Betterment is a smart robo-money manager that helps you save, invest and even spend your money. It has more than 500,000 registered customers and manages over $21 billion in assets. As a fiduciary, Betterment is committed to act in your best interest at all times. The investing platform lets you manage your money, guide your investments and plan your retirement at your convenience.

- Can open an account with a $0 minimum balance

- Offers goal-based investing

- Charges low annual management fees

- Offers a wide range of stocks and ETFs

- Provides access to advanced investing tools

- Provides personalized financial advice plans

- Charges a high fee for personalized financial advice comparatively

- Not suitable for day traders and short-term investors

- Does not offer any real estate stocks, commodities and foreign exchange

Invest

By investing on the Betterment platform, you could earn up to 38% more returns over 30 years than your average investor. The investment platform and its portfolios have been featured in global publications such as The New York Times, CNBC, Business Insider and Forbes.

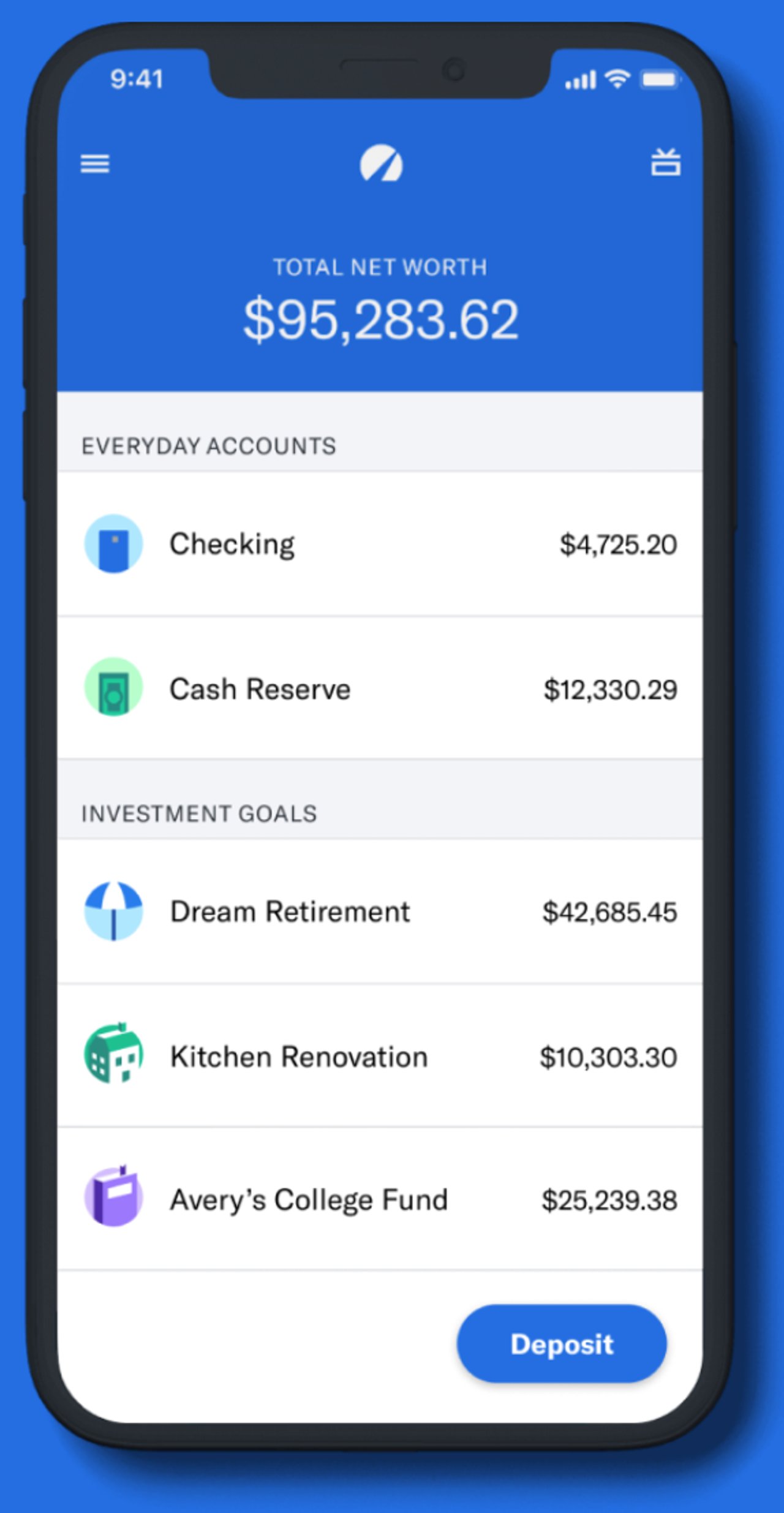

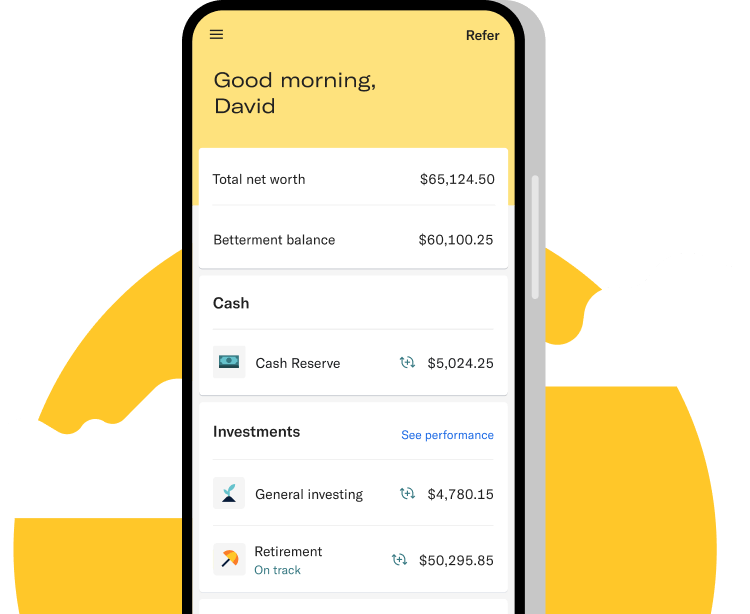

High Yield Cash Reserves

With a Betterment account, you can earn a 4.75% annual percentage yield (APY) on your investments. The APY is the interest you would have earned if the interest rate remained unchanged for an entire year.

Spend

Betterment Checking is an account that offers a Visa debit card for your daily spending. ATM fees and foreign fees are automatically reimbursed. The Visa debit card does not charge you an overdraft fee.

You can change your PIN or lock your card using the mobile app. The Betterment Visa debit card can also be used to tap-and-pay while you are on the move. It also features a cashback rewards program on thousands of favorite brands such as Adidas and Walmart.

Why Betterment Over Others?

Betterment is a financial advisor built for people who are new to investing. The investing platform gives you access to personalized advice and low fees to manage your portfolio.

Unlike other investment brokers, you can sign up for an account on Betterment without a minimum balance. Betterment lets you automate your deposits on a regular basis. It also supports Roth, traditional and SEP IRAs for your retirement planning.

Advantages of Betterment

- Allows next-day deposits

- Own fractional shares

- Has asset allocation and tax coordination

- Has automated tax-loss harvesting

- Allows 60-second rollover on investments

Betterment provides affordable pricing plans to match the requirements of people who are new to investing. You can open an account with a $0 minimum balance.

Basic Plan

New investors can open a basic account on Betterment. A basic account does not charge you an annual fee on your investments. Signing up for a basic account will provide you with a Betterment Checking account and a Betterment Visa debit card. Your basic account is insured up to $2 million for singles and $4 million for joint accounts by the FDIC.

There are advanced tools that you can leverage on the platform for financial advice and retirement planning. Upon request, you can receive feedback on the accounts you hold at other financial institutions. It also gives you access to a cash reserve to pool your money for individual goals.

Digital Plan

Intermediate investors can open a digital account on Betterment. A digital account will charge you an annual fee of 0.25% on your investments or $2.50 on every $1,000 you invest. You get access to low-cost portfolios built and managed based on your priorities. It also provides a wide range of socially responsible investing options.

You can choose between opening an individual account, joint account, IRA account or an account for trusts. The digital plan on Betterment features automation on your portfolio rebalancing and dividend reinvestment. It also provides a checking account and a cash reserve.

Premium Plan

Professional investors can open a premium account on Betterment. A premium plan will charge you an annual fee of 0.40% or $4 for every $1,000 you invest. Besides all the features of a digital plan, you also get access to unlimited calls and emails with Betterment’s in-house team of certified financial planners. You can choose to upgrade to a premium plan when your account has the qualifying balance.

When you sign up, you will be requested to complete a questionnaire about your financial needs. Based on your answers and preferences, Betterment will suggest suitable investment options to accomplish your financial goals. The investment platform has an asset allocation tool to instantly set the ratio for diversifying your portfolio between stocks and ETFs.

The Checking account is a quick and easy way to deposit money. You can transfer funds from your bank account to your Betterment Checking account through electronic transfers. Betterment also allows you to transfer assets from other brokerage accounts using the Automated Customer Account Transfer Service.

For investors planning their retirement, transfers can be completed through IRA rollovers. Transferred funds can be automated to invest within 1-2 business days. However, you can not transfer funds to your Betterment account by check, credit or debit card. Wire transfers may involve a fee on each transaction.

Betterment is filled with rich educational resources that can help you learn how to invest. It has a Frequently Asked Questions section that covers numerous topics such as how investing works, saving money, retirement plans and expert opinions.

The customer support team at Betterment can be contacted by email or phone. The team is available from Monday to Friday. Betterment also has a live chat feature to answer your queries instantly.

Your Betterment account can be verified with 2-factor authentication. If you don’t receive your authentication codes on your registered mobile number, you can immediately contact the customer support team for assistance.

The investing platform also offers The Betterment Satisfaction Guarantee to its investors. According to its policy, investors who are not satisfied with Betterment’s financial advisory experience can have their management fees waived for up to 90 days.

Once you’ve completed the questionnaire, you can pick an investment portfolio that matches your risk tolerance and financial goals.

| Portfolio | About |

|---|---|

| Standard Portfolio | The Standard portfolio offers investment options from a mix of asset classes. These investments provide global exposure to your portfolio and consist of international stocks and ETFs. |

| Flexible Portfolio | The Flexible portfolio offers investment options from different asset classes. It also allows you to customize your asset allocation to improve your returns. |

| Socially Responsible Investing Portfolio | The Socially Responsible Investing portfolio offers investment options that meet certain environmental guidelines. This portfolio contains sustainable and eco-friendly companies. |

| Goldman Sachs Smart Beta Portfolio | The Goldman Sachs Smart Beta portfolio offers investment options that increase your returns while reducing risks. It is available only to investors with more than $100,000 in their Betterment account. |

| Blackrock Target Income Portfolio | The Blackrock Target Income portfolio offers investment options from various Blackrock ETFs. This portfolio is focused on increasing your returns and consists exclusively of ETFs. |

| Tax-Coordinated Portfolio | The Tax-Coordinated portfolio offers investment options with large tax liabilities, such as an IRA account. Investments with lower tax liabilities can be managed from separate taxable accounts. |

You can download the Betterment app for free on your iOS or Android device. The mobile app has all the tools and capabilities of the web version. You can track your portfolio performance and manage your account from anywhere, anytime.

Betterment offers low-cost stocks and ETFs that have attracted young investors. Its pricing plans and the broad spectrum of portfolio options are suitable for new and seasoned investors. The goal-based investing strategy has helped thousands of people fulfill their financial dreams.

The automated deposit on the platform saves time and effort for investors. Betterment also provides a combination of innovative fintech and personalized financial advice to improve your portfolio.

Frequently Asked Questions

Is Betterment good for beginners?

Betterment is great platform for beginner investors. However, its many features can also make Betterment very useful to advanced investors.

How trustworthy is Betterment?

Betterment is considered to be a trustworthy platform for investing. They are a registered investment advisor and have been in operation since 2010. They prioritize transparency and provide clear information about their fees, investment strategies, and security measures. Additionally, Betterment is regulated by the Securities and Exchange Commission (SEC) and the Financial Industry Regulatory Authority (FINRA), which adds an extra layer of oversight and accountability.

Should I use Vanguard or Betterment?

Vanguard is known for its low-cost index funds and long-standing reputation in the investment industry. It offers a wide range of investment options and is suitable for individuals who prefer a hands-on approach to managing their investments.

On the other hand, Betterment is a robo-advisor that uses algorithms to automate investment decisions. It offers a more simplified and user-friendly experience, making it a good option for individuals who prefer a more hands-off approach and want a more automated investment management service.

Consider factors such as your investment knowledge, desired level of involvement, fees, and specific investment goals when deciding between Vanguard and Betterment.