(Wednesday Fed Market Response) The Fed hiked rates 75 basis points for the fourth straight meeting today but offered what some investors saw as more dovish language in its statement. The doves scattered when Fed Chairman Jerome Powell took the mic. Stocks finished the day with steep losses.

The Fed’s benchmark rate now sits between 3.75% and 4%, the highest level in more than 15 years as the central bank presses even harder in its fight against stubborn inflation.

Even as the Fed kept its boxing gloves on, it offered investors hopeful language, hinting at a less hawkish stance in the future. In particular, the Fed said that it will continue to monitor the “cumulative impact” of tightening as it determines the pace of future rate hikes. The language appeared to give both stocks and bonds a lift, at least initially.

“The Committee anticipates that ongoing increases in the target range will be appropriate in order to attain a stance of monetary policy that is sufficiently restrictive to return inflation to 2% over time,” the Fed said in its post-meeting statement. “In determining the pace of future increases in the target range, the Committee will take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments.”

In short, that’s new language and sounded somewhat more market-friendly. It indicates that the Fed is thinking through the future pace of hikes, meaning perhaps it could consider more modest increases at coming meetings. It also acknowledges that the “cumulative” impact of all the rate hikes it’s made can take time to fully hit the economy, meaning it might want to wait and assess what the “lag impact” of higher rates might look like as more data roll in.

Markets Rally at First…and Then Came Powell

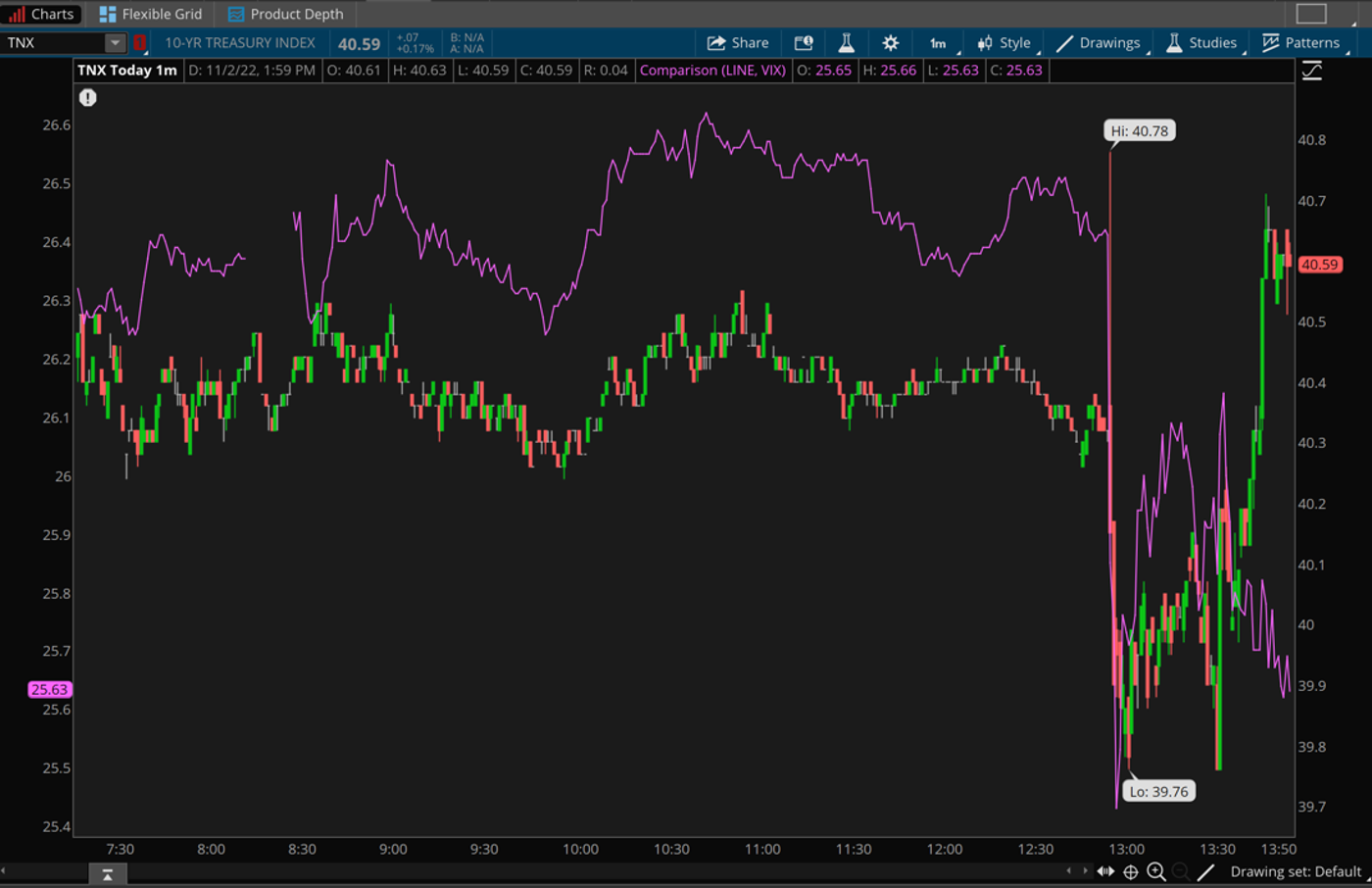

The market initially responded positively because investors were still considering this new language. Major stock indexes and bonds immediately rose. The S&P 500® index (SPX) initially gained 0.6%, and the U.S. 10-year Treasury yield (TNX) dropped to 4%. The Cboe Volatility Index® (VIX), which had been near 26.5 before the decision, pulled back to 26. That’s near a one-month low.

But what a difference a media scrum makes. During his press conference, Powell arguably sounded more hawkish, and stocks quickly gave back their initial gains. The Dow Jones Industrial Average® ($DJI)ended up sinking more than 500 points, or 1.55%, to close at 32,147.76. The Nasdaq® ($COMP) fell a steep 3.36%, and the SPX slipped 2.5% to 3759.69. The early post-Fed statement rally faded very quickly as Powell spoke.

Powell said the Fed remains committed to rate hikes as it attacks inflation, noting that “without price stability, the economy doesn’t work for anyone.”

In fact, he said the peak of Fed rates might need to be even higher than the Fed previously thought. The September Fed dot plot showed a terminal rate of 4.6% in 2023. Powell didn’t say how high rates might have to go but indicated the coming jobs and Consumer Price Index (CPI) reports could help determine the ultimate peak. The market has priced in about a 5% peak next summer.

When asked about the pace of future rate increases, Powell said the Federal Open Market Committee (FOMC) is having discussions about the speed of hikes and will likely address that at its next meeting. “We haven’t tightened too much or too fast,” he said. “There’s still ground to cover, and cover it we will.”

He said the Fed’s statement shouldn’t be viewed as the Fed promising any kind of a pause in rate hikes, and that the Fed will be watching data as it makes decisions. The housing industry has retreated due to higher rates, but the jobs market continues to look very strong, according to Powell. The economy has slowed significantly since rate increases began earlier this year, but not enough to prevent the need for higher rates from here on.

Powell also said the Fed doesn’t want to make the mistake of not tightening rates enough or starting to ease too soon. He might’ve had some history in mind when he said that. The Fed was criticized in the 1970s for easing rates before inflation was fully tamed.

“At some point, it will become appropriate to slow the pace of increases” as rates become sufficiently high to start bringing inflation down to the Fed’s 2% goal, according to Powell. “We’re taking forceful steps to moderate demand so it becomes more in line with supply.” Further, he warned that this could mean a “prolonged period of below-trend growth” and higher unemployment.

Ahead of today’s decision, markets had a remarkable October amid hopes the Fed might pivot and deliver a more dovish message as soon as today’s meeting. Some of the optimism was driven by a late-October article in The Wall Street Journal speculating that some members of the FOMC were growing nervous about the “pain” of higher rates on the economy and on corporations.

What About December?

Now the next question: What will the Fed do for an encore at its next meeting on December 13-14? And what will its economic projections look like then when it unveils its next “dot plot” of unemployment, inflation, and economic growth for the years ahead?

That’s a mystery for now, but investors began debating it Wednesday afternoon as they listened for clues during Fed Chairman Jerome Powell’s press conference. Based on today’s statement, there are early signs that the market thinks the Fed might now be more likely to shift away from another 75-point hike in December. The CME FedWatch Tool now shows a 60% chance of a 50-point hike in December, up from 44% yesterday. Chances of a 75-point hike fell from 50% yesterday to 35% today.

Even if the next hike is just 50 basis points—equal to half a percentage point—rising rates often bring more pain for rate-sensitive sectors like technology and real estate. Climbing rates could also weigh on the bond market, where 10-year Treasury yields (TNX) haven’t been able to find much buying interest lately at rates below 4%. The 2-year Treasury yield hit 4.54% early Wednesday after a brief drop below 4.3% last week and built on its premium to the 10-year yield. A rate inversion like this often has been associated with recessions. The financials sector got an initial boost after the Fed decision because higher rates often help banks.

However, continued signs of economic vigor in this week’s data alone put the Fed into a tough position, and analysts pointed out that despite the less hawkish statement, the Fed still has a lot of work to do. The Fed still indicated it needs to stay vigilant until it sees signs of inflation coming down. The next CPI report is November 10.

Despite any strength in the market after the Fed’s statement and decision today, investors might not want to get too giddy. The FedWatch Tool still shows about a 40% chance of rates reaching 5% by the middle of next year. And if inflation and jobs data continue to look as hot as they’ve been over the last few months, it might be hard for the Fed to slow rate hikes, especially because many market participants think the Fed was too slow to react to emerging inflation last year. That puts more pressure on Powell and company to react to inflationary data if the Fed wants to be taken seriously.

Next Up: Jobs Report Friday

Friday’s Nonfarm Payrolls Report for October could also look hotter than the Fed would likely prefer. Wall Street’s consensus for the headline jobs number is 220,000, according to Briefing.com. That’s down from 263,000 in September but still historically high. Keep an eye on Thursday’s September Factory Orders data for an early hint. If it remains strong, it might reflect growing consumer confidence as more people find employment.

Tomorrow also brings weekly initial jobless claims. Consensus stands at 225,000, according to Briefing.com, up a bit from 217,000 the previous week.

But in case you forgot, it’s still earnings season. Streaming company Roku (ROKU) is expected to report after the close today, putting focus on the slowing digital ad space. Starbucks (SBUX) is expected after the close Thursday, and investors could be watching for its holiday season forecast and any issues the company might be having with its China business.

CHART OF THE DAY: FLUTTERING AFTER FED. The U.S. 10-year yield (TNX—candlestick) and the Cboe Volatility Index (VIX—purple line) moved all over the place in the minutes following the Fed’s rate hike and statement. Initially rates eased, but they quickly rose again as Fed Chairman Powell spoke. Data source: Cboe. Chart source: The thinkorswim® platform. For illustrative purposes only. Past performance does not guarantee future results.

Subprime Days

As much as many of us would love to forget the pandemic peak months of March and April 2020, investors got another reminder of those times today when Amazon (AMZN) plunged to its lowest level since early April of that year. The stock’s market capitalization dropped below $1 trillion for the first time since that month too, and shares are down nearly 19% over the last five days, wiping out about $200 billion in market capitalization.

AMZN seems to be almost alone among its competitors with this level of suffering, for now. Its biggest cloud competitors, Alphabet (GOOGL) and Microsoft (MSFT), both fell after reporting earnings but not as dramatically. The cloud industry has been the biggest profit driver for AMZN, but unlike its cloud competitors, it also carries along a huge general store that’s suffering from the same global economic struggles as many other retailers. Worries about consumer resilience might be one reason AMZN got hit harder than MSFT and GOOGL.

In its earnings call, AMZN pointed toward inflation, rising energy costs, and foreign currency headwinds having a negative impact across all its businesses. In the cloud, its customers are suffering from some of the same issues and are cutting their budgets to save money, AMZN said last week on its earnings call with analysts. AMZN’s cloud growth last quarter was 28% overall but fell toward a mid-20% growth rate late in Q3. That led AMZN to project similar Q4 growth.

TD Ameritrade® commentary for educational purposes only. Member SIPC.

Image sourced from Shutterstock

This post contains sponsored advertising content. This content is for informational purposes only and not intended to be investing advice.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.