The speed with which volatility is realized, across markets, has risen.

This is due in part to changing market structure; via a reduction in rates and market stabilization programs, participants have been induced to take on more interest rate and equity market risk.

In the face of prevailing regulations and frameworks, heightened stress may result in hedging and de-leveraging cascades that affect the stability of all markets.

With day-to-day variances higher and increased positive cross-asset correlations, especially in stressful market environments, classic hedging methods — the 60/40 portfolio, for instance — are naive.

“We’re living through a time where there has not been as many cross-asset correlation breaks as this time, and the only true hedge is volatility,” The Ambrus Group co-chief investment officer Kris Sidial once explained to Benzinga. “It is shocking for me to see how many people, who control money, are dislocated with the day-to-day market moves and potential hazards at bay.”

To learn how investors may use packaged options and volatility targeting strategies to reduce portfolio volatility, Benzinga spoke with Karan Sood, CEO and Managing Director, Head of Product Development at Cboe Vest Financial LLC.

The Protective Collar: After 2008, the illiquidity, credit risk, and cost of structured notes pushed investors into the S&P 500 complex.

In light of this movement, Cboe Vest launched its flagship fund to help investors mitigate losses and amplify long-term returns.

The Buffer Protection Strategy — a put-spread collar applied to static long S&P 500 exposure — is an investable asset that provides investors downside protection.

With such a product, investors who are more sensitive to risk can forgo some upside to protect the downside.

Graphic: Illustration of hypothetical returns for Cboe Vest’s Buffer Strategy.

“It’s been a phenomenal strategy, and you’re seeing other market participants enter the space,” Sood said on Cboe Vest’s iterations of the Buffer Protection Strategy garnering up to $6 billion in assets over half a decade.

In the face of a relentless long-term uptrend, Sood sees interest in his firm’s products as a result of skittishness with respect to heightened valuations and a breakdown in cross-asset correlations, rendering traditional hedges, like bonds, less attractive.

“Whenever we think of classical risk management, we think of the balanced portfolio; you want to be in equities and bonds,” Sood said. “You want to be enough in bonds so that you can stomach the downside risk on equities.”

Over the past 40 years, monetary policy was used as a crutch to support the economy. This promoted deflation, innovation, and the subsequent rise in valuations.

“Bonds have been giving you really good returns because interest rates have been going down since the 1970s when they peaked at about 11%,” Sood added.

“That’s changing now; we’re at the zero bound, and it’s unlikely that will be as a strong of a tailwind. Worse, it could be a headwind if interest rates start to rise.”

With fears that rising rates will take away from the protective benefits bonds offer to portfolios, Sood offers an alternative with no duration or rate risk: “Just like you use insurance for other elements of your life, you can use options to risk manage.”

Graphic: Cboe Vest compares the risks associated with participating in the market.

Victims Of Success: Similar strategies, including those offered by Cboe Vest, have garnered around $20 billion in assets.

These strategies, in providing investors constant hedged equity exposure, must trade in and out of certain options maturities, in massive size, which may impact underlying market movement.

Benzinga asked Sood whether such strategies could become victims of their own success and how his firm is protecting investors.

“The first version of these kinds of strategies have a lot of options that are rolling” from one expiration to another in one go. “The new versions of these strategies tend to not roll in one go,” he added.

Cboe Vest, in anticipation of strategy growth and market impact, from the start, diffused interest across multiple strategies.

“We would offer a product that rolls in JAN, we would offer a product that rolls in FEB, one in MAR, and so on,” Sood said. “We offer 10% protection products, 20% protection products,” too.

As no single strategy is rolling in one day, it’s tougher to front-run and take value from unsuspecting customers.

“The best way to deal with it is to offer multiple strategies and distribute the asset base, in those multiple strategies, so that no single one is getting into a technical situation where there’s some kind of a delta risk on the day the strategy rolls,” he noted.

Applying The Thesis Elsewhere: “What we do is we take risky assets, and we give an investible option to clients,” Sood said. “We’ve done that for equity, international developed markets, international emerging markets, and commodities like gold.”

With the recent interest in listed cryptocurrency products that subject investors to burdensome roll costs and fees, Cboe Vest introduced the first mutual fund providing access to bitcoin futures, with a built-in strategy to manage volatility.

“The S&P may give you, worst-case, 30% vol,” Sood explained. “Bitcoin’s long-term average is something like 95% vol. That will hijack the portfolio’s volatility.”

In smoothing the volatility of bitcoin investments, Cboe Vest employs a futures volatility targeting strategy.

Graphic: Per Cboe Vest, “Bitcoin has been significantly more volatile, sometimes as high as 5 times more volatile relative to the U.S. stock market. Its volatility has exposed investors to sizeable losses in the past.”

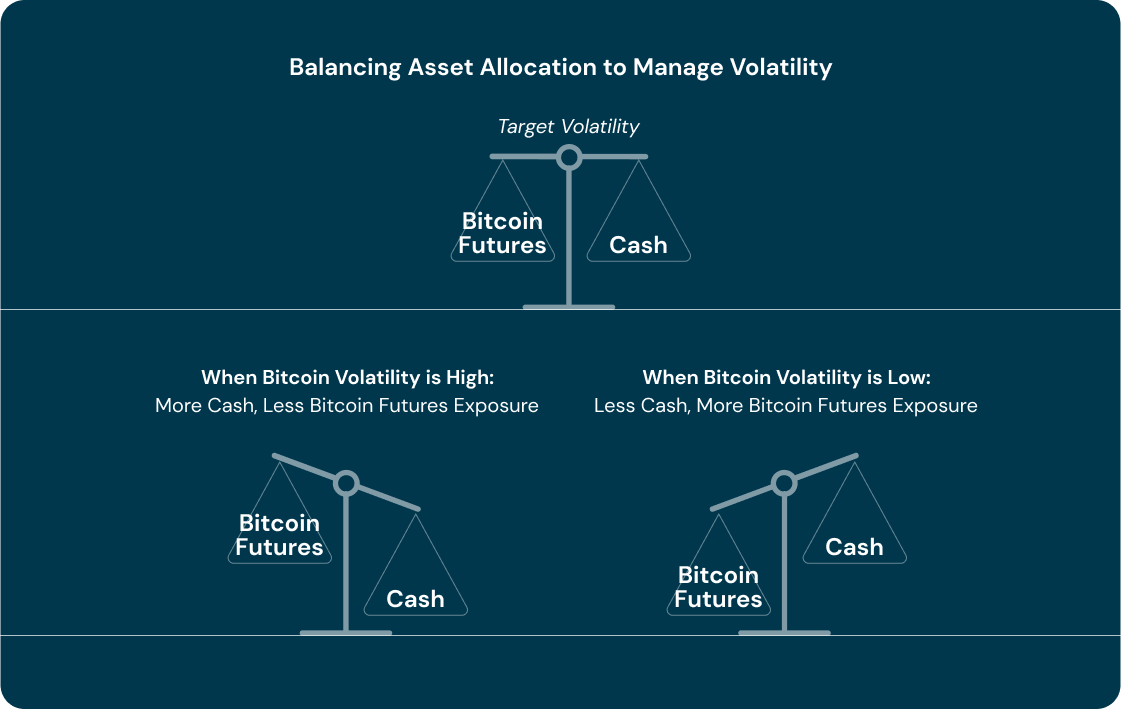

“When bitcoin’s volatility goes up, we decrease exposure to bitcoin. When bitcoin volatility goes down, we increase exposure, all the while targeting a set level of volatility around 45%,” Sood said.

Putting it simply, when bitcoin performs well, its realized volatility is low. That’s when allocations to the asset are highest.

Conversely, when bitcoin begins to decline and volatility picks up, allocations are dropped.

“Over a full market cycle, you end up with fewer returns than bitcoin, but with substantially lower levels of volatility,” he noted in explaining how this product allows investors to increase their allocation in the asset class. “Now you can move the needle from a return perspective.”

Graphic: Visualizing Cboe Vest’s management of bitcoin-linked returns.

Vision For The Future: As the regulatory environment around cryptocurrency evolves, there may be a time when Cboe Vest provides participants exposure directly to spot bitcoin.

“Right now, you can’t be assured that you’re getting a good price, that there’s no front-running happening, and there is good competitive price discovery,” Sood said.

Moreover, a focus going forward for the firm is the application of its risk management strategies on a broader set of asset classes. “We want to offer solutions for the entire portfolio,” he said, in looking to clients for input on what products they want to be offered.

“I think there’s too much faith being placed in bonds for protection, and that worries me," Sood added. "As investors could have a double whammy of being in risk assets like equities and their risk management bucket not working out for them because they’re too much invested in bonds.”

To learn more about Cboe Vest’s portfolio enhancing strategies, visit cboevest.com.

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.