The Viridian Cannabis Deal Tracker is an information service that monitors capital raise and M&A activity in the legal cannabis industry. Each week the Tracker analyzes/aggregates all closed deals and allocates each transaction to one of twelve key industry sectors in which the deal occurred (from Cultivation to Brands), the region in which the deal occurred (country or U.S. state), the status of the company announcing the transaction (public vs. private) and the type of deal structure (equity vs. debt).

The Viridian Cannabis Deal Tracker provides the deal data/terms/valuations/structures and market intelligence that cannabis companies, investors, and acquirers utilize to make informed decisions regarding capital and M&A strategy. Since its inception in 2015, the Viridian Cannabis Deal Tracker has tracked and analyzed more than 2,500 capital raises and 1,000 M&A transactions totaling over $45 billion in aggregate value. Find it exclusively on Benzinga Cannabis every week!

Below is a summary of the first half of 2020.

After a brutal 2019 during which global cannabis stocks lost approximately 70% of their value, the beginning of 2020 was relatively benign, but as the impact of COVID-19 became clear, global cannabis stocks traded off another 62%, finally bottoming out around March 18.

The stock decline further exacerbated the cannabis capital crunch, bringing capital raises for earlier stage companies and most M&A activity to a virtual halt.

Stock prices and market conditions have improved significantly since the bottom, but cannabis stock prices are still about 25% down since the beginning of the year. The partial recovery has brought back a bit of vigor to the capital raise and M&A activity in the industry.

Cannabis was classified as an “essential” business by most states, allowing continued albeit altered operations. Cannabis sales volume has held up remarkably well and recent data suggests an acceleration of the growth trajectory despite general economic weakness.

Canadian LPs and several large U.S. MSOs continue to retrench, restructure and divest non-core operations. U.S. companies have generally fared better, and several large MSOs are now positive EBITDA and successfully consolidating their market positions.

Some of the largest cannabis M&A deals ever closed during 1H’2020, including Curaleaf/Select and Cresco/Origin House and another major transaction, Curaleaf/Grassroots closed in July 2020.

The unbridled and undisciplined pace of M&A activity from 2016 to 2019 is over. Tighter capital and lower public company valuations are mandating M&A strategies that are much more accretive financially and strategically.

Cannabis SPAC IPO’s raised more than $2.6 billion in the last year, and more than $700 million in 1H’2020, as institutional investors recognized the opportunity to acquire distressed/discounted assets in the industry.

The U.S. cannabis marketplace has become the dominant focus of both investors and acquirers.

1st Half 2020: Capital Raise Summary

Capital raise transactions decline

We tracked 166 capital raises in the first half of 2020 that raised a total of $2.6 billion, a decline of 67.5% versus the first half of 2019, and a decline of 32.2% versus the second half of 2019.

Sales-leasebacks and SPACs tilt capital allocation ratios

Of the 12 industry sectors we actively track, Cultivation & Retail continues to lead with 55% of all invested capital, although down from 66% in the first half of 2019. The two other leading capital raising sectors were Real Estate (18% of invested capital, up from 4% in the previous year) and Investments/M&A (13% of invested capital, up from 7% in the previous year). These two sectors highlight the growing role of sales-leaseback financing and SPACs.

Public capital raises have become more dominant

Public companies represented 89.2% of the money raised and 80.7% of the number of transactions, significantly higher than the 70.3% of capital raised and 67.8% of the number of transactions registered for the first half of 2019. As in any distressed/uncertain environment, investors chase liquidity that public companies can provide.

Equity raises represented a similar percentage of total capital raises compared to the first half of 2019

Equity deals represented 70.5% of the number of capital raises and 67.5% of total capital raised versus 70.2% of the number of capital raises and 68.7% of total capital raised in the first half of 2019. Debt financing and debt providers have become much more active in the industry providing an additional source of financing.

Convertible debt shrinks as straight debt becomes a larger part of the landscape in the U.S.

Canadian companies utilized straight debt in 61% of their debt capital raises in the first half of 2020 versus 36.3% for U.S. companies. Historically straight debt has been confined to ancillary, non-plant touching sectors of the U.S. market, but this is beginning to change. Late 2019 and 2020 to date have seen several large straight coupon debt issuances by U.S. MSOs and we expect this trend to continue as more of them become free cash flow positive.

Capital Raises Recovering with Stock Prices

Cannabis capital raise activity, particularly equity raises, are quite sensitive to cannabis stock price levels.

Between the end of the second quarter of 2019 and the beginning of 2020, cannabis stocks declined 43%, adding to the damage from earlier in the year decreases.

The market traded off an additional 45% between the beginning of 2020 and its bottom on March 16, as the full impact of COVID-19 became apparent. The total market decline from the end of the Q2’2029 through the market bottom was approximately 69%.

Market disruption from COVID-19 brought fundraising in the cannabis market to a virtual standstill in May before it began to bounce back in response to a strong recovery of stock prices which have increased 92% from the bottom

2nd Half Outlook for Capital Raises

We Foresee Renewed Growth In Capital Raise Activity Based on Current Market Dynamics

Valuation levels have stabilized after a significant bounce off the bottoms.

Reduced overall valuation levels will drive increased investor interest.

Companies will continue to require growth capital as the industry shows increasing growth rates.

Consolidation/roll-up initiatives underway across the industry will require both acquisition and operating capital.

COVID-19 induced budgetary shortfalls will give more states an incentive to pass Medical and Adult-Use legislation in the November 2020 elections.

Potential for landmark changes in federal regulation of cannabis if Democrats win control of the White House and Senate in addition to retaining the House.

1st Half 2020: M&A Summary

M&A activity continued to fall from an already low level in the second half of 2019

We tracked 39 M&A transactions in the first half of 2020, down 81% from the 205 recorded in the first half of 2019. The drop in M&A activity directly relates to the dramatic decline in cannabis stock prices as most industry transactions are predominantly stock-based.

Sector Rotation

Cultivation & Retail, consistently the largest M&A sector, recorded 25 M&A transactions in the first half of 2020, down 79% from the 117 recorded in the first half of 2019 and 61% from the 64 recorded transactions in the second half of 2019. Significant declines in activity also occurred in Hemp, and Infused Products and Extracts. The Biotech/Pharma sector saw the largest increase in M&A activity.

Going-public deals recoil from their peak in the second half of 2019

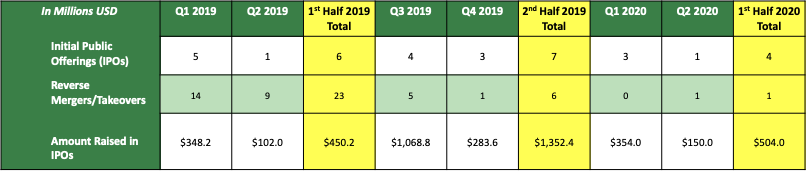

We recorded 5 going-public transactions in the first half of 2020, raising a total of $504 million. This number of transactions was 62% lower than the 13 recorded in the second half of 2019 and the capital raised was 63% lower than the $1.35 billion raised in the second half of 2019. The change was largely due to the virtual cessation of RTO transactions (1 versus 6) and a lower amount of SPAC capital raised. The second quarter of 2019 figure was heavily influenced by two large SPAC IPOs (Bespoke and Subversive) that together raised $925 million.

Corporate M&A strategy evolves

The unbridled and undisciplined pace of M&A activity from 2016 to 2019 is over. Tighter capital and lower public company valuations are mandating M&A strategies that are much more accretive financially and strategically.

2nd Half Outlook for Mergers & Acquisitions

We Foresee a Pick-Up in M&A Activity Based on Current Market Dynamics

SPACs should begin to announce/close deals.

Reduced valuation levels for private companies will drive buyer demand.

Companies that can’t raise growth capital will pursue M&A exits.

Distressed companies will be sold as ongoing operations or in pieces.

The U.S. cannabis marketplace will remain the dominant focus of both investors and acquirers.

Capital Raise Activity

1st Half 2020 Capital Raise Key Figures

Total Capital Raised: $2.55 Billion

YoY Growth: -65.75%

# of Raises: 166

YoY Growth: -50.89%

Largest Raise: $300 Million

Most Active Cannabis Sector: Cultivation & Retail

Most Active Region: U.S.

Q2 2020 Capital Raise Key Figures

Total Capital Raised: $908.8 Million

YoY Growth: -73.01%

# of Raises: 87

YoY Growth: -54.92%

Largest Raise: $174 Million

Most Active Cannabis Sector: Cultivation & Retail

Most Active Region: U.S.

COVID-19 Impact on Cannabis Capital Markets

We compared data from the Viridian Cannabis Deal Tracker for June 2020 (4th full month of COVID-19) vs. the prior months of Q2’2020, the prior quarter (Q1’2020) and prior yearly period (Q2’2019).

Financing Activity Still Weak But Improving

Total capital raises were down in June 2020 versus May 2020 but still 86.8% higher than in March 2020, the weakest month we have recorded.

Equity issuance is up strongly since March, due in part to the recovery in stock prices.

Debt issuance has remained weak since the onset of COVID-19 as more conservative debt investors ponder the sustainability of the industry’s robust performance in the face of severe economic disruption.

Public vs. Private Company Capital Raises

Public companies represented 85.0% of all capital raises in the second quarter of 2020, down from 91.5% for Q1’2020 but up from the 61.7% for Q2’2019. The turbulence in global markets in general, and the cannabis markets in particular, will continue to drive investors to seek liquidity. The capital crunch in the cannabis industry is acutely impacting private companies.

Capital Raise Activity: Public versus Private

Viridian Capital tracked 166 capital raises in the first half of 2020 that raised a total of $2.6 billion.

Public companies represented 89.2% of the money raised and 80.7% of the number of transactions. These are significantly higher than the 70.3% of capital raised and 67.8% of the number of transactions registered for the first half of 2019.

Total capital raised in the first half of 2020 declined 67.5% versus the first half of 2019 and 32.2% versus the second half of 2019. Public company capital raises faired slightly better, with capital raised in the first half of 2020 decreasing 58.9% from the first half of 2019, but only 7.1% versus the second half of 2019.

The stock price decline and capital crunch is a result of investor realizations that prior valuation metrics were unsustainably high, particularly given the fact that cannabis companies have repeatedly performed below analyst expectations.

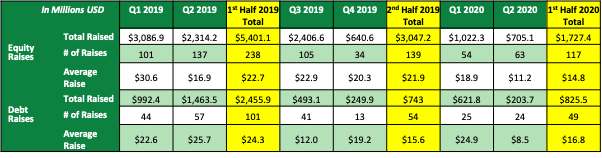

Capital Raise Activity: Equity vs Debt

After strong growth in 2019, the number of debt deals, and the total debt capital raised fell in the first half of 2020. Canadian companies accounted for the largest share of the decline. In the first half of 2020, Canadian companies raised $257.6 million in 37 transactions, down 82.6%, and 47.9% respectively from the $1,481.9 million in 71 transactions in the first half of 2019. U.S. companies raised $567.1 million in 11 transactions, down 37.5%, and 56.0% respectively from the $907 million in 25 transactions in the first half of 2019.

Equity deals represented 70.5% of the number of capital raises and 67.5% of total capital raised versus 70.2% of the number of capital raises and 68.7% of total capital raised in the first half of 2019.

Debt deals represented 29.5% of capital raises and 32.5% of capital raised in the first half of 2020 versus 29.8% of the number of capital raises and 31.3% of the total capital raised in 2019.

We expect debt deals to reaccelerate in the second half of 2020 as more companies achieve positive EBITDA and free cash flow status, demonstrating the capacity to service debt.

1st Half 2020: Convertible vs. Straight Debt

Convertible debt has historically made up the bulk of debt issuance in the cannabis market. In the first half of 2019 convertibles represented 61.0% of the debt transactions and 65.1% of total debt capital raised.

The dramatic fall in the cannabis equity market shifted this emphasis in the second half of 2019 with convertibles representing only 50% of the issues by number and 29.4% of total capital raised. Convertibles bounced back in the first half of 2020, representing 63.3% of the issues and 56.3% of total debt capital raises.

Canadian cannabis companies have greater access to banks and traditional financing sources, and this is mirrored in the debt composition. In the first half of 2020, Canadian companies raised 39.0% of their total debt capital via convertible debt compared to 63.7% convertibles for U.S. companies.

Late 2019 and early 2020 saw the first sizeable straight debt issues by stronger U.S. MSOs including Curaleaf, and Cresco. Other strong credits, including Green Thumb and Trulieve, were able to close transactions with relatively modest warrant coverages (in the 20% range). We expect more straight debt transactions for the top tier of U.S. cannabis credits (similar to the recent Verano deal).

One interesting structure that we have seen quite frequently since the capital crunch is secured convertible debt with additional warrants. Total warrant coverage (including the 100% from the convert) has been observed as high as 250%, offering investors an attractive upside in a gapping upward market move such as might be experienced with federal legalization.

1st Half 2020 Top 10 Capital Raises

Capital Raises by Industry Sector – 2019/2020

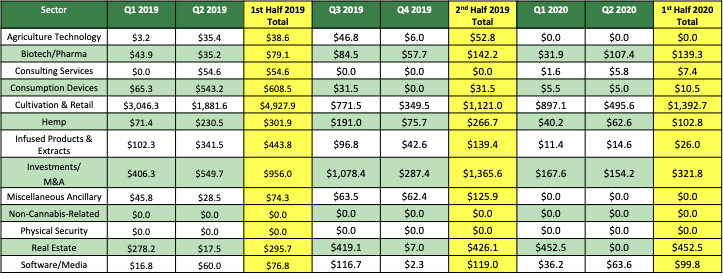

Cultivation & Retail continues in its historical role as the largest capital raising sector, but its relative percent of capital raised fell to 55% in the first half of 2020 versus 66% in the first half of 2019.

The Investments/M&A sector has increased in importance and took the top position in the second half of 2019, reflecting IPOs by cannabis SPACs. The sector represented 13% of capital raised in the first half of 2020 versus 7% in the first half of 2019.

A major trend is the growth in capital raised by the Real Estate sector which is up 53.0% from the first half of 2019 and represents 18% of total capital raised versus 4% in the first half of 2019. The main impetus for this increase is the rise of real estate SPACs and REITs both offering advantageous sales-leaseback financing.

Agriculture Technology Capital Raises

Sector Description: Providers of controlled environment agriculture (CEA) and other cultivation technologies.

The Agriculture Technology sector had no new capital raises in the first half of 2020, down from 11 transactions for a total of $38.6 million in the corresponding period in 2019.

More than ½ of the dollar amount of transactions in the first half of 2019 was attributable to two large deals: GrowGeneration ($12.8M) and Arcadia Biosciences Inc. ($7.5M).

The last half of 2020 looks promising for this sector with one transaction for $15M already on the books in July.

Biotech/Pharmaceuticals Capital Raises

Sector Description: Companies pursuing clinical development of cannabinoid-based drug candidates through the FDA, the EMA, or a similar regulatory body.

The Biotech/Pharmaceuticals sector saw a 92.3% increase in the number of transactions and a 76.1% in the total capital raised in the first half of 2020 vs. the corresponding period in 2019.

A large portion of the increase in capital raised in the first half of 2020 is due to the $42.4 million increase in debt raised, most of which is accounted for by two transactions: $27.9M by MediPharm Labs, and $10M by Pharmhouse in Q2: 2020.

Biotech/Pharmaceuticals sector stock prices have been buoyed by COVID-19 vaccine and treatment expectations

Consulting Services Capital Raises

Sector Description: Providers of various consulting services, including management, operations, strategy, compliance, licensing, et al.

The Consulting Services sector saw a 50.0% increase in the number of transactions but an 86.4% decrease in total capital raised in the first half of 2020 vs. the corresponding period in 2019.

2019 figures were skewed by the inclusion of the $50M 4Front Holdings LLC term loan which accounted for 91.6% of total capital raised in the sector during the first half of 2019

Consumption Devices Capital Raises

Sector Description: Manufacturers and downstream sellers of various consumption devices, such as vaporizers, rigs, glassware, etc.

The Consumption Devices sector saw a 75.0% decrease in the number of transactions and a 98.3% decrease in total capital raised in the first half of 2020 vs. the corresponding period in 2019.

First half 2019 results were skewed by two large equity raises: Pax Labs Inc. ($420.0M) and Greenlane Holdings ($102.0M).

The vape scare, beginning in the 3rd quarter of 2019, substantially undercut interest in the sector, particularly in the U.S. with an only slight recovery in the 2nd quarter of 2020.

Cultivation & Retail Capital Raises

Sector Description: Companies that grow, distribute, or sell cannabis and cannabis-derived products.

The Cultivation and Retail sector saw a 43.5% decrease in the number of transactions and a 71.7% decrease in total capital raised in the first half of 2020 vs. the corresponding period in 2019.

Cultivation and Retail continues to be the largest capital raising sector, accounting for 47.0% of the total number of cannabis capital raises and 54.5% of capital raised.

The decline in capital raised began in the third quarter of 2019 and accelerated through the 1st quarter of 2020 before recovering slightly in the 2nd quarter of 2020 based on increased stock prices and stronger financial performance in the sector.

Hemp Capital Raises

Sector Description: Companies that grow, distribute, or sell hemp and hemp-derived products.

The Hemp sector saw a 78.6% decrease in the number of transactions and a 66.0% decrease in total capital raised in the first half of 2020 vs. the corresponding period in 2019.

Hemp acreage planted has grown more than 70% since the 2018 Farm Bill causing an oversupply and dramatic decline in raw CBD prices.

Growth in the industry remains highly uncertain as the entrance of large CPG companies into the ingestible CBD market has been stalled by delays in FDA regulation.

Several large hemp processors have filed for Chapter 11 and others are also experiencing distress. A significant increase in restructuring activity is expected in this sector in the second half of 2020.

Infused Products & Extracts Capital Raises

Sector Description: Companies that extract and refine cannabis/hemp derived oils as well as develop and sell cannabis/hemp - infused foods, drinks, cosmetics, and other products.

The Infused Products & Extracts sector saw a 66.1% decrease in the number of transactions and a 94.1% decrease in total capital raised in the first half of 2020 vs. the corresponding period in 2019.

Activity in the sector began to decline in the second half of 2019 and has not recovered.

Several brands have begun to coalesce, particularly in the edible segment of the market however, the state-by-state nature of branding in the industry has prevented the emergence of any truly dominant brands.

Investments/M&A Capital Raises

Sector Description: Financial service firms, investment funds, holding companies, and other capital providers targeting the cannabis industry.

The Investment/M&A sector saw a 53.7% decrease in the number of transactions and a 66.3% decrease in total capital raised in the first half of 2020 vs. the corresponding period in 2019.

Two U.S. listed SPAC issues (Collective Growth Corp $150M and Greenrose Acq. Corp $150M) accounted for 93.2% of total capital raised in the sector in the first half of 2020. Collective Growth is the first SPAC specifically targeted towards the U.S. Hemp sector.

Activity in the sector in 2019 was also heavily influenced by SPACs with 2 larger SPAC issues (Mercer Park Brand Acq $402.5M and Tuscan Holdings $276.0M) accounting for 71.0% of total capital raised.

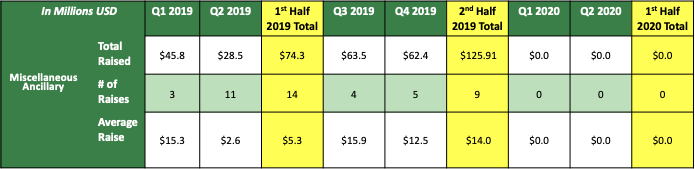

Miscellaneous Ancillary Capital Raises

Sector Description: Service or product companies, such as testing laboratories, specialized packaging, branding, and labeling companies, and cannabis-focused recruitment firms, that fall outside the other ancillary sectors.

The Miscellaneous Ancillary sector saw a complete absence of activity in the first half of 2020 vs. 14 deals for a total of $74.3M in the first half of 2019.

The $34 million equity issue by KushCo Holdings in January 2019, made up 45.8% of the sector’s total capital raised in the first half of 2019.

Real Estate Capital Raises

Sector Description: Companies that own, lease, develop, or license commercial properties for cannabis operators.

•The Real Estate sector saw a 70.0% decrease in the number of transactions but a 53.0% increase in the total capital raised in the first half of 2020 vs. the corresponding period in 2019.

•Two large issues by Innovative Industrial Properties ($250M) and Subversive Real Estate Acquisition REIT LP ($200M) together accounted for 99.4% of capital raised in the sector during the first half of 2020. Subversive was the first cannabis real estate SPAC. These issues demonstrate the dramatic rise of cannabis sales-leaseback financing which has been extensively utilized by MSOs as one of the lowest cost financings that is available.

Software & Media Capital Raises

Sector Description: Companies that develop and provide technology, software, data, and media solutions such as seed-to-sale tracking, delivery, enterprise software, etc.

The Software & Media sector saw a 35.3% decrease in the number of transactions but a 29.9% increase in total capital raised in the first half of 2020 vs. the corresponding period in 2019.

A majority (68.7%) of the increased capital raised in the first half of 2020 was made up of one innovative $17M convertible debt issue by Akerna Corp. which included a 12% original issue discount and monthly principal payments but no regular interest payments.

Capital Raises: International

While the majority of deals we have tracked have been closed by companies in the U.S. or Canada, we continue to see increased activity by companies in South America, Europe, Africa, and Asia as cannabis liberalization proceeds in those markets. International deals accounted for a record 12.4% of financing in the last half of 2019 but have returned to a more usual 3.4% of capital raised in the first quarter of 2020.

Financing activity is shifting from Canada to the U.S. and we anticipate this trend continuing as more states pass medical or adult-use measures and the prospects for federal legalization increase

1st Half 2020 Capital Raises by State

California and New York continue to top the list, but newly adult-legalized states of Massachusetts and Illinois have taken the number three and four slots as capital demand for new growth facilities and dispensaries accelerates.

We anticipate greater capital demand in states that are pushing to turn recreational, including New Jersey and Pennsylvania.

M&A ACTIVITY

1st Half 2020 M&A Key Figures

Q2 2020 M&A Key Figures

COVID-19 Impact on Cannabis Capital Markets

M&A

Public Companies Dominate Buy-side M&A Activity

Public companies represented 94.4% of buy-side acquisition activity in the second quarter of 2020, up from 90.5% in Q1’2020 and 80.2% in Q2’2019.

Even with depressed market caps, public companies remain the only viable acquirers.

Inability to raise capital, along with the lack of marketable securities to pay for an acquisition, have taken the private company out of the buy-side M&A market.

Private Companies Dominate Sell-side M&A Activity

Private companies represented 88.9% of sell-side acquisition activity in the June 2020 quarter, down from 95.2% in Q1’2020 and 90.0% in Q2’2019.

The depressed valuations of private companies makes them attractive acquisition targets.

The closing of the IPO/RTO window makes sell-side M&A the primary path to a liquidity event for private companies.

M&A Activity: Public vs. Private

M&A Activity: Public vs. Private

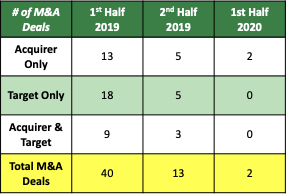

Overall M&A activity has leveled off but not recovered from its 2019 levels. The 39 closed transactions in the first half of 2020 are 59% lower than the 95 closed deals in 2019’s second half and 81.0% below 2019’s first-half total of 205.

Two of the largest U.S. Cannabis M&A transactions ever completed occurred in the first half of 2020: the $950 million Curaleaf/Select deal, and the $400 million Cresco/Origin House deal. Cannabis companies also canceled several noteworthy transactions in the first half of 2020, including the $850 million Harvest/Verano deal.

Public acquisitions of private companies continue to be the prevailing transaction model in the industry, accounting for 94.9% (2 out of 39) in the first half of 2020, up from 69.3% (142 out of 205) of the deals in the first half 2019.

Acquisition activity is expected to increase in the second half of 2020 buoyed by SPAC activity and opportunistic distressed acquisitions by the stronger industry players.

1st Half 2020 Top 10 M&A Transactions

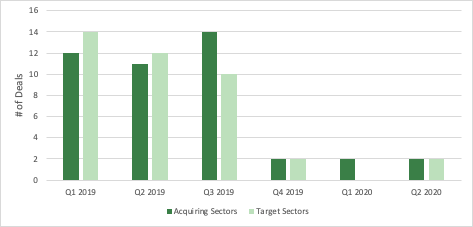

M&A Activity: Acquirer Sector Breakdown

Companies in the Cultivation & Retail sector have been the dominant acquirers expanding into new markets but increasingly concentrating on building scale in existing markets.

Cultivation & Retail M&A activity is expected to increase in the second half of 2020 and into 2021 as new states open for both medical and recreational cannabis.

Biotech/Pharma companies were the second most active acquirers in the first half of 2020 and the only sector to experience more deal flow than in the 1H’ 2019.

M&A Activity: Target Sector Breakdown

Cultivation & Retail remains the favorite target sector as MSOs continue to expand into new markets and build scale in existing markets.

The Hemp sector, which was negatively impacted by sharp price declines, bankruptcies of large competitors, and continued delay in FDA rulemaking, had no transactions in the first half of 2020.

The decline in Non-Cannabis-Related transactions stems from the collapse of RTOs which accounted for 21 deals in the first half of 2019, 3 deals in the second half of 2019, and 0 deals in the first half of 2020.

Agriculture Technology M&A Activity

Most transactions in 2019 and 2020, where the target was a company in the Agriculture Technology sector, have been completed by other companies in the same sector. We expect this to change over the next year as cultivators seek increased yields, greater operating efficiency, and lower costs.

Since the beginning of 2019, GrowGeneration Corp. has completed 80% (8 out of 10) of the transactions where the acquirer was an Agriculture Technology company.

Biotech/Pharmaceuticals M&A Activity

•Biotech/Pharmaceuticals sector M&A activity is up in the first half of 2020 versus both the first half of 2019 and the second half of 2019.

•We expect to see continued strong activity in this sector as research steps up to address the uses and efficacy of the “lesser” cannabinoids like CGG and CBN as well as potential COVID-19 applications of cannabinoid-derived drugs.

Consulting Services M&A Activity

The first glimmer of activity in this sector since 2018 occurred in the first half of 2020 with the purchase of a small consulting company by Harvest Health and Rec. and the acquisition of a small Biotech company by Osoyoos Cannabis, a Canadian contract tolling extraction services company.

This sector could see an upswing if, as we expect, COVID-19 budget shortfalls foster increased state legalization efforts.

Consumption Devices M&A Activity

The Consumption Device sector saw a 71.4% decrease in the number of transactions by buyers and sellers.

The attractiveness of the sector as an acquisition target collapsed and no transactions occurred in the first half of 2020.

Negative influences included tariffs on Chinese goods and the vape scare both of which appear to be resolved.

Cultivation & Retail M&A Activity

Combined buy and sell transaction volume of 25 deals in the first half of 2020 was down 60.9% versus the 2H’ 2019 and 78.6% versus the 1H’ 2019.

The decrease in M&A activity is directly related to the collapse of cannabis stock prices. An index of U.S. Cannabis companies was 83.6% from the end of the first quarter of 2019 through the end of the first quarter of 2020. The market performed strongly in the second quarter of 2020, increasing by approximately 41.0% from its end of March levels and spurring an increase in both capital raises and M&A volume in the second quarter and beyond.

The Curaleaf/ Grassroots deal, valued at approximately $700 million and ranked as one of the largest U.S. cannabis acquisitions, closed in the third quarter of 2020. The transaction will require divestiture of around $100 million of assets in Illinois, Maryland, and Ohio to conform with local licensing restrictions.

Hemp M&A Activity

Hemp sector M&A activity has essentially ground to a halt with no transactions targeting the industry in the first half of 2020 compared to 27 in the first half of 2019. A similar decline has been seen concerning transactions where hemp companies were the acquirers.

The decline relates to the economic disarray in the industry with lower pricing and profitability than experienced in the year-earlier period.

The entrance of CPG companies into the CBD ingestible market has been indefinitely delayed by a lack of FDA regulatory action, which does not appear to be likely in the next several quarters.

Collective Growth Corp., the first Hemp SPAC, completed its $150 million IPO on 5/1/20 which should produce future M&A activity in the sector.

Infused Products & Extracts M&A Activity

Combined buy and sell activity of 6 transactions in the first half of 2020 was down 87.8% from the first half of 2019 and 78.6% from the second half of 2019.

This segment continues to have the potential for much higher activity fostered by two trends: 1) cannabis demand is shifting from flower consumption to vapes, edibles and other extracted/infused forms and 2) the cannabis and hemp businesses will eventually evolve into true CPG businesses which will present significant opportunities for acquirers to consolidate the fragmented industry through acquisitions.

Investments/M&A M&A Activity

Activity in the Investment/M&A sector declined 86.7% from 30 transactions in the first half of 2019 to 4 transactions in the first half of 2020.

A significant amount of the 2019 activity that was not repeated in 2020 was from SPAC investments including 4 separate acquisitions by Cannabis Strategics Acquisition Corp. that together created AYR Strategies, and the acquisition of assets by Cannacord Genuity Growth Corp. that formed Columbia Care. C21 investments also completed 3 acquisitions that helped form the integrated Oregon and Nevada cannabis company.

We expect this sector to heat up as an acquirer as roughly $3 billion of SPAC money now on the books is deployed.

Miscellaneous Ancillary M&A Activity

Combined buy and sell interest in this sector continues its downward path after peaking in 2018.

A significant part of the 2019 transaction volume consisted of acquisitions by CB2 Insights, a leader in clinical operations, technology, and analytical research services.

Physical Security M&A Activity

The Physical Security sector has seen no M&A transactions since the first half of 2019 and no capital raise transactions since 2018.

Real Estate M&A Activity

The Real Estate sector saw a 50% decrease in M&A activity in the first half of 2020 versus the first half of 2019.

Despite the lower M&A transaction volume, total capital raised in the sector increased significantly due to the equity raised for real estate SPACs and REITs providing sales-leaseback financing to the Cultivation and Retail sector.

Software & Media M&A Activity

The Software & Media sector saw a 76.5% decrease in M&A activity.

GOING-PUBLIC ACTIVITY

Going-Public Transactions – 2019/2020

The total number of IPOs and RTOs has declined in virtually every quarter since the first quarter of 2019. Total IPO/RTO activity in the first half of 2020 was 82.8% lower than in the first half of 2019 and 61.5% lower than the second half of 2019.

The decreased volume is particularly striking in the Reverse Mergers/ Takeovers category. There were 11 RTOs of Canadian companies and 9 of U.S. companies in the first half of 2019 and this has fallen to only 1 Canadian RTO in the first half of 2020.

The IPO transactions in the table include a large representation of SPAC IPOs.

Investors have been stung by the sharp decline of cannabis stock prices with virtually every investor who bought at RTO levels now well underwater. Baring complete federal legalization, these RTO levels seem unlikely to return. Investors have become distrustful of repeatedly lowered broker projections and are now waiting for a clear demonstration of paths to profitability while focusing heavily on company liquidity amidst the ongoing capital crunch.

1st Half 2020 Reverse Takeovers Key Figures

1st Half 2020 IPOs Key Figures

1st Half 2020 SPAC Transactions Key Figures

SPAC Transactions

The rise of Cannabis SPACs has been one of the most important trends in the last year.

SPAC IPOs since the third quarter of 2019 have raised over $2 billion of capital.

SPACs have replaced IPOs as the main takeout opportunity for mid to large private cannabis companies.

SPACs generally have 18 months to make a qualifying acquisition, so most of them still have ample time to pursue deals.

Outstanding SPACs are approximately evenly divided between those with Canadian listings and those with U.S. listings. The importance of the distinction is that NYSE and NASDAQ listed SPACs are prevented from pursuing acquisitions of plant-touching companies, which is expected to increase M&A activity in ancillary sectors.

SPACs are also expected to be aggressive bidders for distressed assets.

-

Lead image by Ilona Szentivanyi. Copyright: Benzinga.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.

Cannabis is evolving—don’t get left behind!

Curious about what’s next for the industry and how to stay ahead in today’s competitive market?

Join top executives, investors, and industry leaders at the Benzinga Cannabis Capital Conference in Chicago on June 9-10. Dive deep into market-shaping strategies, investment trends, and brand-building insights that will define the future of cannabis.

Secure your spot now before prices go up—this is where the biggest deals and connections happen!