Stocks made new record highs, with the S&P 500 reaching a closing high of 5,026.61 and an intraday high of 5,030.06 on Friday. For the week, the S&P gained 1.4%. The index is now up 5.4% year to date and up 40.5% from its October 12, 2022 closing low of 3,577.03.

Coming into 2024, Deutsche Bank and Societe Generale were among a handful of banks whose economists were calling for a recession in 2024.

Last week, they both pulled that call.

“When we first adopted a mild recession as our baseline forecast, a key element was that, with an economy far from the Fed's objectives, the history of central bank-induced disinflations showed the path to a soft landing was narrow if not unprecedented. We now think the economy will land on this narrow path and that a recession will be averted with limited cost in the labor market.” - Deutsche Bank’s Matthew Luzzetti, Feb. 5

"We no longer anticipate the mild recession for 2024 that we had expected for nearly a year. Gains in jobs and consumer spending may be moderating, but they are not signaling problems ahead." - Societe Generale’s Stephen Gallagher, Feb. 7

The banks’ revised views follow a slew of better-than-expected economic reports released since the beginning of the year. (Read more about them in TKer’s weekly review of macro crosscurrents here, here, here, here, and below.)

While the data in aggregate continues to confirm the economy is in pretty good shape, some of the data show it isn’t quite as hot as it used to be.

Upgrade to paid

Debt Delinquencies Rise

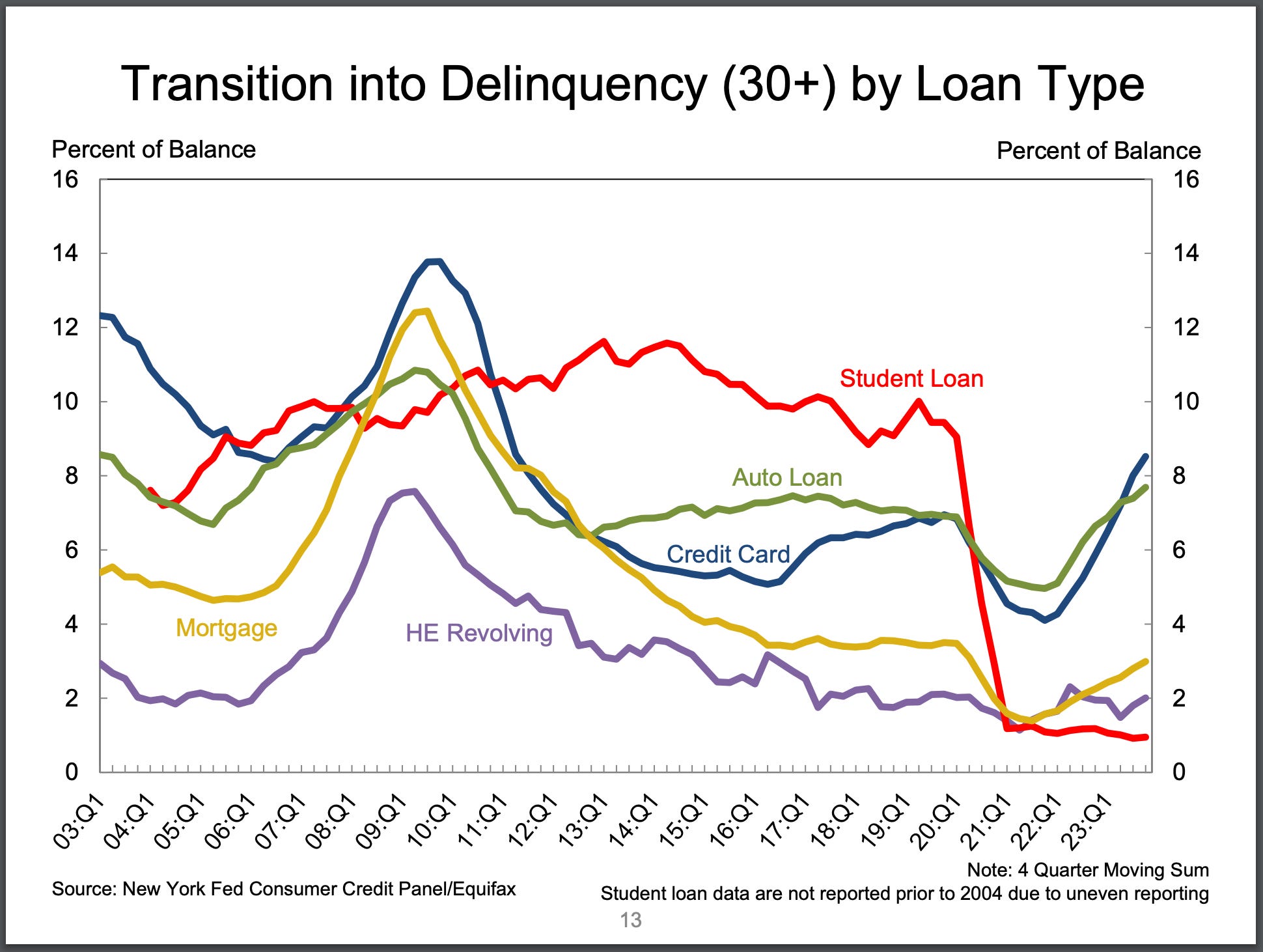

One set of metrics that has been deteriorating over the past couple quarters is debt delinquency rates. (More on this here, here, here, here, here, and here.)

According to the New York Fed’s Q4 Household Debt and Credit (HHDC) report, the share of debt newly transitioning into delinquency continued to rise for most forms of borrowing.

“Annualized, approximately 8.5% of credit card balances and 7.7% of auto loan balances transitioned into delinquency,” the New York Fed observed. “Early delinquency transition rates for mortgages increased by 0.2 percentage point yet remain low by historic standards.“

Balances transitioning into delinquency are rising. (Source: New York Fed)

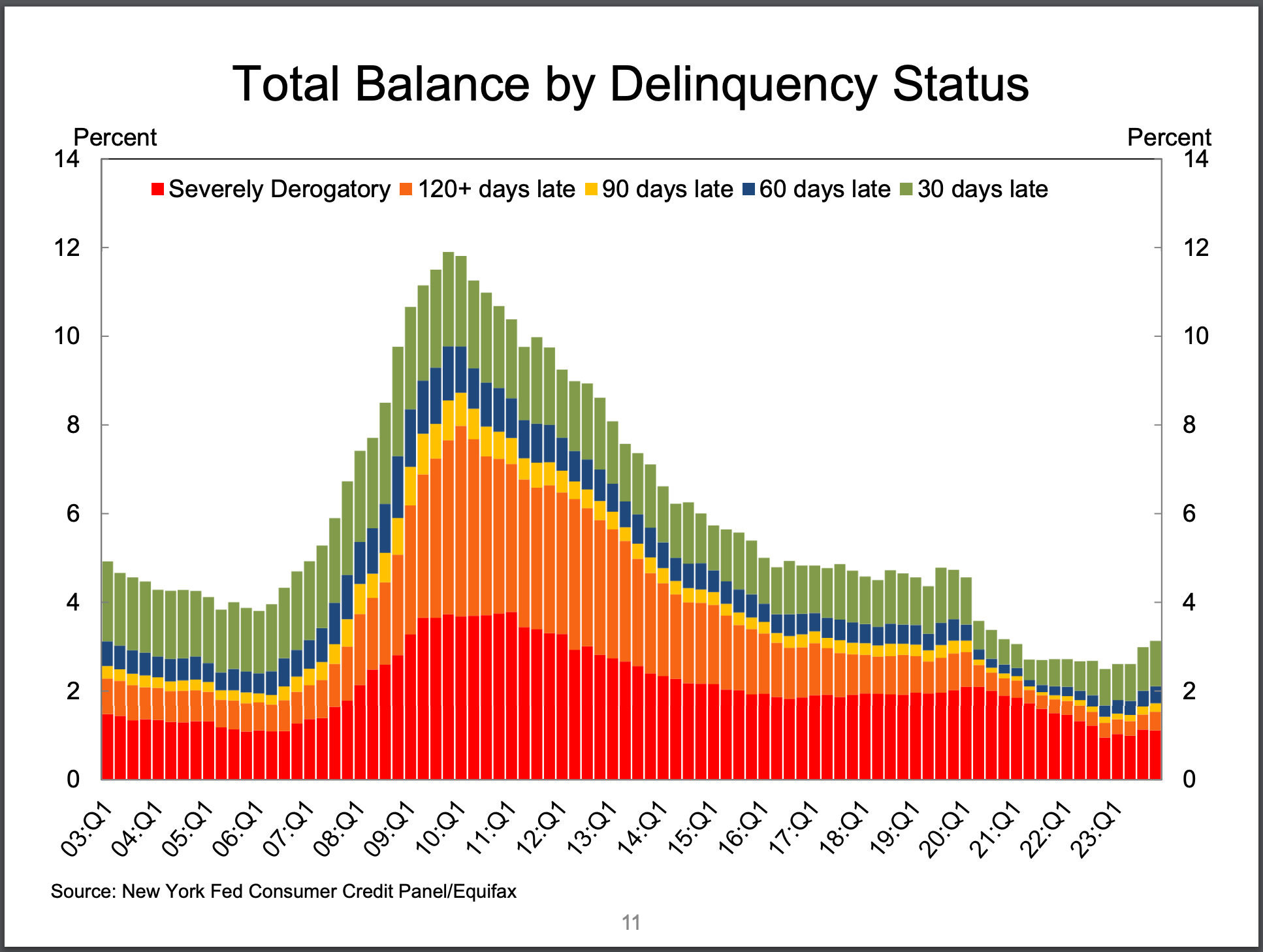

When you consider all outstanding debt, the delinquency rates, while rising, continue to reflect a normalization back to prepandemic levels.

In other words, while the “flow” into new delinquency has been picking up, the “stock” of delinquencies remains below prepandemic levels.

“As of December, 3.1% of outstanding debt was in some stage of delinquency, up by 0.1 percentage point from the third quarter,” New York Fed researchers wrote. “Still, overall delinquency rates remain 1.6 percentage points lower than the fourth quarter of 2019.“

Total balances in delinquency are relatively low. (Source: New York Fed)

So while debt delinquency rates have deteriorated, absolute levels of debt delinquencies aren’t too bad.

“It's maybe not a flashing red signal but something that is indicative of a slight weakening in household balance sheets that is consistent with a slowdown in consumption,” New York Fed researchers said on a call with reporters.

It’s also worth keeping in mind that cooler economic activity has been an aim of the Federal Reserve in its ongoing effort to bring down inflation. (More here and here.)

About ‘Record High’ Credit Card Debt

There continues to be a lot of attention on credit card balances. Here are some headlines from the past week reporting on the New York Fed’s data:

Americans' credit card debt hits record $1.13 trillion - ABC News

Americans owe a record $1.1 trillion in credit card debt, straining budgets - CBS News

Credit card debt hits a ‘staggering’ $1.13 trillion. - CNBC

Credit card debt smashed another record high at the end of 2023 - Fox Business

Credit card debt passes $1 trillion. Here’s a payoff playbook. - Washington Post

While these headlines are accurate and it is true that delinquency rates have been ticking up, there is much-needed context.

Credit card balances are up. (Source: NY Fed)

“All of these debts are nominal figures,” New York Fed researchers explained. “As price changes, naturally most of our debt figures are going to tend to be all time high. … If we were to report these as a percent of personal income or adjusted for CPI, I don't think that you would see these kinds of all time highs.”

Upgrade to paid

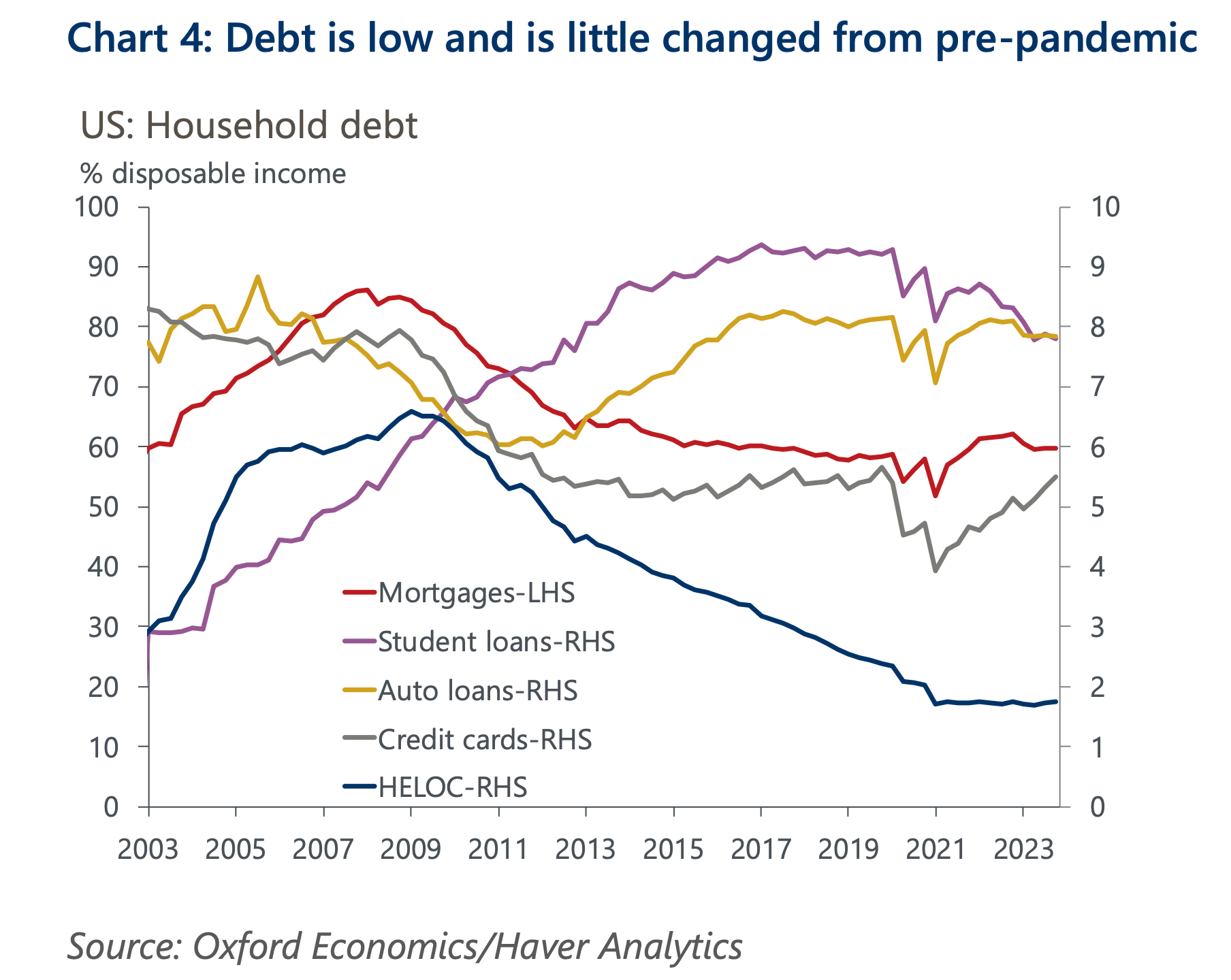

Indeed, as the chart below from Oxford Economics shows, credit card debt as a percent of disposable income (gray) is not abnormally high.

Credit card debt levels aren’t actually very high. (Source: Oxford Economics)

“Every category of consumer loan is now smaller relative to disposable incomes than before the pandemic,” Oxford Economics’ Michael Pearce wrote on Thursday. “That is true even for credit card debt that, despite rising at a solid pace in recent years, remains below its Q4 2019 level as a share of incomes.”

More timely data from Bank of America confirm that credit card activity also does not reflect a financially stretched consumer.

“Two metrics to measure consumers’ ability to borrow for everyday spending are the share of current spending they are financing on credit as opposed to debit cards and the degree to which they are spending close to their credit limits,” Bank of America analysts wrote on Thursday. “On the first of these, Bank of America internal data suggests that the share of spending on credit cards, while rising since 2020, is no higher than it was in 2019. On the second, the average credit card utilization rate (credit card balances relative to credit limits) remains below 2019 levels.

Bank of America clients aren’t maxing out their credit cards. (Source: Bank of America)

The Big Picture

Metrics like debt delinquencies suggest things are relatively worse than they were during the hottest periods of the current economic expansion. It’s a normalization that’s to be expected in the Fed’s efforts to bring down inflation.

But the absolute levels of most metrics suggest the economy continue to be generally good — further confirming we are experiencing a bullish “Goldilocks” soft landing scenario where inflation cools to manageable levels without the economy having to sink into recession.

A version of this post was originally published on Tker.co.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.