COVID-19 (more commonly known as coronavirus) has ushered us in a full-fledged health crisis and an economic crisis; however, we are not yet fully submerged into a financial crisis. While the Global Financial Crisis (GFC) of 2008-2009 witnessed a pronounced and prolonged dislocation of the financial system, thus far COVID-19 has not drastically displaced our ecosystem enough to plunge us head-first into a complete setback. While the COVID-19 crisis has likely placed us ankle-deep in the waters of a financial crisis, stimulus measures from the Federal Reserve may subside the financial floodwaters.

While there is not a playbook available for navigating recessions induced by global pandemics, the US Government is drawing upon valuable lessons learned during the GFC and is responding quickly and aggressively. If past outbreaks are any indication, then COVID-19 should largely be contained by the first half of 2020. Many analysts anticipate a strong rebound in the markets by the second half of the year.

With that being said, it is important to note that the commercial real estate (CRE) sector does not mirror the stock market in terms of recovery and movement. CRE is slower moving and the leasing fundamentals do not swing broadly from day-to-day. Certainly, if the virus has a sustained and material impact on the broader global economy, it will have reciprocal impacts on CRE as well. However, it is still too early to gauge the longer-term impact.

Below, we'll break down the impacts of COVID-19 on capital markets, the various property types of commercial real estate, and the macro trends that we are seeing it influence.

CARES ACT

On March 27, the Coronavirus Aid, Relief, and Economic Security (CARES) Act was enacted. The scale of the stimulus package is unprecedented at $2.3 trillion (equivalent to nearly 11% of US GDP). For context, the 2009 American Recovery and Reinvestment Act was about $800 billion, or 5% of US GDP.

The CARES Act provides financial assistance in three key areas:

- The Paycheck Protection Program which authorizes up to $349 billion in forgivable loans to small businesses to pay their employees and cover most operating costs including rent;

- Direct payments to taxpayers which are forecast to begin to be delivered in late-April/early May; and

- Additional unemployment benefits averaging approximately $400 per week.

DEBT MARKETS

Quick action from the Fed is immensely helping keep the credit markets afloat. However, the markets are becoming increasingly volatile. The adage emerging in the market seems to be “If you have a deal in hand — take it.” Read on to see how the individual debt markets are responding to the crisis.

RESIDENTIAL MORTGAGE MARKET

Mortgages for conforming home loans remain available, however down payment and credit requirements continue to increase. For instance, JPMorgan recently announced they will require a minimum 20% down payment and a borrower credit score of at least 700 for new residential mortgages. Nonconforming or “jumbo” mortgages are increasingly difficult to obtain as are “non-qualified mortgages” (those that do not meet criteria for government purchase). Wells Fargo recently suspended its purchasing of nonconforming residential mortgages, though its direct-to-consumer business remains selectively active. Cash-out refinances and home equity loans are on pause for most traditional lenders.

COMMERCIAL MORTGAGE MARKET

The commercial mortgage market varies widely by type of lender and by property type. Interest rate volatility is impacting lenders who remain in a phase of ‘price discovery’ and lenders are struggling to price assets. Hospitality and retail are especially challenging loans for all lenders. Agency financing (Fannie Mae, Freddie Mac, FHA/HUD) stands out as the most active source of CRE debt, being supported by the government’s commitment to the residential market.

However, even the agencies are experiencing some issues in navigating the market, limiting forward commitments to interest rates amidst market uncertainty. Insurance companies are still active, albeit very selectively. With ample liquidity being provided by the Fed, banks also remain active, though focusing on relationship lending, increasing covenants, and tightening underwriting standards.

There is virtually no current lending activity in the CMBS market with bonds being too volatile to price in the secondary market. All others including non-bank lenders, mortgage REITs, debt funds and specialty finance companies are by-and-large out of the market, with many experiencing their own liquidity issues and margin calls, though some private funds do remain active.

MORATORIUMS & FORBEARANCE

On the residential side, the CARES Act allows impacted homeowners with federally backed loans to delay paying their mortgage and get a break on accumulating interest for up to a year. However, an unintended consequence, while mortgage servicers are granting the payment deferrals to borrowers with no questions asked, as is required by the law, the servicers are still contractually obligated to pay the underlying mortgage bondholders.

On the multifamily side, things are a little clearer. Within the CARES Act, mortgage loan forbearance for up to 90 days is provided to multifamily landlords with agency debt (Fannie Mae or Freddie Mac). Though the specifics are still being clarified, the programs generally allow pre-packaged mortgage forbearance with certain conditions such as suspending evictions. This should provide significant near-term relief as the agencies account for nearly half of all multifamily loans in the US.

For non-agency debt, the scenario is more nuanced, with provisions established lender-by-lender and perhaps case-by-case; this is true not just for landlords but also for homeowners. The good news is that Federal bank regulators have extended flexibility to local banks to provide forbearance and modification options to borrowers in need.

However, to further complicate matters, at least 85 individual, local, and/or states have issued their own eviction moratoriums which may contain differing provisions than required by lenders. Learn more about the individual state standards here.

TRANSACTION VOLUME

RESIDENTIAL

A recent study by Realtor.com examined a sample of 106 counties and found a rapid and pronounced change in the for-sale residential market. In the 10 weeks prior to the COVID-19 onset, through the week ending March 8, sales in this sample were up 15% year-over-year on average. However, by the week ending March 29, home sales for this sample were down 30% year-over-year. In the same study, new listings experienced a sharp decline as well. In the two weeks ending March 29 and April 5, the volume of newly listed properties decreased by 34% and 31% year-over-year respectively. The study anticipates even larger and more widespread declines for April, further supported by a recent Mortgage Bankers Association survey for the week ending March 27, which showed mortgage purchase applications down 11% from the prior week and down 24% over this time last year.

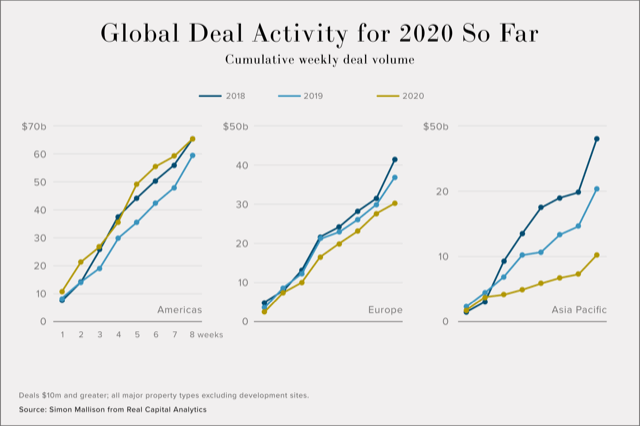

The Commercial Real Estate (CRE) industry reports most data on a quarterly basis, thus the actual impact of COVID-19 on the property markets is still being calculated. With relatively long sales processes, private CRE also tends to lag the public equity markets where the market impact is more immediate. However, in Asia Pacific, where COVID-19 has had more time to impact the markets, CRE transaction volume is down 50% for the first eight weeks of 2020. We would expect second-quarter 2020 US CRE transaction volume to be down in a meaningful way as buyers and sellers alike take a “wait-and-see” approach.

If the virus is contained in relatively short order, a rebound in the second half of 2020 is likely. Like any asset class, CRE performance is cyclical and investment has fluctuated during previous recessions and crises. However, CRE remains one of the few investments which provided the combination of a hard asset and inflation hedge while potentially producing meaningful current income. According to a recent publication by global CRE services firm JLL, the spread between CRE yields and government bond yields remains at or near all-time highs. Thus, it is expected that the COVID impact on CRE yields is minimal and that capital allocation to CRE remains stable or potentially increases.

IN SUMMARY

The immediate impact has been quick and easily recognizable. However, second- and third-order effects are harder to anticipate and not yet fully realized. All markets will be impacted by indirect effects, though to what degree is harder to predict.

However, considering the US government’s proactive and aggressive monetary, fiscal, and policy measures, paired with the Federal Reserve System’s “whatever it takes” response, the economic ramifications of COVID-19 are expected to be dampened. The final result, however, depends heavily on how well the government and central banks can limit the damage — along with the individual microeconomic responses from the financial sectors. As a result, it is difficult to assess with certainty the scale of COVID-19’s impact on real estate transactions.

To read our coverage of the impact of COVID-19 on individual sectors, click on the links below:

- Healthcare, hospitality, and senior living

- Office, self storage, and industrial

- Retail

- Student housing

- Multi-family

Full disclosure. The information provided here is not investment, tax or financial advice. You should consult with a licensed professional for advice concerning your specific situation.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.