Homeowners insurance helps protect homeowners from life’s uncertainties. This insurance policy covers your property, liabilities for injuries, and other parts of your home. It’s no surprise people pay homeowners insurance. Lenders can force borrowers to have insurance, and it’s a helpful safeguard. Most homeowners want to protect other valuables, such as their jewelry. Below, Benzinga discusses whether insuring jewelry works for homeowners.

How is Jewelry Covered by Home Insurance?

Home insurance policies cover your jewelry but only up to a certain amount. If your jewelry gets stolen, your insurer will assess the jewelry’s value. Then, the insurer will replace the jewelry up to its value or your insurance policy’s limit, whichever is lower. Some insurers have lower limits for stolen jewelry than damaged jewelry.

When Is Jewelry Covered By Homeowners Insurance?

Homeowners insurance provides jewelry coverage under various scenarios. You can qualify for a replacement under these circumstances:

- Jewelry theft

- A natural disaster destroys jewelry and other items in your home

- Vandalism

- Damages

How Much Jewelry Does a Home Insurance Policy Cover?

Home insurance providers can cover expensive jewelry, ranging between $1,000 and $2,000. These caps represent the maximum an insurer will pay to give you a replacement. You will have to cover every dollar that exceeds this cap which can be a substantial out of pocket expense for items worth more than a couple of thousand dollars. You can usually get coverage for more expensive jewelry through a floater to a homeowners policy, but this additional coverage will result in higher premiums.

3 Ways to Increase Your Coverage on Jewelry

Homeowners insurance is a starting point for jewelry insurance, but it may not sufficiently cover your collection. Jewelry owners can get more coverage for their prized possessions with these strategies.

Raise the Sublimits in Your Policy

Sublimits are separate limits in an insurance policy. Insurers may have lower limits for jewelry theft than damaged jewelry. Some homeowners insurance companies will let you raise these limits. However, you may have to pay higher premiums because insurers incur more risk when raising sublimits.

Coverage Endorsements

Coverage endorsements expand the scope of your homeowners insurance policy. You can add one of these endorsements to your policy to cover additional jewelry insurance. You can get endorsements for other scenarios, but each endorsement will increase your monthly premiums. A coverage endorsement can provide enough protection to compensate for lost or stolen jewelry.

Specialty Jewelry Insurance

Some homeowners insurance policies do not have enough coverage for your jewelry collection. Some people seek a standalone or specialty jewelry insurance policy to cover any gaps in their home insurance. Specialty jewelry insurance can provide additional protections and may not require a deductible. If you do not want to pay a deductible, you will likely have to pay higher premiums than a plan with a deductible.

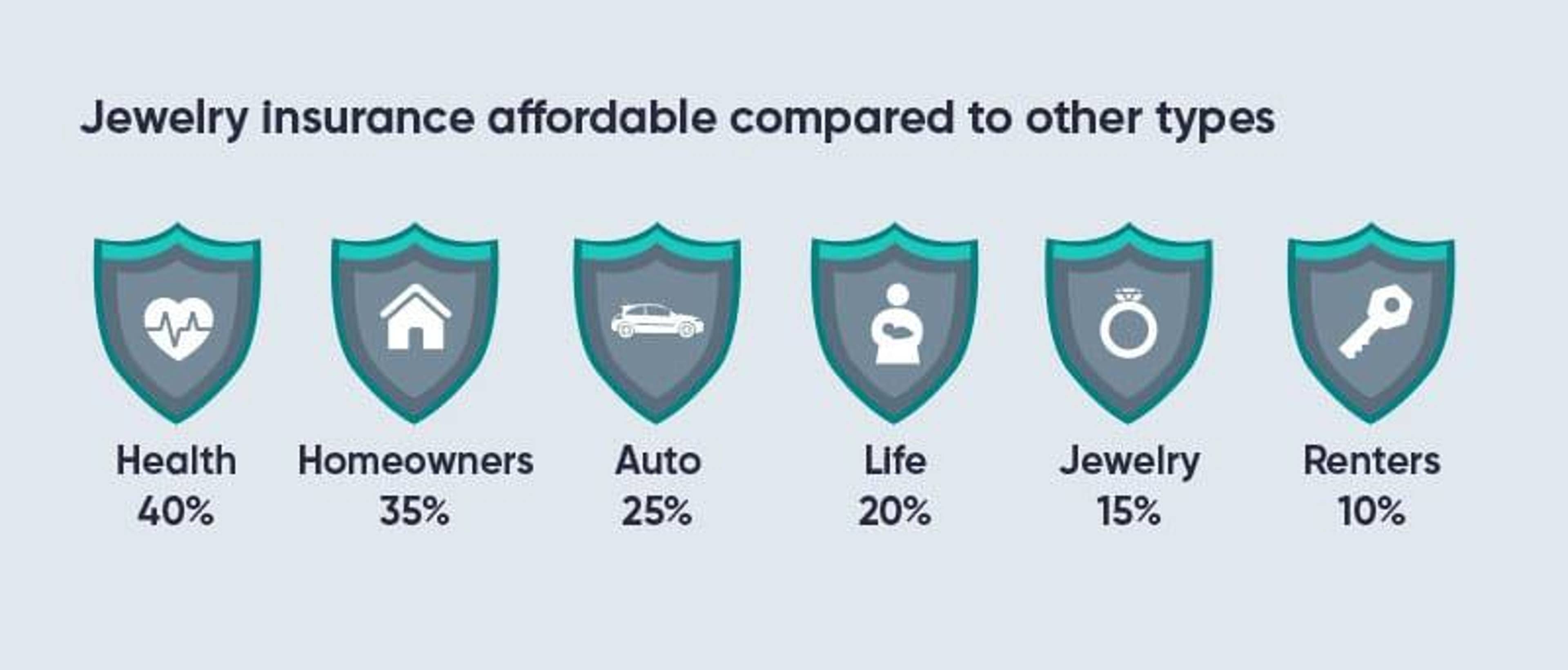

Why Home Insurance Might Not Be the Best Choice To Cover Your Fine Jewelry

Home insurance can help you protect basic jewelry, but it will fall short for more expensive items. Home insurance policies don’t typically offer high enough caps or broad enough protections for fine jewelry and high-end engagement rings. Some people may not have enough money to replenish their collection if something happens. These people would benefit the most from jewelry insurance because it offers extra safeguards. The insurer will replace your jewelry instead of you footing the bill.

Specialty jewelry insurance should cover loss, theft, damage, and what’s known as “mysterious disappearance.”. Homeowners insurance may not cover all these situations nor their associated costs. You also may not get a suitable replacement stone if you’re required to replace it from a preferred network specified by your homeowners insurance company.

Home Insurance Rates and Deductibles Keep Going Up

As home insurance policy premiums keep increasing, especially in areas where hurricanes, tornadoes, and wildfires happen, many homeowners are also facing higher deductibles just to keep premiums down. Unbundling fine jewelry insurance from a homeowners policy can make jewelry coverage more affordable, minimize or eliminate deductibles and reduce the risk of getting a home insurance policy canceled if a claim is made.

Get a Quote for Your Jewelry Insurance

You can continue using homeowners insurance for some jewelry coverage, but it probably won’t be enough for your fine jewelry. BriteCo offers specialty jewelry insurance policies that match your needs and concerns with replacement coverage up to 125% of the appraised value and no deductibles. You can get a free custom quote online in 60 seconds to see how much coverage for your fine jewelry will cost.

Frequently Asked Questions

Does jewelry insurance cover missing diamonds?

Jewelry insurance can cover missing diamonds, depending on your insurance policy and the diamond’s cost.

What should you do when you lose expensive jewelry?

Retrace your steps and try to remember where you may have lost the jewelry. After finding the jewelry or getting a replacement, you may want to consider jewelry insurance for future protection.

What happens if you lose an insured ring?

A specialty jewelry insurer will provide a replacement — sometimes of greater monetary value than the ring you lost.