Stocks closed higher last week with the S&P 500 SPY rising 1.6%. The index is now up 9.2% year to date, up 17.2% from its October 12 closing low of 3,577.03, and down 12.6% from its January 3, 2022 record closing high of 4,796.56.

As worries about recession risks linger, the focus last week shifted to the consumer. Remember: Personal consumption accounts for about 71% of GDP.

Good news: Personal consumption is holding up!

According to Census Bureau data, retail sales in April climbed 0.4% to $686.1 billion.

Retail sales rose and continues to trend near record levels. (Source: @USCensusBureau)

While the pace of sales is off its record high, it continues to trend well above pre-pandemic levels.

“Not to take issue with a popular coffee ad, but America runs on consumer spending,” JP Morgan economist Michael Feroli wrote Friday. “And consumer spending continues to run in the right direction, as this week’s strong April retail sales report confirmed.”

None of this should be very surprising to TKer readers. As we’ve discussed repeatedly, consumer finances have been in remarkably good shape despite what weak sentiment may suggest. And robust demand for labor continues to fuel job creation. All of this represents massive tailwinds powering spending, which has been bolstering economic growth for months.

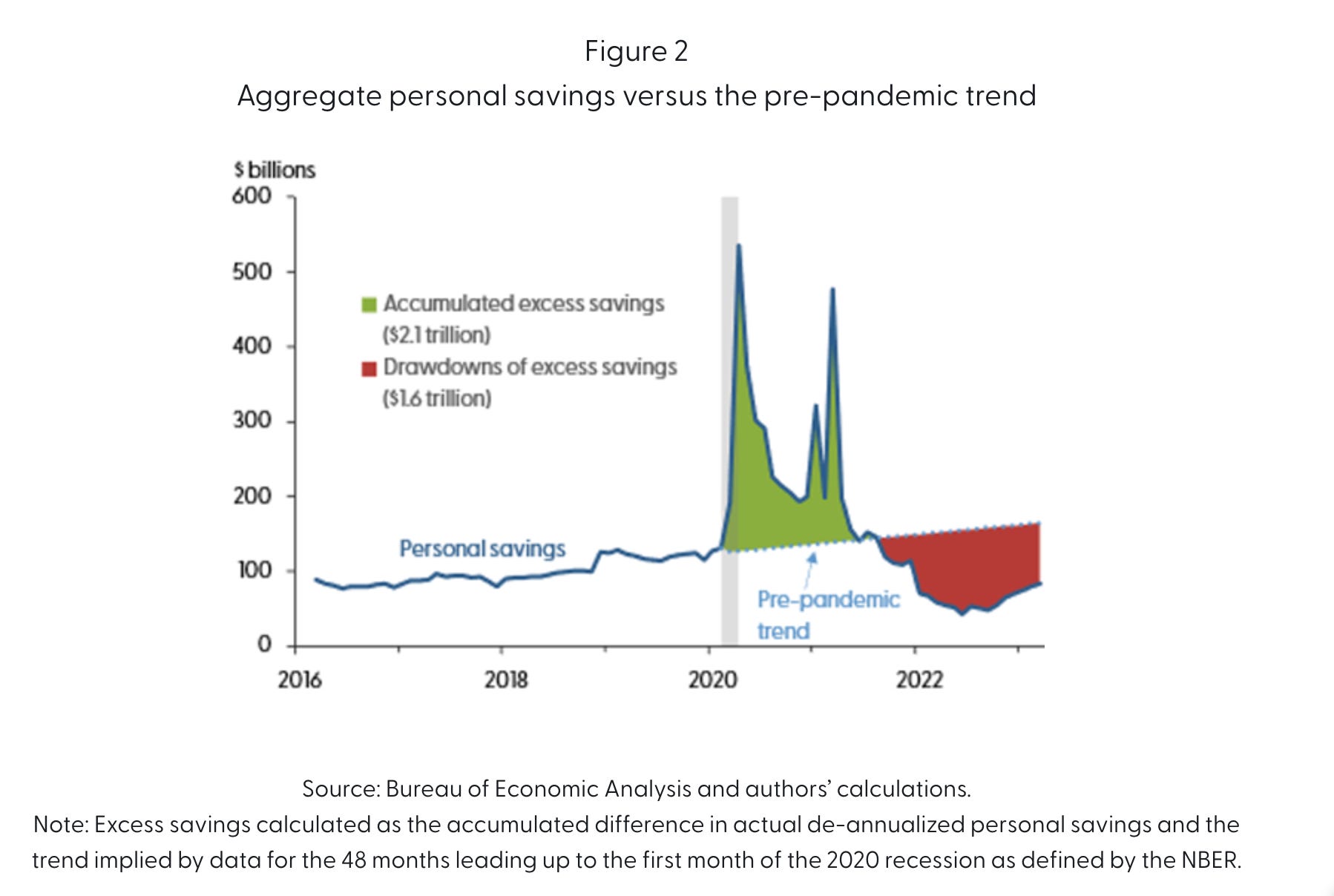

Just last week, San Francisco Fed researchers estimated consumers were still collectively sitting on $500 billion in excess savings — the extra cash consumers piled up since February 2020, thanks to a combination of government financial support and limited spending options during the pandemic.

Excess savings are helping to power spending. (Source: San Francisco Fed via TKer)

“The consensus expects a recession starting next quarter, but the upside risk to this negative forecast is that consumers still have plenty of savings left,” Torsten Slok, chief economist at Apollo Global Management, wrote on Tuesday.

For more on the consensus expectation for a recession, read: Why Warren Buffett ignores economic forecasts 🙉

Resilient, But Cooling

This is not to say that economic growth hasn’t been cooling. Indeed, the Federal Reserve’s campaign to fight inflation by tightening financial conditions and slowing growth has been effective.

And while aggregate retail sales grew, some categories — including electronics, furniture, and general merchandise — saw declines.

Retailer earnings, meanwhile, have been a bit mixed. Last week, Walmart reported strong sales growth whereas Target sales growth was lackluster and Home Depot sales fell.

Berkshire Hathaway CEO Warren Buffett warned earlier this month that most of his many companies expected to report lower earnings this year. In addition to weaker demand, Buffett said many of his companies would be selling goods at unfavorable prices as they clear out excess inventory.

“It is a different climate than it was six months ago, and a number of our managers were surprised,“ Buffett said. “We'll start having sales at places where we didn't need to have sales before.”

Cambiar a la suscripción paga

Consumer finances are normalizing 📉

While consumer finances have been strong, they have been normalizing.

The San Francisco Fed suggested that the $500 billion in estimated excess savings could dwindle by Q4 of this year, depending on how quickly consumers draw them down.

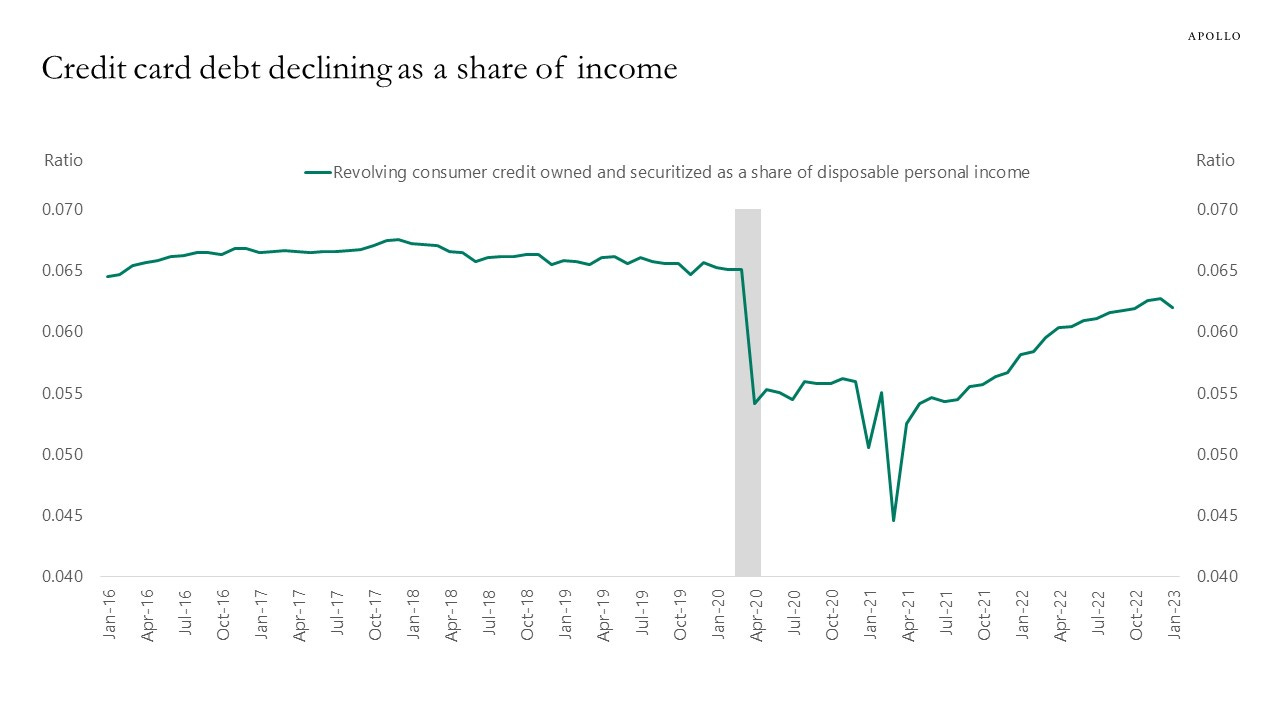

And credit card balances have been on the rise. While they remain low relative to disposable income, these metrics have been trending higher.

Credit card debt is up, but relatively manageable. (Source: Apollo Group, via TKer)

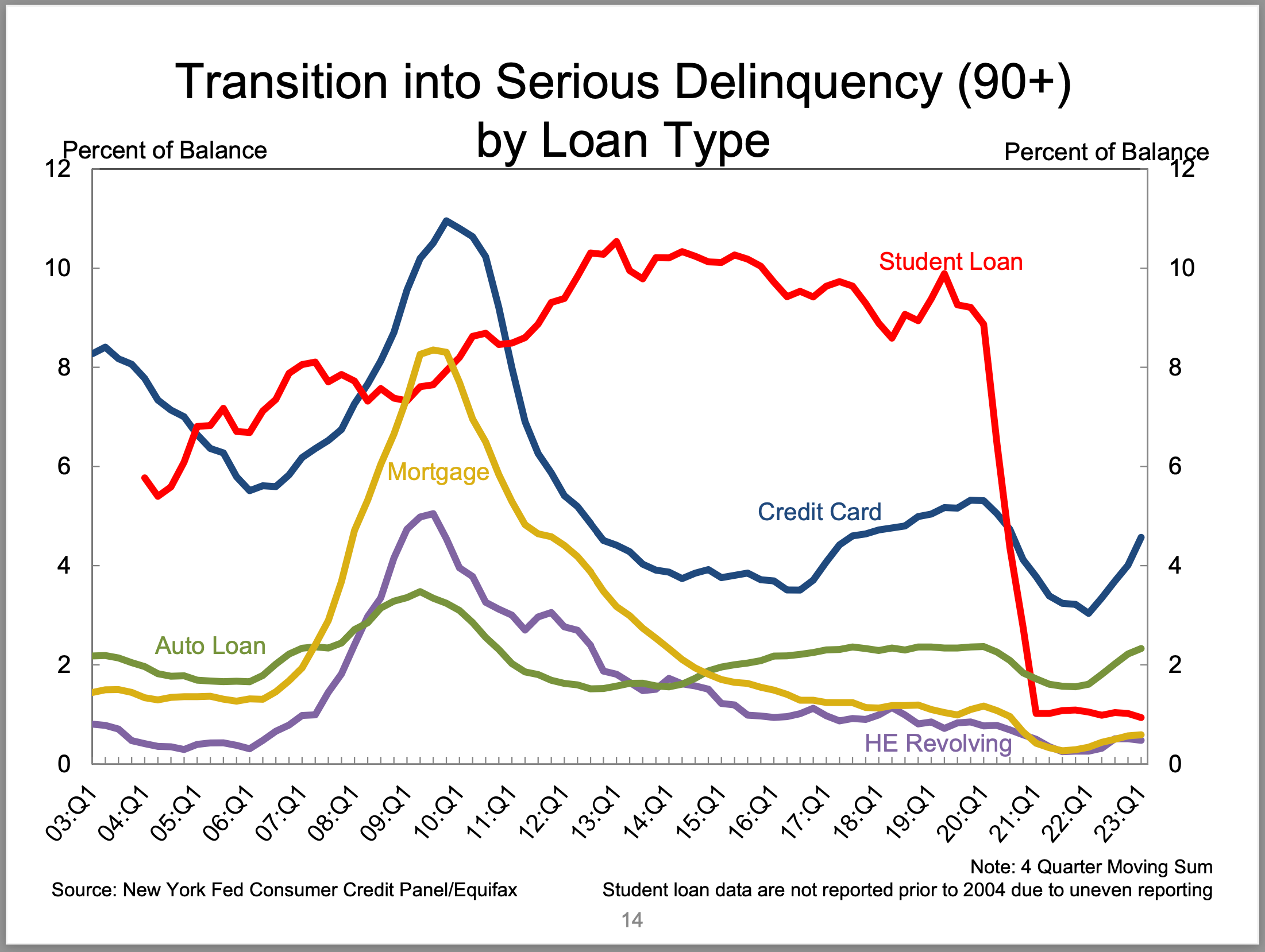

Meanwhile, the New York Fed’s Q1 Household Debt & Credit report shows debt delinquency rates are up from their lows. From the report (emphasis added):

Aggregate delinquency rates were roughly flat in the first quarter of 2023 and remained low, after declining sharply through the beginning of the pandemic. As of March, 2.6% of outstanding debt was in some stage of delinquency, 2.1 percentage points lower than last quarter of 2019, just before the COVID-19 pandemic hit the United States.

The share of debt newly transitioning into delinquency increased for most debt types. Transition rates into early delinquency for credit cards and auto loans increased by 0.6 and 0.2 percentage points, following similarly sized increases for the past year. Delinquency transition rates for mortgages upticked by 0.2 percentage points. Those for student loans have remained flat, as the federal repayment pause remains in place.

Delinquencies are up, but below historical levels. (Source: NY Fed)

The number of consumers with a bankruptcy notation ticked up in Q1, but the level remains below the pre-pandemic trend.

Bankruptcies are below historical levels. (Source: NY Fed)

Again, all of this is a discussion about normalization. The evaporation of excess savings only means savings levels would have returned to the pre-pandemic trend level. Same with rising delinquencies: they’re rising, but they’re mostly gravitating back to the pre-pandemic trend.

The Big Picture

Economic recession remains at bay thanks to an increasingly employed American consumer with a strong balance sheet.

Yes, recession risks are up as the Fed actively tries to slow the economy.

But the macro tailwinds bolstering the economy seem likely to keep growth going.

And even if the economy does slip into recession, keep in mind that many metrics are at historically strong levels. In other words, a recession could mean the economy goes from being very strong to just slightly less very strong, with limited risk of the bottom falling out thanks to what continues to be a lot of excess demand in the economy.

A version of this post was originally published on Tker.co

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.