(Friday Market Open) Equity index futures are pointing to a higher open after yesterday’s massive sell-off sparked by several central banks raising key rates.

Potential Market Movers

Fed Chairman Jerome Powell will step in front of a microphone later today at a Federal Reserve-sponsored conference. His speech at the Inaugural Conference on the International Roles of the U.S. Dollar will likely offer Powell a chance to address how other central banks have to the Fed’s rate hike on Wednesday, and how they’ve moved to protect their currencies from the rising strength of the U.S. dollar.

The dollar is bouncing back this morning with the U.S. Dollar Index ($DXY) rising 0.84% despite the 10-year Treasury yield (TNX) falling nearly nine basis points before the opening bell. The 10-year yield has dropped back to 3.22%.

Yesterday’s selloff may have been a bit overdone based on the bounce back in equity futures this morning. However, the bounce is unlikely to be a risk-on event. It’s more possible that investors may feel some extra volatility because it’s a triple witching Friday as options contracts expire potentially causing some liquidity issues before the close. Additionally, many traders will likely liquidate positions ahead of the three-day holiday weekend. U.S. markets will be closed on Monday for the Juneteenth holiday.

There are a couple of stocks making news this morning. Roku (ROKU) rallied 3.91% during Thursday’s after-hours trading in reaction to an exclusive deal with Walmart (WMT) allowing viewers to browse, shop, and purchase directly from their Roku-equipped TVs.

Also, Adobe (ADBE) reported better-than-expected earnings and revenue but provided weak forward earnings guidance causing the stock to fall 2.25% in extended-hours trading. ADBE had already fallen to its lowest level in two years before the announcement.

U.S. Steel (X) issued a positive change in earnings guidance, adjusting its quarterly forecasts for EBITDA to $1.6 billion. X rallied 6.44% in premarket trading.

Reviewing the Market Minutes

Bears continued their attack Thursday with the S&P 500 (SPX) falling 3.25%, taking it nearly 24% from its all-time high. The Nasdaq Composite ($COMP) plunged 4.08% for the day, finishing off 34% from its high. The sell-off was triggered by the Swiss National Bank (SNB) and the Bank of England (BoE) following the Federal Reserve’s 75-basis-point rate hike on Wednesday. The SNB’s hike was a surprise and its first since 2007, moving its benchmark from -0.75% to -0.25%. The BoE’s hike was its fifth consecutive monthly increase, taking its key rate up to 1.25%.

In fact, within a few hours after the Fed raised its benchmark rate, hikes followed in Brazil as well as several gulf central banks including Saudi Arabia, Kuwait, United Arab Emirates, Qatar, and Bahrain.

In the last six months, nearly four dozen central banks have raised interest rates according to The New York Times. While many of these banks belong to much smaller countries and many of these countries try to peg their currency with the U.S. dollar, it paints a picture of inflation that is much worse than many had originally forecast. Their moves also highlight a need to protect their respective currencies from the recently advancing strength of the U.S. dollar.

The rate hikes apparently worked. On Thursday, taking the U.S. Dollar Index ($DXY) 1.28% lower and back below its May highs. In the past few months, weakness in the dollar has helped multinational companies that have been hurt by currency headwinds. However, with no sign of slowing inflation and rates rising, there’s a greater likelihood of recession, which will likely be a drag on stocks.

In the consumer arena, rising rates have taken the average 30-year mortgage rate above 6% this week. That’s bad news for the housing market, which saw a few more negative reports on Thursday. Building permits fell 7% in May and housing starts dropped 14.4%, reflecting continued weakness in the in new homes market. The S&P Homebuilders Select Industry Index fell 6.66% yesterday, taking it 40% from its all-time high set back in December.

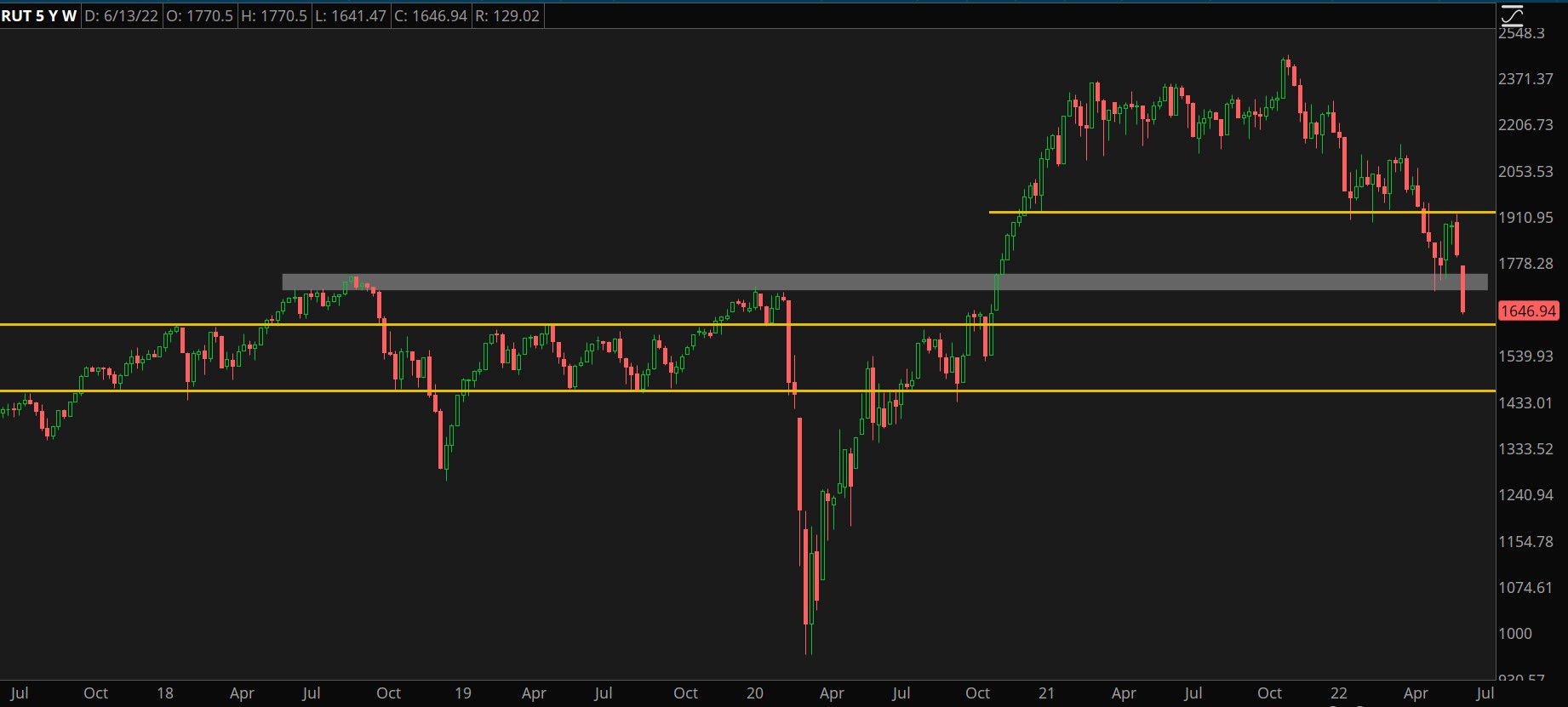

CHART OF THE DAY: BIG MOVES, SMALL STOCKS. Looking at a five-year weekly chart, the Russell 2000 (RUT—candlesticks) broke an important support level on Thursday by falling below its 2019 and 2020 highs. Levels of support appear to exist around the 1,600 and 1,450 levels. Data Sources: ICE, S&P Dow Jones Indices. Chart source: The thinkorswim® platform. For illustrative purposes only. Past performance does not guarantee future results.

Three Things to Watch

Small Blocks: Investors trying to determine a market bottom will likely need to see a bottom form on the Russell 2000 (RUT) before they’ll see one for the S&P 500 (SPX). However, current economic conditions aren’t generally in favor of smaller companies. First, if other central banks are successful in strengthening their currencies, it’ll weaken the dollar longer-term. A weaker dollar tends to mainly benefit large- and mega-cap companies because they tend to be multinationals that are doing business overseas.

Second, smaller companies also have a harder time absorbing higher input costs from inflation and/or passing on higher costs to customers because of the lack of pricing power.

Third, rising rates mean that the days of easy credit and enthusiastic investors are probably behind us at least for a while because investors are demanding more for their money. Newer, smaller companies need to offer more than a cool idea; they need to show they can make money.

So, a market bottom for companies small and large, is unlikely to happen until the inflation picture improves.

Housing Repairs: While the housing market has softened, increased weakness could compound the current recessionary picture because so many Americans have the majority of their wealth tied up in their homes. If home prices start declining, people will likely feel less financially secure and therefore consume less, which in turn will hurt home sales. Also, falling prices could prompt real estate speculators to sell their inventory pushing housing prices down even further, recalling the 2008 housing bear market. Finally, fewer new homes mean less work for contractors and construction workers. These are just some of the issues that likely figured into yesterday’s sell-off.

Downward GDP: The Atlanta Fed GDPNow tool readjusted once again on Thursday to reflect the Fed’s recent actions and the latest economic reports. GDPNow is projecting Q2 gross domestic product (GDP) for the United States at 0.0%. The tool had originally projected 2.4% about two months ago and dropped to 1.3% about a month later. Last week, the number shrunk to0.9% and now, it’s at zero. If the actual GDP turns out to be negative, the U.S. will experience two straight quarters of negative GDP—which commonly defines a recession.

Notable Calendar Items

June 20: Market closed for Juneteenth holiday

June 21: Existing home sales

June 22: Earnings from KB Home (KBH) and H.B. Fuller (FUL)

June 23: Initial jobless claims, U.S. manufacturing PMI, and earnings from FedEx (FDX), Accenture (ACN), and Darden Restaurants (DRI)

June 24: Michigan Consumer Sentiment, New home sales, and earnings from CarMax (KMX)

TD Ameritrade® commentary for educational purposes only. Member SIPC.

Image sourced from Pixabay

This post contains sponsored advertising content. This content is for informational purposes only and not intended to be investing advice.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.