Many people find self-employment and contract work very rewarding, but calculating the U.S. taxes you owe can get tricky. It’s critical to make sure you have everything you need so you can make the appropriate deductions, claims, etc. and still max out your tax refund.If you were self-employed or worked as a contractor over the past year, you will probably receive tax form 1099-MISC since you earned what the Internal Revenue Service (IRS) calls “non-employee compensation.”In general, your business clients need to issue Form 1099-MISC to you whenever they paid you $600 or more in any tax year. Also, if you are self-employed, you must report any self-employment income you earn if the total amount is $400 or more. Filing your taxes will also differ from what a regularly-employed taxpayer with income reported on a W-2 will experience.

Overview: Contract/1099 taxes

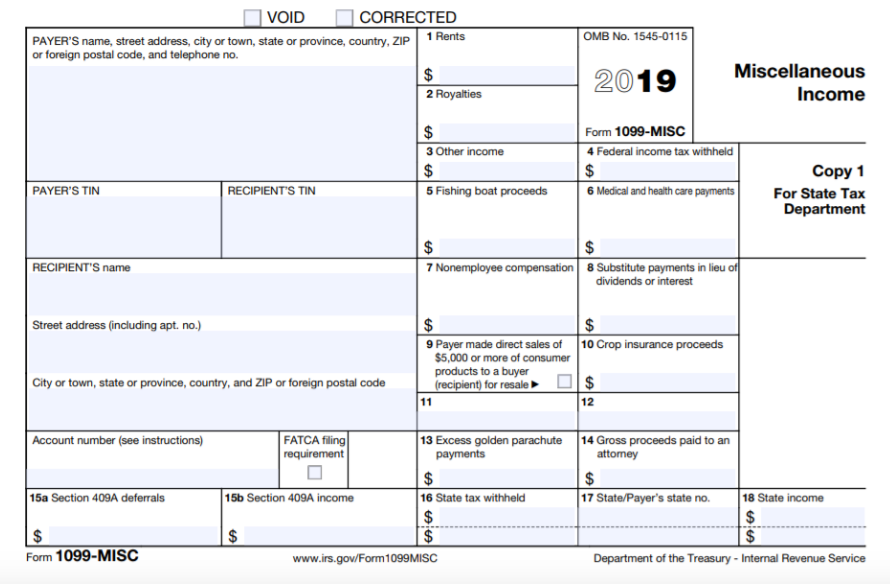

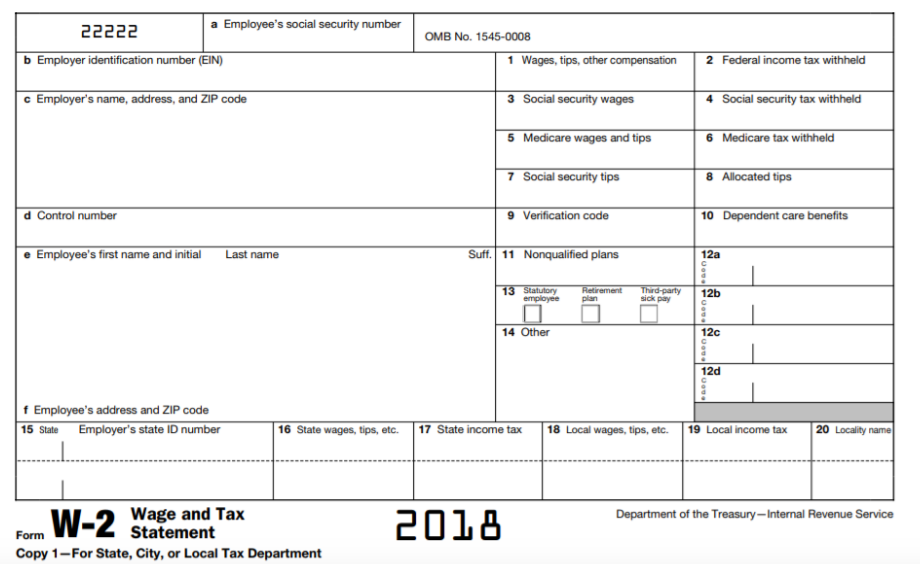

U.S. taxpayers and employers generally use the IRS’s Miscellaneous Income Form 1099-MISC to report information about payments they make to independent contractors. An image of the 1099-MISC form from the IRS appears below: You can compare that form with the IRS’s W-2 form instead of the 1099-MISC form:

You can compare that form with the IRS’s W-2 form instead of the 1099-MISC form: An employer might use IRS Form 1099-MISC instead of Form W-2 to:

An employer might use IRS Form 1099-MISC instead of Form W-2 to:

- Report any payments they might make as a result of their business or trade to someone who is not their employee or to a business that is not incorporated, or

- Report payments of over $10 in gross royalties or over $600 in rent or compensation payments.

Many independent contractors will 1099-MISC tax form, so if you’re an independent contractor, you need to understand how to calculate tax on your 1099 income.

Breakdown of Tax Liabilities For 1099 Taxes

Tax liabilities reported on IRS Form 1099 have a number of possible components relevant to independent contractors and others who receive income from sources other than regular employment. This includes Section 409A income and deferrals, as well as state tax withheld and state income. The following list breaks down the various payments that employers can report on Form 1099-MISC most relevant to independent contractors. It also provides examples of what sort of taxable income source gets reported in which box on that form, according to the IRS.

Box 1: Rents

This amount put in this box reports rent paid to you for the use of real estate.

Box 2: Royalties

Royalties paid to you arising from oil, gas or mineral properties; timber, coal and iron ore; and copyrights or patents are reported in this box.

Box 3: Other income

The number shown in this box may be payments received from a deceased employee, as well as prizes, taxable damage, awards, Indian gaming profits, or any other income subject to taxation.

Box 4: Federal income tax withheld

This box shows any backup withholding tax withheld by your employer. It can also show withholdings from gaming profits obtained at Indian casinos.

Box 5: Fishing boat proceeds

This box shows what you received from fishing in a boat where the operator considers you to be self-employed.

Box 6: Medical and health care payments

If you received payments for providing medical or health care as an individual, it will appear in this box.

Box 7: Nonemployee compensation

This box shows your nonemployee compensation and will typically be most relevant to an independent contractor. Independent contractors generally receive this form in place of Form W-2 because the filer did not think of them as an employee, so they did not withhold income tax, Social Security tax or Medicare tax from payments the contractor received for services provided.

Box 8: Substitute payments in lieu of dividends or interest

Shows the amount of substitute payments made in lieu of dividends or tax-exempt interest that was received by your broker for you from loaning out your securities.

Box 9: Payer made direct sales of $5,000 or more of consumer products to a buyer or recipient for resale

If this box was checked, it means that $5,000 or more was paid to you for sales of consumer products. These sales may have been made on a buy-sell or a deposit-commission basis, for example. The employer does not have to state a dollar amount of sales.

Box 10: Crop insurance proceeds

This box contains the total amount of crop insurance proceeds of $600 or more that were paid to you when operating as a farmer by one or more insurance companies.

Box 13: Excess golden parachute payments

If you receive golden parachute payments in excess of the base amount, it will be reported in this box. The base amount is the average annual compensation for services you included in your gross income over the past five tax years.

Box 14: Gross proceeds paid to an attorney

The filer will put the gross amount of $600 or more they paid to an attorney for legal services, irrespective of whether or not those services were performed on their behalf.

Where To File Your 1099 Taxes

A nice thing about getting a1099-MISC instead of a W-2 form as an independent contractor is that you can claim deductions on the Schedule C form you will need to file with the IRS. This form is used to compute net profits from self-employment activities. Furthermore, if your deductible business costs total $5,000 or less, you can file the considerably briefer Schedule C-EZ with the IRS instead.Note that such deductions generally need to come from business expenses the IRS considers ordinary and necessary for the self-employment activities you engaged in. In general, an expense is considered ordinary if self-employed individuals in a similar field typically incur it, while a necessary expense consists of one helpful to you for completing the work you were contracted for.

Final Thoughts

Whether you use Schedule C-EZ or C to file with the IRS, your net profit will be computed by subtracting your deductible business expenses from your total self-employment income that also includes earnings not reported on a Form 1099-MISC. That net profit figure will then be put on your Form 1040 and added to any other earnings you had to compute your taxable income.Finally, your 1099 income may not be the only tax liability you have as an independent contractor, since you may also need to pay employee income taxes,capital gains taxes,investment taxes and/orbrokerage taxes. It may therefore make sense for you to consult with a professional for any complicated tax situations to help minimize your tax payout and assure you report all earnings and deductions correctly.

About Jay and Julie Hawk

About Julie:

Julie Hawk earned her honors undergraduate degree from the University of Michigan before pursuing post-graduate scientific research at Cambridge University. She then started work in the private sector as a business systems analyst for a major investment bank, where she qualified as a Series 7 Registered Representative and received comprehensive training in various financial products. Further honing her skills, she attended the prestigious O’Connell and Piper options training course in Chicago, mastering professional option risk management techniques.

Julie then transitioned into the role of a professional Interbank forex trader, currency derivative risk manager and technical analyst, ascending to the position of vice president over a 12-year career in the financial markets. Julie’s illustrious banking career spanned working for major international banks in New York City, London, and San Francisco, where she served as an Interbank dealer, technical analyst, derivative specialist and risk manager. Her responsibilities included educating, devising customized foreign exchange hedging and risk-taking strategies, and overseeing large-scale transactions for esteemed banking clients, including corporations, fund managers and high-net-worth individuals. As part of her responsibilities, Julie managed substantial portfolios of forex options, spot, and futures positions as a currency options risk manager, earning recognition for executing innovative and highly profitable forex derivative transactions. Julie also spearheaded educational conferences on currency derivatives.

During her banking career, Julie attained world-class expertise in technical analysis, including Elliott Wave Theory, and pioneered research into automated trading and trading signal systems. An active member of the San Francisco Writers’ Guild, Julie also authored trade strategies, educational material, market commentary, newsletters, reports, articles, and press releases. She became a sought-after market expert who was frequently interviewed by financial magazines and news wires such as REUTERS.

Following her retirement from the banking sector, she dedicated 15 years to online forex trading, mentoring and freelance writing for TheFXperts, which she co-founded with her husband Jay. Julie is the co-author of “Forex Trading: A Beginner’s Guide” and “Technical Analysis for Financial Markets Traders,” in addition to five other books on financial markets trading and personal finance. She now focuses on writing articles on financial markets for platforms like Benzinga, although she continues to trade forex online and mentor fellow traders as part of TheFXperts’ financial team.

About Jay:

Jay Hawk grew up in Chicago and Mexico City where he became bilingual in English and Spanish. After taking formal training as a classical guitarist at prestigious music conservatories in Europe, Jay then embarked on a remarkable journey into the financial markets, cultivating his notable expertise through hands-on experience that began on the Midwest Stock Exchange.

His financial career progressed as he started actively participating in various exchange floor trading activities in the Chicago futures and options pits, where he worked his way up the ladder, serving as a clerk, trader, broker, investor and fund manager. Jay then ran a retail stock brokerage desk and managed funds for large institutional investors, leveraging his discretionary trading skills to yield profitable results for clients.

This ultimately led to Jay holding exchange seats and operating as a market maker on options exchanges in Chicago and San Francisco, initially on the Chicago Board Options Exchange. Jay also played a significant role in the Chicago Mercantile Exchange’s evolution, where he contributed to launching and actively trading the first listed currency futures options. After transitioning to the West Coast, Jay then held a seat and ventured into trading stock options and their underlying stocks on the Pacific Options Exchange.

Jay’s comprehensive understanding of fundamental economic and corporate analysis continues to inform his trading and investment activities and has led to his subsequent success as an expert financial writer. Together with his wife Julie, he co-authored “Stock Trading: A Beginner’s Guide”, “Commodity Trading: A Beginner’s Guide” and “Fundamental Analysis for Financial Markets Traders,” among their published books focusing on financial markets trading, market analysis, and personal finance.

As an integral member of TheFXperts’ team, Jay now excels in trading forex online for his personal account, mentoring aspiring traders and writing for financial platforms like Benzinga where he specializes in covering topics related to the stock and commodity markets, as well as investing, trading and reviewing online brokers.