This post contains sponsored advertising content. This content is for informational purposes only and not intended to be investing advice.

Farmers across the Northern Hemisphere are gearing up for the spring planting season caught in the crosshairs of the La Niña weather phenomenon, higher farming costs from the surge in oil and fertilizer prices adding to already elevated inflation, and the unfolding crisis in Ukraine. In addition, borrowing costs are likely about go up in the United States for the first time since the 2015-2018 cycle, with the Federal Reserve (Fed) expected to begin raising short-term interest rates in mid-March.

The turmoil over Ukraine has already lifted prices for primary commodities such as corn, soybeans, and wheat to multi-year highs (Figure 1), which could in turn up the heat on rising consumer prices for meats and other foodstuff and put pressure on margins for food companies. Corn and soybeans are the primary feedstock for livestock and poultry. Wheat is a critical ingredient in diets all over the world, from breads, scones, cakes, pizza, noodles, and so much more. With food prices soaring, the economic implications are most severe for emerging market countries where spending on food makes up a higher percentage of total income, but the economic ramifications will also be felt in developed countries.

Figure 1: Soybeans, Corn, and Wheat

Ukraine-Russia Wheat and Corn

Let’s start with an examination of the spring planting season in the region with the highest level of uncertainty.

Farmers in southern and eastern-southern Ukraine are typically the first to kick off the spring planting of corn in mid-April and sowing in the primary growing central-west and northeast regions begins in May, according to data from Foreign Agricultural Service of the U.S. Department of Agriculture (Figure 2). In Russia, sowing of corn traditionally begins in the north, south and central districts in mid-April.

Figure 2: Ukraine planting regions.

Ukraine plays a significant role in the global commodities trade, being the world’s fourth largest corn exporter, accounting for about 13% of the world’s commerce in feed grain. It is also a major supplier of corn to the European Union. Any possible disruption to corn production in Ukraine could therefore have significant regional and global implications. Russia is a relatively low-level exporter of corn, shipping about four million metric tons to overseas markets. [The corn export market is dominated by the United States, which accounts for nearly 40% of the global trade, followed by Argentina and Brazil, respectively, with a combined 33%.]

In contrast to corn, wheat is the commodity most impacted by the Ukraine conflict. Russia is the world’s top wheat exporter, accounting for 19% of the global trade, while Ukraine accounts for 8% of the world’s wheat exports. So, it is not surprising that wheat has seen the largest price rises and sharpest increase in volatility. Among the primary importers of wheat are North African countries such as Egypt; Middle Eastern countries such as Iraq, Iran and Saudi Arabia; China and Southeast Asian nations such as Indonesia, Thailand and Vietnam.

Due to the fighting in Ukraine, the location of substantial Russian troops around the breadbasket regions of the country, and the closing of the Black Sea ports, the government of Ukraine has indicated that the spring planting season will be severely disrupted.

Weather & La Niña

The weather could also pose challenges to grain and oilseed production. La Niña, or the little girl, returned in 2022, coinciding with record heat in parts of South America, particularly in major corn and soybean producing countries such as Argentina, Brazil and Paraguay.

There is also a drought in parts of the Middle East which is expected to impact the production of wheat in Iran, Iraq and Syria, thereby increasing their dependence on imports. The agriculture minister of China, the world’s largest consumer of wheat, has said unusually heavy rainfall had significantly delayed the planting of the country’s winter wheat crop, which could add to the supply woes.

The damage to crop yields from the dry weather in South America is expected to reduce the amount of soybean to be exported from Brazil, Argentina and Paraguay – these three countries account for more than half of the world’s soybean exports, according to U.S. Department of Agriculture data. This could provide an opportunity for U.S. exporters to fill the gap in South American production (Figure 3).

Figure 3: Soybean Production

For the United States, La Niña is generally associated with cooler, wetter winters in the Northern U.S. and Canada along with dryer and warmer conditions in the southern U.S. Since 1959, when the National Oceanic and Atmospheric Administration began measuring El Niño and La Niña with their Oceanic Niño Index (ONI), there have been nine previous major episodes of La Niña. We define a major episode as one in which the ONI falls below -1°C (or rises above 1°C in the case of an El Niño).

Of the nine previous La Niña, seven have generally been associated with falling prices for corn, soybean and wheat. The last two La Niña’s have been different. Spot prices for corn and the soy complex rose in the 12 months following the beginning of the August 2010 La Niña. Wheat prices fell slightly. In the 12 months after the October 2020 La Niña began, prices rose for corn, wheat, soybeans and notably for soybean oil. Only soybean meal prices declined, and that has since reversed given the severity of the current drought in Argentina and Brazil.

These two most recent episodes of La Niña came at a time when commodity prices were generally rising amid quantitative easing by the Fed and other major central banks. Oil prices rallied in the summer of 2010 and early 2011 as the Arab Spring uprising caused concerns about supply. Oil and agricultural markets show a high degree of co-movement in prices, in part, because corn, wheat and soybeans are used to produce biofuels, and also because energy is among the input costs for agricultural goods.

U.S. Spring Planting

Data shows that a large swath of the U.S. Midwest and Central Plains tends to become dry-to-very-dry during La Niñas in March to April, with the Midwest – where the bulk of the U.S. corn and soybean crops are grown – returning to normal weather conditions in April-May, while the Southwest continues to show dry-to-very-dry conditions (Figure 4).

Figure 4: Precipitation during La Niña

U.S. farmers typically kick off their sowing of corn in April and soybean in May, and as they get closer to making their planting decision, prices will play a significant role in how much of their land will be cultivated with both crops. The USDA will issue its Prospective Plantings report at the end of March based on interviews with about 80,000 farmers. This report is likely to kick-off a vigorous debate about how many acres of soybeans and corn will be planted by U.S. farmers. Farmers intentions can change rather dramatically as the planting season gets closer, and as all of the various factors on the supply side of the ledger, from higher energy and fertilizer costs, to the critical demand-side factors emanating from the Ukraine conflict and drought in South America. Nevertheless, with the rally in prices for corn and soybeans, there will be a big push by U.S. farmers to plant more acres of corn and soybeans, the question is just how much more.

For farmers looking to hedge their corn and soybean crops that will be harvested in late summer/early fall, they might not be able to lock in the current high prices as the markets are in backwardation – where current prices are higher than prices further out (Figure 5). The shape of the maturity price curve is usually an indication that the current phase of high prices is dealing with a highly disruptive event which is not viewed to be permanent, but it could get worse (or better) at any time.

Figure 5: Backwardation

For instance, the March CBOT March corn contract was trading at $7.65 per bushel, while the

September contract was trading at $6.66, and the December contract at $6.38 as of this writing. Even though the contracts for delivery in September and December are lower than the corn contract for March delivery, they are relatively elevated compared to last year.

Similarly, the March CBOT soybean contract was trading at $16.93 per bushel, while the November contract is trading at $14.46. Kansas City May wheat was trading at $12.40 per bushel, compared to the December contract that was priced at $10.98.

Chicago wheat has the highest degree of backwardation. As of March 7, 2022, the nearby contract was 43% above the one-year-out contract.

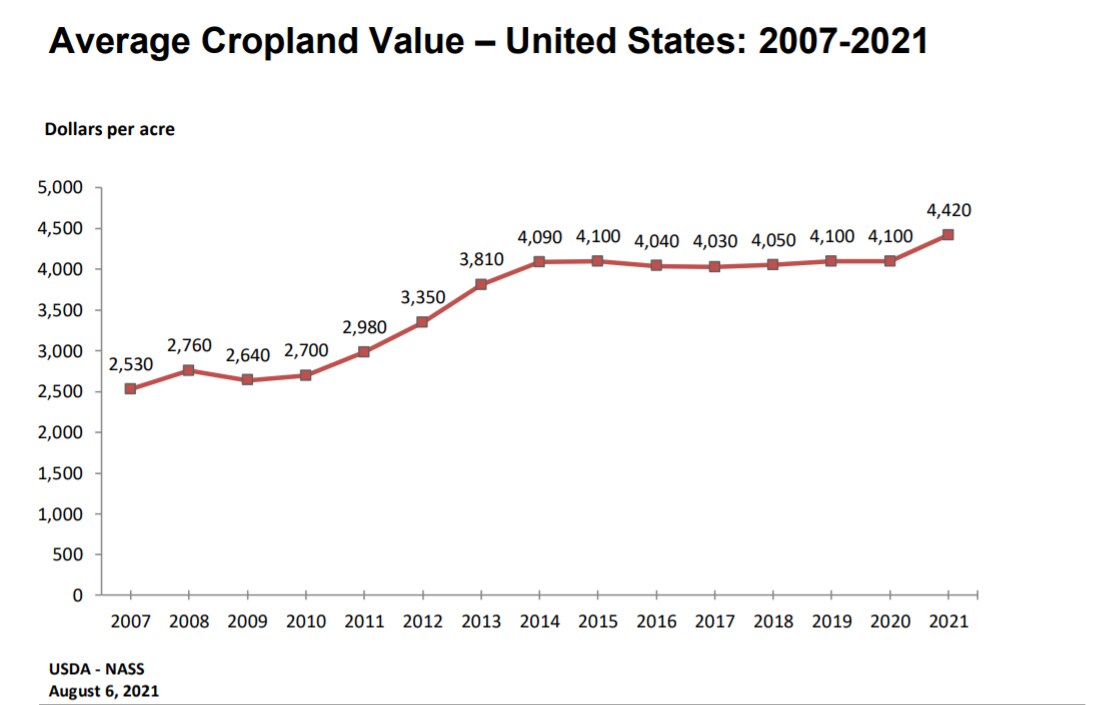

Aside from backwardation, which influences the ability to hedge, there are also rising costs for inputs into the production process. U.S. farming costs rose about 2.3% to $366 billion in 2020 from 2019, with total fuel costs amounting to $11.1 billion, according to USDA data. Diesel costs accounted for $7.1 billion. Crude oil prices averaged about $41 in 2020. On March 8, 2022, WTI crude oil was trading at $128 per barrel. The surge in oil prices could obviously add to farming costs, but the relatively high prices for grains and oilseeds could help to offset some of the costs (Figure 6).

Figure 6: Cropland Values

Farmers were already concerned over rising production cost amid the supply chain constraints related to the pandemic. The concerns might just escalate. The Purdue/CME Group Ag Economy Barometer’s February survey – conducted before the crisis in Ukraine – showed the producers remain concerned over the spike in production costs, leading them to expect weaker farm incomes in 2022. Supply chain issues continued to hamper farmers’ plans for investments in farm machinery, building and grain storage bins. Thirty percent of corn/soybean farmers said they had some difficulty in purchasing field inputs for the 2022 crop, with herbicides topping the list, followed by fertilizer and farm equipment parts.

Bottom Line

A lot is at stake this spring from the agricultural perspective that could have implications for global food production. As the common adage in farming goes, high prices are the cure for high prices. So, elevated prices for grains and oilseeds could motivate farmers in the U.S. and elsewhere to dedicate record amounts of their land to the production of grains and oilseeds that could help to make up from deficits from countries that are mired by conflict or inclement weather. But with production costs heating up as oil prices surge, there could be a further shrinking of consumer wallets. Inflation in the U.S. is already at the highest level in 40 years, rising to 7.5% in January and might head higher before peaking. All of these concerns make the U.S. spring planting season much more uncertain than usual.

This post contains sponsored advertising content. This content is for informational purposes only and not intended to be investing advice.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.