The following is a contributed article from a content partner of Benzinga

Amid all the uncertainty and controversy caused by the ongoing COVID-19 crisis, one thing seems to be universally accepted: the economy is struggling. And, although less certain, it’s likely to get a lot worse in the coming months.

Governments across the globe have already injected trillions into their economies in an attempt to stave off the immediate damage caused as a result of the pandemic. The U.S. alone has spent over $2 trillion in relief.

This money will eventually need to be repaid, and it will likely involve a squeeze to public and private sectors that economists with The World Trade Organization expect could surpass those of the 2008 global financial crisis.

The thought is chilling for anyone who lived through the 2008 financial crisis, especially investors whose stock portfolios have enjoyed nearly a decade of growth that now seems destined to reverse in the coming months.

However, while all asset classes will no doubt be impacted by the economic fallout, investors who diversify may find themselves in a stronger position to weather the storm than others. In this article, we’ll explore three alternative investment strategies that you can protect your wealth over the times to come.

Bitcoin

Nobody knows how bitcoin will perform in the depths an economic downturn. Given the fact that it is only a little over a decade old, nobody is sure how it will perform under a variety of economic conditions. The world’s first cryptocurrency was only born in 2008, at the height of the global financial crisis, so it hasn’t had to weather any sustained period of global turmoil.

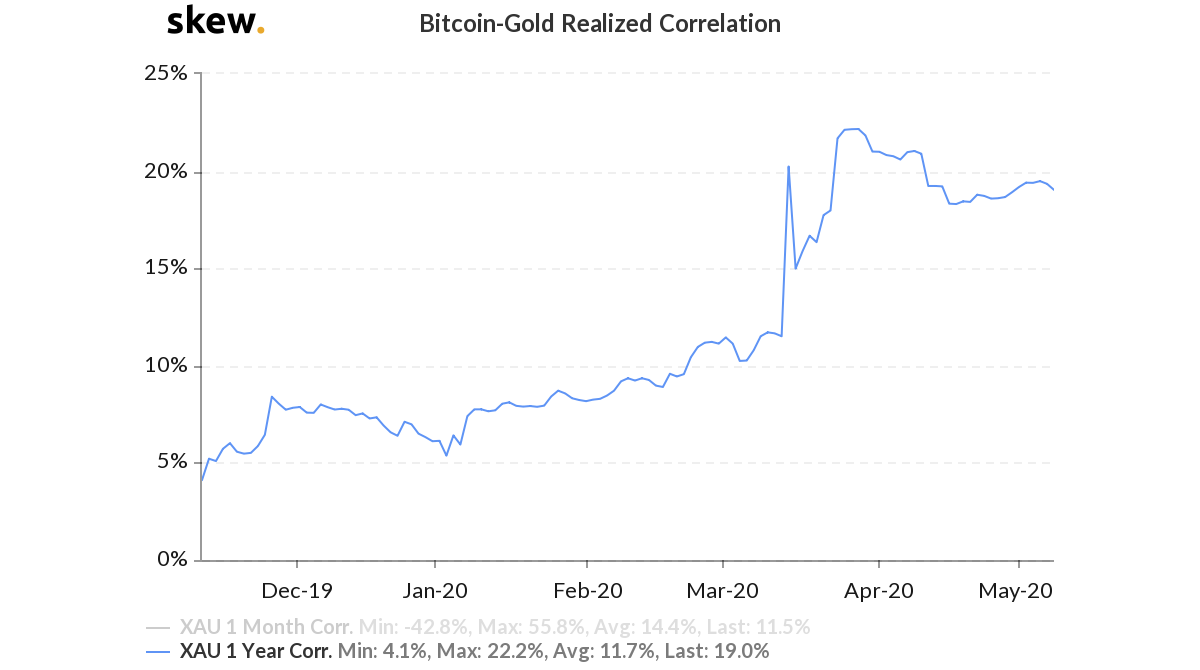

Nevertheless, in its most recent trial by fire, bitcoin has shown a decent amount of resilience as a store of value. The cryptocurrency has maintained a high correlation to gold throughout the pandemic, while also remaining mostly uncorrelated to the day-to-day movements of the stock market or other asset classes.

This correlation with gold rose sharply in mid-March following the crash in the stock markets at the height of the COVID-19 panic.

Source: Skew.com

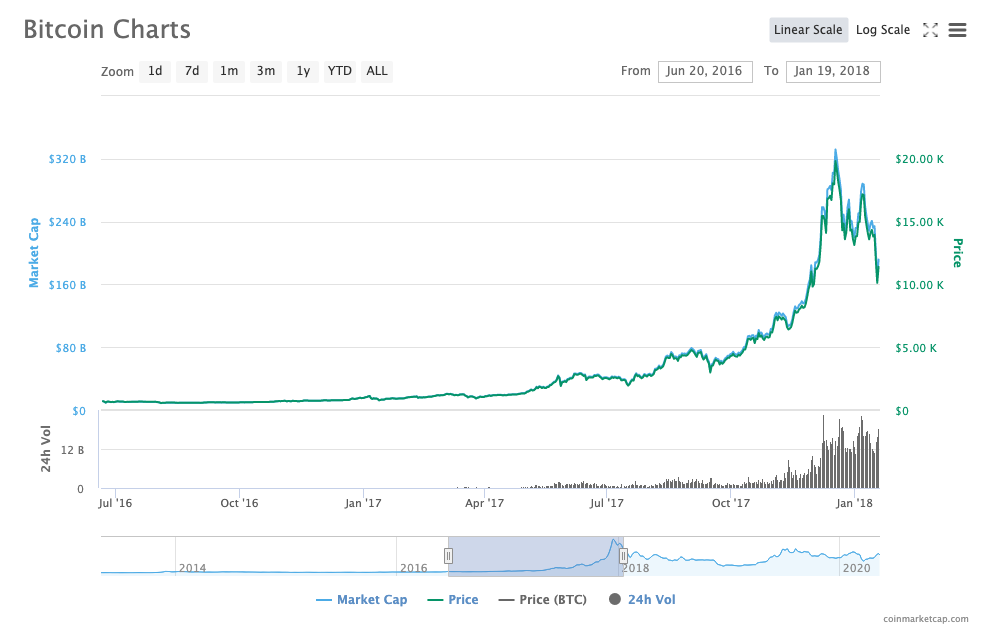

Adding to the potential interest in the digital coin, bitcoin also just recently undergone its third “halving,” which is a regularly scheduled event that reduces the number of bitcoins rewarded to miners by half, this time from 12.5 to 6.25. Historically, bitcoin has seen significant price increases in the year following the halving. In July 2016, when the last halving happened, Bitcoin was trading at around $650, and by December 2017, it reached its all-time high of $20,000.

Source: CoinMarketCap

Buying physical bitcoin is very easy these days, with some low fee exchanges such as Skrill allowing investors to fund their trades through their bank account or credit card. From there, investors are free to buy or sell bitcoin and various other cryptocurrencies on desktop or using the mobile app.

For those who want to dive deeper into the cryptocurrency space, Binance offers a more comprehensive range of trading products and services. These include derivatives contracts and a lending service that enables you to loan your cryptocurrencies to other users in exchange for interest payments.

Gold

Historically, gold has shown an inverse correlation to the stock markets and the US dollar. For example, during the 2008 financial crisis, the S&P 500 fell by over 35%, whereas the price of gold went up by 25% in the period between November 2007 and June 2009.

Gold prices during the last financial crisis Q4 2007 to Q2 2009. Source: Kitco

The main reason for this negative correlation is that the price of gold is almost purely driven by supply and demand, unlike stocks which are linked to the value of the underlying company. These factors make gold a solid choice for hedging against an economic downturn.

There are various ways to gain exposure to the price of gold. Firstly, you could buy physical gold in the form of bullion. However, this isn’t necessarily the easiest method. You’ll need a safe place to store your bars or coins, and it can be difficult to liquidate later down the line.

Furthermore, many gold merchants put significant markup on the price of physical gold, so you’ll have to see quite some upturn in price to cover those fees before you can start benefiting from any gains.

Perhaps a more accessible option is to invest in “paper gold.” There are a variety of ways of doing this, including certificates, or derivatives contracts such as futures.

However, for most individual investors, a passive method such as an ETF is probably the most attractive option. There are ETFs backed by physical gold, such as SPDR Gold Shares or iShares Gold Trust. Both of these offer exposure to the price of gold without taking ownership of the asset itself.

Performance of the iShares Gold Trust over the six months November 2019-April 2020. Source: iShares

Cash

Although the greenback is likely to take a hit as a result of the COVID-19 pandemic, it’s always worth keeping a portion of your portfolio in cash. It’s unlikely that cash will see the same levels of volatility as the stock markets, so keeping a stash of cash means you can hedge the impact of volatility on the rest of your portfolio.

Furthermore, cash is a store of liquidity that will enable you to jump on any opportunities that may arise as a result of a broader market downturn. Before the pandemic hit, Warren Buffett was sitting on a record $128 billion in cash, indicating he had a pretty good idea of what was coming.

Cash also allows you to implement a dollar-cost averaging strategy, setting a fixed amount each month for purchasing a particular asset. This means you can take advantage of low prices by buying more when prices are low, and hedge against higher prices by buying lower share amounts. Overall, this strategy reduces the average price paid per unit.

Changing Your Spending Habits

During times of economic insecurity, it’s easy to get into spending patterns that eat away at your monthly disposable income. For example, it’s effortless these days to sign up for an app or online service, only to discover they’re still taking a subscription fee from your credit card long after you stopped using it. You may be paying over the odds for insurance premiums or be sitting on a ton of loyalty points that could pay for goods or services.

The ultimate way to hedge against the economic risks of the bad times is to make sure you adopt a thrifty approach to spending. Redirect any savings into your investment portfolio where they can be put to work, helping to provide some shelter against the proverbial rainy day.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.