This post contains sponsored advertising content. This content is for informational purposes only and not intended to be investing advice.

(Monday Market Open) Equity index futures were down quite a bit overnight as European markets were selling off. However, comments from Russian Foreign Minister Sergei Lavrov suggested there was still a diplomatic way out of the current situation with the Russian troop build up near the Ukrainian border. The comments helped futures turn around and actually move to the positive. However, an interview with St. Louis Fed President James Bullard appeared to push futures slightly to the downside again.

On top of Russian tensions and Bullard comments, Goldman Sachs (NYSE: GS) lowered their price target on the S&P 500 (SPX) for 2022. The new target is 4900, but GS analysts did offer a range of 3600 to 5500. Last Friday, GS increased their forecasts for Fed rate hikes to seven for the year.

Bullard in a China Shop

In response to the hotter than expected Consumer Price Index (CPI) report last Thursday, St. Louis Federal Reserve President James Bullard commented that he would like to see the overnight rate raised to 1% by July. While the market reacted negatively to the CPI report, it really sold off after his comments. This morning, Mr. Bullard had another interview on CNBC where he defended his comments that the Fed needs to be more aggressive attacking inflation.

President Bullard acknowledged that he was only one member of the Fed committee, but he still plans to push for higher rates sooner. He cited that each CPI report from October 2021 to January 2022 has been worse than expected and expressed concern that the situation could create a negative feedback loop of inflation that the Fed may not be able to manage in the future. He felt that the Fed could manage the current situation without disrupting the markets too much, but he expressed concern that the Fed’s credibility is on the line if they don’t act. Equity index futures turned slightly negative after his comments.

Several other Fed members will be speaking this week, which will likely attract more attention as investors try to determine how the committee will swing in March. Additionally, the FOMC meeting minutes are scheduled for release this Thursday.

On Tuesday, the Producer Price Index (PPI) will provide additional insight to what companies are dealing with as far as inflation.

Outside of the focus on the Fed, semiconductor Nvidia (NASDAQ: NVDA) is expected to report earnings on Wednesday, and Walmart (NYSE: WMT) is expected on Thursday.

Friday’s Action

On Friday, stocks were unable to bounce back from Thursday’s sell-off. Stocks fell throughout the morning as rumors from the United Kingdom surfaced about increasing tensions with Russia. U.S. stocks started selling off going into the lunch hour. During the afternoon trading session, a White House press briefing with White House National Security Advisor Jake Sullivan revealed that United States and some of its allies were concerned about Russia possibly invading Ukraine in the near future. In fact, Mr. Sullivan warned all Americans to leave Ukraine as soon as possible.

According to Euronews, the United Kingdom and Norway joined the United States in urging their respective nationals to leave Ukraine immediately too. However, Ukraine appears to be downplaying the threat. Ukrainian Foreign Minister Dmytro Kuleba said that there was “nothing new” from the United Kingdom or the United States.

The tension between Russia and Ukraine has been ongoing. In 2021, Russia had been slowly accumulating troops in several locations about 250 kilometers or more outside the border. The troop movements have caused Ukrainian allies to try and push back against Russia.

The tensions are likely a contributing factor to rising oil prices. One of the big issues in the Asia and Eastern European region is the building of oil pipelines. So, it’s no surprise that crude oil prices jumped on the news. Crude futures jumped up to $95 per barrel. However, prices pulled back to close at $93.85 for a change of 4.42%. Nonetheless, oil still closed at a new seven-year high. This morning, oil prices had pulled back 0.87% in premarket trading.

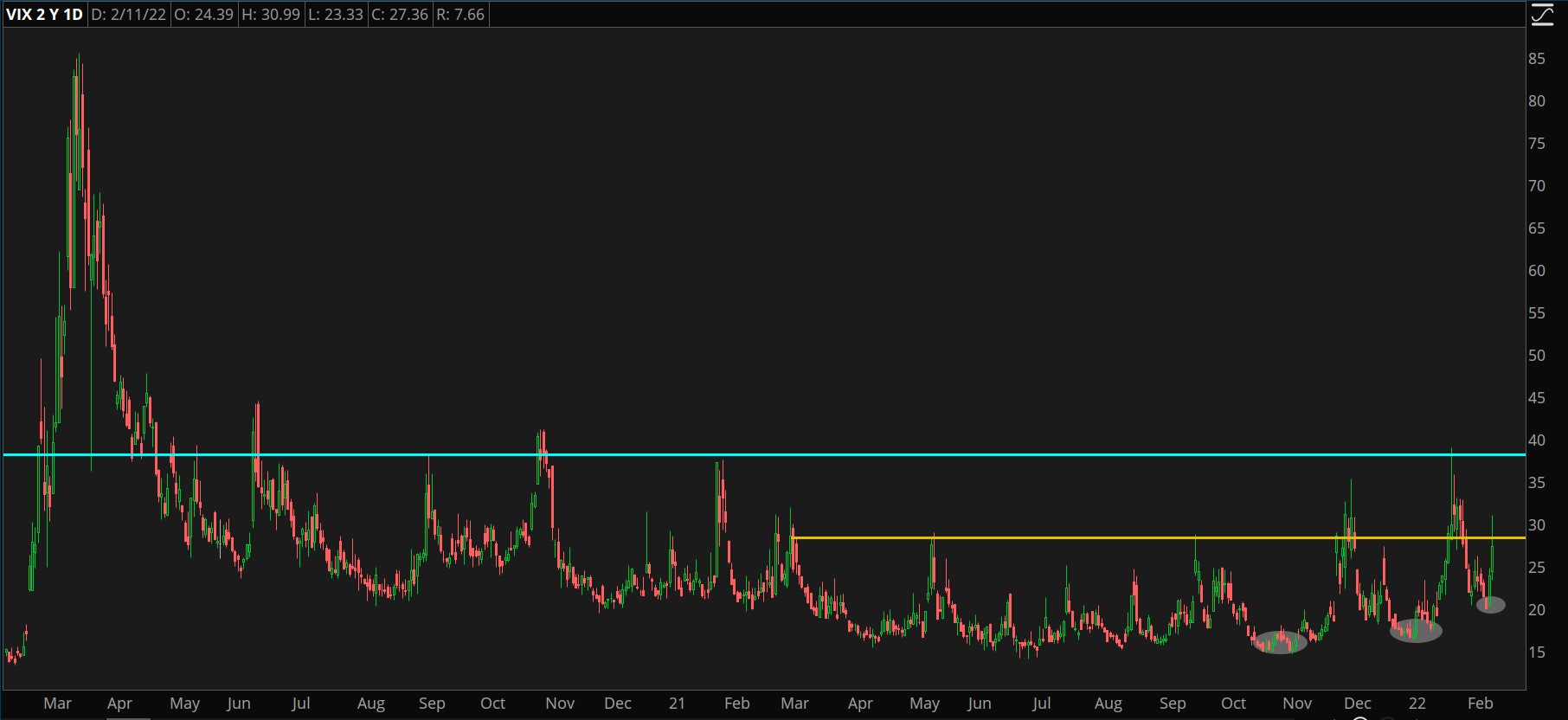

The S&P 500 (SPX) fell on the news but traded mostly sideways after the press briefing and actually closed off its lows for the day. The SPX closed 1.90% lower on the day. The Cboe Market Volatility Index (VIX) spiked up from about 25 to 31 during the day as investor fears increased. However, the VIX also pulled back, closing at 27.36. The Nasdaq Composite ($COMP) was hit the hardest, falling 2.78% on the day. The Russell 2000 (RUT) actually showed some strength in that it fell the least, dropping 1.02%.

Aerospace and defense company Lockheed Martin (NYSE: LMT) rose 2.79% and Northrup Grumman (NYSE: NOC) increased 4.53%, but the S&P Aerospace & Defense Select Index closed 0.03% lower on the day.

CHART OF THE DAY: CRESCENDO? The Cboe Market Volatility Index (VIX—candlesticks) appears to see increasing fear among investors because it has created higher lows in recent months. It has also broken its short-term reversal line in favor of a longer-term reversal line. Data Sources: ICE, S&P Dow Jones Indices. Chart source: The thinkorswim® platform. For illustrative purposes only. Past performance does not guarantee future results.

Second Look: After Thursday’s CPI report, the CME FedWatch Tool spiked up to a greater than 93% probability of a half-point hike by the Fed in March. However, the market has quickly pulled back from that projection, giving a 54% probability of a half-point rate hike. This tool can vary day to day and likely has no bearing on the Fed’s decision, but it’s helpful in understanding what the markets are telling investors.

As I said above, the Fed has another CPI report before it meets in March, which could signal the slowing that many economists have been projecting. So, it could be that these probabilities will continue to change up or down as more information is available.

The 10-year Treasury yield (TNX) was nearing 2.1% yesterday and even inched up a little closer this morning but has since pulled back below 2%, closing at 1.955% for the day. There had been some tension around the 10-year yield getting to 2%, so perhaps the bond market can settle down now that mark was met. Unfortunately, the tension around oil prices possibly reaching $100 may make it hard on bond traders, and the 2-year Treasury Yield was testing new highs on Friday.

This morning, the 10-year yield was trading around 1.99%, and the 2-year yield was trading at 1.58% which is higher than its Friday close.

TD Ameritrade® commentary for educational purposes only. Member SIPC.

Featured image sourced from Unplash

This post contains sponsored advertising content. This content is for informational purposes only and not intended to be investing advice.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.