In the final of our three outlook notes we are going to review 2023 with an eye on the future. Rather than getting bogged down with details, we are going to discuss our differentiated perspectives on economic output, inflation, policy, equities, fixed income and other asset prices. We aren’t going to cover everything that happened, instead we are going to focus on surprising developments that will have persistent effects on the macro environment. We left the street in part to reduce constraints on writing provocative research, we hope you’ll find this note helpful as you reflect on the year that was. We appreciate all of you and wish a Merry Christmas and Happy Holidays.

Productivity Boom And Policy Bust

If you are in the generative artificial intelligence business (or stocks) it was the best of times, if you work for a bank (or are a stockholder), it was the worst of times. Well maybe not the worst of times if you work at a big bank, but nothing like the post-GFC zero rate policy regime when buying USTs at historically low yields still generated strong returns due to zero cost deposits, even with reduced leverage. Monetary policy came in like a lion, and went out like a lamb, or maybe in like a mean house cat and out like one that gets along with your dog. The Fed made two communication blunders in ‘23; the first when Chair Powell threatened a reacceleration of the tightening pace at the March Monetary Policy report to Congress, within days three banks bought a one-way ticket to FDIC resolution. The second followed the September FOMC excessively hawkish Summary of Economic Projections that increased the duration and magnitude of the tightening cycle (higher for longer), leading to an intensification of the supply-driven Treasury bear steepening correction. The biggest event of the year with the most lasting ramifications was the US reaching the fiscal limit for the second time, but this one with inflation above the Fed’s ill-fated target and the Treasury’s checking account on overdraft, making it difficult to paper over Secretary Yellen’s buyer’s strike.

As downbeat as this sounds, our 2023 outlook forecast for a complete retracement of the ‘22 S&P 500 correction from 4800 to 3500, back to the all-time highs was realized late in the year (we expected to reach 4800 in 3Q) following the FOMC October policy put, November pause and December pivot. The critical elements to our call were disinflation we described as the ‘Path from 9 to 4’, an abundant liquidity regime due to the debt ceiling impasse limiting Treasury supply, limited earnings downside risk due to resilient nominal growth, and the ‘94-’95 analog. We expected a strong first half, and more difficult second half as the disinflationary process slowed and liquidity tightened following a mid-year debt ceiling deal. We began ‘23 all in on cyclical sectors, quickly pivoted in late January back into technology and related sectors after 4Q22 earnings accelerated the recovery in earnings revision momentum. We downgraded banks following the March FOMC meeting when the FOMC plowed ahead despite the bank failures on the theory that the problem was idiosyncratic and could be resolved with macro-prudential policies. The FOMC’s determination to increase the policy rate above 5%, despite the deepest yield curve inversion since the Volcker Fed triggered a chain of events that ended destroyed the thrift (Bailey Building & Loan) industry that supplied 80% of mortgage credit, led to the second largest contraction in bank credit in 50 years.

The disinflationary process exceeded our expectations. A modest contraction in earnings and the corporate input to our preferred measure of economic output, gross domestic income, confirmed our view that earnings contractions during periods of elevated inflation are shallow, however, the deep curve inversion and credit contraction was a crucial divergence from the ‘95 analog when the equity market had a broad-based advance led by technology with banks not far behind.

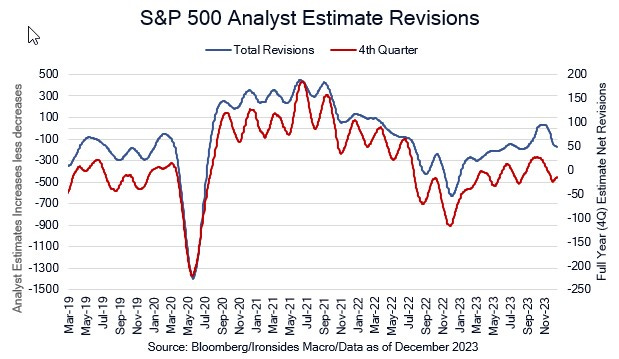

As we review 2023, our perspective is driven by our view that economic output drives corporate earnings, but only played a tertiary role in the level of interest rates through policy channels, supply, real rates or term premium. Inflation was the dominant factor in the monetary policy channel of rates in 2023, until September through the December FOMC meeting pivot. The primary explanatory variable in the expansion of equity market multiples in ‘23 was the rate of change of earnings growth; in other words, increasing net revisions from November ‘22 through October ‘23. If you are skeptical of our perspective, consider sector relative performance: consumer discretionary, technology, communication services net revisions drove the recovery, and those sectors massively outperformed the other 8 sectors. The final year-end push higher was driven by the FOMC pivot, which begs the question, will conditions develop that facilitate a broadening of the advance? The fixed income market round trip was all about policy, while most of the focus is monetary policy, There's a New Sheriff in Town, the US Treasury and management of the highest levels of debt relative to the size of the economy since WWII.

Figure 1: Are revisions about to turn back higher? Tech and related sectors are falling, cyclicals are driving the stabilization.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.