a speculative play, but rather a movement by institutional tactical asset allocators who must manage large cash portfolios.

British Pound Is At A Crossroads

The British pound has seen mixed fortunes in 2025. Once bolstered by high yields and demand for carry trades, sterling fell 1.7% on June 17 to $1.3427—its worst single-day performance in over a month.

The pound's slide followed a string of weak labor market data, including the sharpest drop in employment in five years and slower-than-expected wage growth, according to data for May.

"The dovish repricing of BOE rate-cut expectations takes some of the shine off the pound," Lee Hardman, a senior currency analyst at MUFG, told Bloomberg. He noted that the strengthening trend is "unlikely on its own to reverse the recent upward trend unless the BOE signals it is more willing to speed up rate cuts."

Bank of England interest rate plot (2016-Present), Source: Bank of England

The Bank of England (BOE), which has already cut rates four times to 4.25%, is facing mounting pressure to ease them further. Markets are fully pricing another rate cut in September and see a 90% chance of an additional move by December.

BOE's Rate Journey Remains Unclear

Yet the path ahead is far from clear. Inflation remains sticky, with April's annual CPI at 3.4%, well above the BOE's 2% target, and expected to rise to 3.7% before cooling in 2026. Thus, opinions diverge on the most optimal policy path.

Some, like BOE committee member Alan Taylor, want deeper and faster cuts amid deteriorating growth. Others, including economists at JP Morgan and Schroders, argue that inflationary risks from elevated wage and services costs warrant a more cautious approach.

Options markets reflect this uncertainty, with no apparent bias in the direction.

Nevertheless, the pound remains one of the highest-yielding G10 currencies and has benefited from a rebound in risk appetite. Unless the BOE signals a more aggressive pivot toward easing, or the inflation picture improves substantially, the pound may struggle to maintain its upward momentum.

Disclaimer:

Any opinions expressed in this article are not to be considered investment advice and are solely those of the authors. European Capital Insights is not responsible for any financial decisions made based on the contents of this article. Readers may use this article for information and educational purposes only.

This article is from an unpaid external contributor. It does not represent Benzinga’s reporting and has not been edited for content or accuracy.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.