Central to my market and macro outlook at present is the likelihood we are amid a growth cycle downturn that is looking to decelerate meaningfully in the coming months. Whilst a potential recession was not part of this thesis, given the recent movements in the yield curve, geopolitical landscape, inflation pressures and deteriorating forward outlook for growth, the probabilities of such an outcome seem to be increasing by the day.

So, whilst having a macro framework and data driven outlook in mind, how to trade and profit from this scenario is key. It is all well and good analysing markets, companies and the macro environment, but, profiting from this analysis is what we as investors strive to do. In a slowing growth environment, buying long-term treasuries has been the go-to macro trade over the past 40 years. Right now, this classic late cycle long-bond trade is more hated and contrarian than it has been in a generation.

This is perhaps rightfully so with inflation is at its highest level since the 1980s. Unsurprisingly, long-term treasuries have as a result suffered their worst peak-to-trough drawdown in over 20 years.

Source: Bloomberg

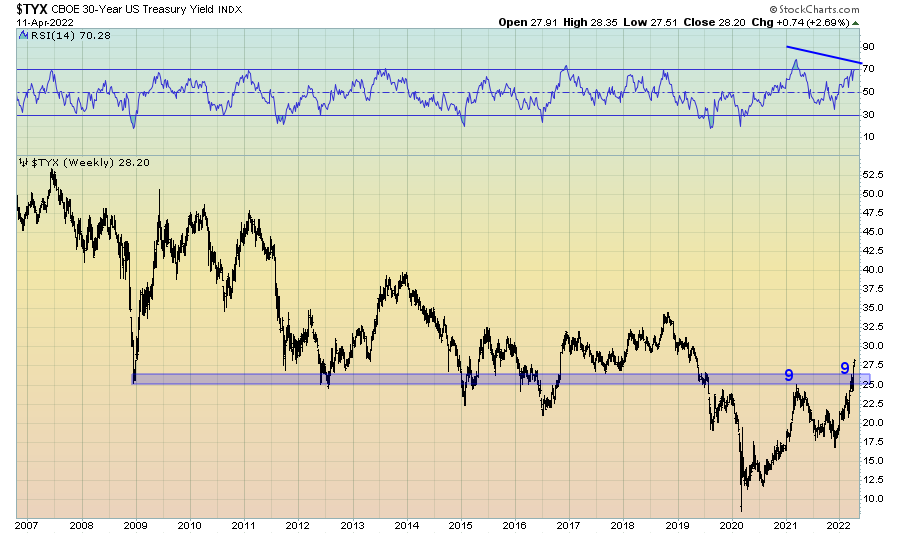

This bond sell-off has seen 30-year yields once again test the upper range of their 40-year downtrend, a trend that has been colloquially termed ‘The Chart of Truth’.

Is the great bond bull market finally over and the Chart of Truth no more?

We are indeed seeing endless calls for this to be the case, with any suggestions to the contrary being met with ridicule and contempt. However, some of the great contrarian trades eventuate when there is clear consensus. Right now, the consensus is very much of the opinion that yields are only going higher.

Such one-sided consensus can be headlined by one of the classic contrarian sentiment indicators in recent times in the cover of The Economist.

Likewise, calls for higher rates by the likes of JPMorgan’s Jamie Dimon seemingly have an uncanny ability to occur at their peak.

Clearly, bonds are hated right now and people want to believe yields will only go higher from here.

Looking at bond market sentiment through the lens of SentimentTrader’s Optix index, we are witnessing a level of pessimism towards bonds seen only a handful of times over the past two decades, all of which formed the base of strong rallies in the long bond.

On a shorter-term basis too, bond sentiment (per the 10-day Daily Sentiment Index) is nearing levels indicative of a reversal in recent years.

Source: The Felder Report

Whilst being a contrarian can be profitable at times, it is important to not simply be a contrarian for the sake of being contrarian. But, when everybody in the world hates bonds and we are heading into a growth slowdown, the risk-reward setup for bonds begins to look attractive. To profit as a contrarian is to have variant perception. So, what could lead yields lower?

Well, with all this talk of a shift to structural inflation, it is important to remember when yields rise this far this fast, things tend to break.

Source: Jesse Felder - The Felder Report

The market can only sustain such a swift rise in yields for so long. Throw in a slowing economy and the potential peaking of inflation, and we the makings of a fundamental case for an allocation to bonds.

Growth, Inflation & Bonds

In short, we are seeing a clear indication of a slowing economy and mounting headwinds for inflation.

There is now plenty of evidence to suggest we are entering the late stages of the economic cycle. Whether or not a recession will eventuate is not yet clear, but a material slowdown in growth is certainly what the leading indicators of the growth cycle are pointing to. We have a tight labour market, inverted yield curve, low unemployment, peak earnings, spiking oil prices, waning demand and plunging consumer confidence among many other late cycle indicators flashing risk-off.

Couple this with a monetary policy stance that is now a headwind for growth worldwide, and we have a clear deceleration in growth ahead of us.

Source: Top Down Charts

And financial conditions are now tight, a situation that does not bode well for growth.

Source: Andreas Steno Larsen

Indeed, inflation acts a tightening of financial conditions in its own right as it destroys demand and eats into real incomes.

Source: Raoul Pal

You simply cannot raise prices on consumers at a faster pace than their income growth without a significant destruction in demand. This is why inflation will in itself sow the seeds of its own demise.

Source: Gianluca

Again, as I have detailed in the past, though many inflation tailwinds are likely to persist for the years ahead, on a rate-of-change basis there is much evidence to suggest that inflation will deceleration throughout the second half of 2022 as the deceleration in growth becomes too much to bear. This dynamic should at some point provide a tailwind for bonds.

Even the Fed’s response of quantitative tightening to the current inflation pressures via the contraction of their balance sheet has ultimately resulted in yields falling over time. This is an important dynamic overlooked by many. The Fed implementing QT has historically resulted in yields falling over time as the economy cannot withstand higher yields in the face of slowing growth and tightening monetary policy.

Even during the inflationary 1970s, the period so prevalent in investors minds at present, bonds outperformed equities and did a better job of offsetting inflation than equities as the Fed tightened, a dynamic recently noted by Verdad Capital.

“In hiking environments, the risk-reward for owning equities becomes worse, and investors should look to diversify away from an all-equity book to preserve their capital for a better time. As bad a hiking cycles were in the 1970s, preserving capital for easing cycles would have been a terrific strategy.”

Again, this ties into the idea that Fed tightening is a late cycle dynamic brought on by their dual mandate of stable prices and low unemployment, two of the most lagging business cycle indicators that exist.

Indeed, the unemployment rate has in recent times provided a good indication of where we are in the business cycle. Right now, it is clearly telling us we are nearing the latter stages, which in the past has marked the top in interest rates. Don’t get me wrong, the Fed will proceed to raise the Fed Funds Rate for the foreseeable future and proceed with reducing their balance sheet, but, as notes by Alex Gurevich, “When unemployment levels get very low there is less possibility and room for growth, coupled with the Fed getting aggressively tighter to avoid a “wage spiral” (and quell inflation overall), but, the reality is, it is through these actions that growth comes to die.”

Again, this is where bonds could begin to provide some value as 2022 progresses. As noted by Teddy Vallee, whether or not bonds appreciate on an absolute basis as much as once would have remains to be seen, but relative to broad equities they are beginning to appear quite attractive.

Source: Teddy Vallee

Indeed, slowing growth has long been a tailwind for bonds.

Source: Andreas Steno Larsen

Source: Julian Bittel

As the business cycle slows, yields will eventually follow suit.

Source: Acheron Insights, FRED, 42 Macro

As will inflation. The evidence suggests this will likely be the story for the second half of 2022.

Source: Mr. Blonde Macro

Indeed, the current inflation pressures won’t be able to escape the business cycle forever. Meanwhile, investors have seemingly priced in nearly every bearish outcome for bonds, whereas the market internals now seemingly confirming what the business cycle is telling us and are too beginning to diverge from consensus.

The divergence between bonds and utilities relative to regional banks is striking. What this could mean for yields is clear.

Source: EPB Research

Represented differently, the performance of regional banks relative to the S&P 500, generally an excellent barometer for the direction of rates, have also diverged negatively.

Likewise, the copper to gold ratio has not confirmed this latest move higher in yields. Ever the markets macro barometer, the copper to gold ratio has a fairly solid track record of the direction in yields and was calling for higher yields for much of 2021. This is a notable non-confirmation in the new high in yields.

The performance of small caps relative to large caps is confirming this message.

Likewise, the ratio of cyclical versus defensive stocks has also diverged bearishly from yields.

The most economically sensitive sectors of the stockmarket as a whole are now pointing to lower yields.

Source: The Felder Report

Clearly, the markets are pricing in slower growth. Eventually, bonds will follow suit.

Indeed, when yield rise this far this fast and the 12-month rate of change exceeds 25% in conjunction with the 14-month RSI exceeding 70, we tend to see yields fall or at the very least plateau over the ensuing months. Again, yields cannot rise this fast without causing damage.

Though we are amid a bond market rout and inflation bonanza, bonds are starting to appear to offer a more attractive risk-reward profile over the next 12-months relative to broad equities. Again, as noted in the previously mentioned piece by Verdad Capital, we are amidst one of the worst drawdowns from treasuries in the past 70 years, with the subsequent six month returns in nearly all cases being positive and an average of 4.9%. Right now, bonds have a growth tailwind at their back, equities do not.

Source: Verdad

From a technical perspective however things aren’t so rosy for bonds. On the weekly chart, the 30-year yield has clearly broken through an important resistance level around the 2.5% area, though this breakout comes accompanied by another weekly DeMark 9 sell signal and waning momentum. Whether or not this proves to be a false breakout or the 30-year yield can flip 2.5% into a new level of support will be telling.

Should this breakout prove to be a head-fake and we break back below 2.5% in the coming months would for me be the trigger to go long bonds and prove my thesis correct. This is an important technical level to watch in the weeks and months ahead.

In regards to bonds themselves via TLT, we have clearly broken down from the important $130 support level. $115-$120 looks to the next key level of support to watch. If we break below $115, I suspect bonds will go much lower before they go higher, perhaps as low as $105. Such levels would appear attractive entry points given the growth and inflation dynamics highlighted above.

Risks To The Bond Trade

Like any trade or investment, there are a number of risks to be considered that may prove to be a headwind for one’s thesis. For a potential bond trade, there remains a number of risks which must be addressed.

Stocks & Bonds Correlation

Firstly, with the latest headline inflation reading coming in at over 8%, the negative correlation between stocks and bonds that has existed during this great bond bull run will simply continue to be non-existent until the rate-of-change in inflation subsides.

At what point could this negative correlation reassert itself, this looks to be around the 2.5%-3% level for core-CPI.

Source: Gerard Minack

Or, per the work of Darius Dale at 42 Macro, the negative correlation could seemingly reassert itself should headline-CPI fall back below 5%.

Source: 42 Macro

Though supply chain and commodity issues remain, waning demand, slowing growth and unfavourable base effects for the growth rate in inflation should in all likelihood prove to be a headwind too strong for inflation to bear come the second half of 2022. As such, at some point later this year we should see bonds again behave as the traditional diversifier and safe-haven asset they have been in recent times. Remember, the US dollar and the US bond market are still the most risk averse assets in the world.

Oversupply Of Bonds

Another significant risk for bonds at present is the clear oversupply of treasuries set to flood the markets as the Fed accelerates their QT program and contract their balance sheet. Though I have discussed how previous attempts at QT has seen bond yields actually fall as result of the market simply breaking under the weight of tightening financial conditions, there is of course no guarantee such a scenario will play out during this tightening cycle.

This is a significant risk to bonds that has been highlighted recently by former Fed trader and financial plumbing expert Joseph Wang. Put simply, as a result of the Fed shrinking their balance sheet, a record amount of Treasury Securities will flood the markets over the coming months. Based on Fed Chair Powell’s QT guidelines of a balance sheet reduction of $1 trillion per year and with Treasury issuance by the Federal Government set to remain historically higher at around $1.5 trillion per year, Wang notes that:

“This implies that non-Fed investors will have to absorb ~$2t in issuance each year for 3 years in the context of rising inflation and rising financing costs from rate hikes. Even the most ardent bond bulls will not have enough money to absorb the flood of issuance, so prices must drop to draw new buyers. In this post we preview the coming QT, sketch out potential investor demand, and suggest a material steepening of the curve is likely.”

This is a significant risk of bonds. Were the Fed performing QT without the backdrop of a growth slowdown, the upward pressure of interest rates exerted by QT and Treasury issuance would be even greater. Though this may indeed by the case, it could well prove true than QT once again breaks the economy and ultimately leads to yields rolling over.

For now, I do suspect QT will exert further upward pressure on rates and downward pressure on bonds, at least until something breaks.

Source: Joseph Wang

Have The Rules Of The Bond Market Changed?

Pondering whether the rules for the bond market have changed appears to be the culmination of the previous two points I have highlighted in inflation and an oversupply of bonds exacerbating the current sell-off. Indeed, as noted by Luke Gromen, despite the clear deteriorating growth environment bonds have yet to catch a bid.

Per Luke Gromen (via FFTT-LLC):

“In plain English, the potential rule change is this:

Post-Great Financial Crisis, when the Fed began removing QE, market participants shifted into long-dated USTs on the anticipation of the return of deflationary pressures in the absence of Fed QE.

This time, for the first time post-GFC, the US fiscal and debt situation has deteriorated to such a degree that in the ongoing absence of sufficient foreign buying of USTs seen since 2014, as the Fed pulls back on QE, UST yields are beginning to rise, potentially driven by supply and demand issues.

We are not completely convinced that the rules have changed… it is still theoretically possible that a massive global depression and stock market crash could drive risk assets into USTs, driving yields down.

However, we are increasingly leaning in the direction that there HAS been a rule change on this front, because of the lived experience of March 2020, when global stock markets crashed, and 12 days into that stock market crash, UST markets began crashing alongside stocks (i.e. UST yields up), due to insufficient UST buying in the face of massive foreign UST selling.”

This is a significant issue posed by Luke, and one in which we simply cannot yet know the answer. However, for a contrarian like myself, it seems as though Luke’s view is now becoming a little too consensus. I am not yet willing to fully write of bonds in the face of a slowing economy.

Still Too Early

So, given these risks, what could be the catalyst for a rally in bonds?

Firstly and most importantly, we would need the material deceleration in the growth cycle to commence, and, based on the short-term leading indicators of the growth cycle, such as ECRI’s Weekly Leading Index below, said deceleration may not materialise until the latter stages of Q2.

Source: Economic Cycle Research Institute

If we intertwine this idea of an impending growth slowdown with 30-year treasury seasonality, we can see that long-term yield tend to bottom around the March to April period, with the May to August months being the most favourable for bonds historically. Seasonality is suggesting the bond sell-off may be nearing an end.

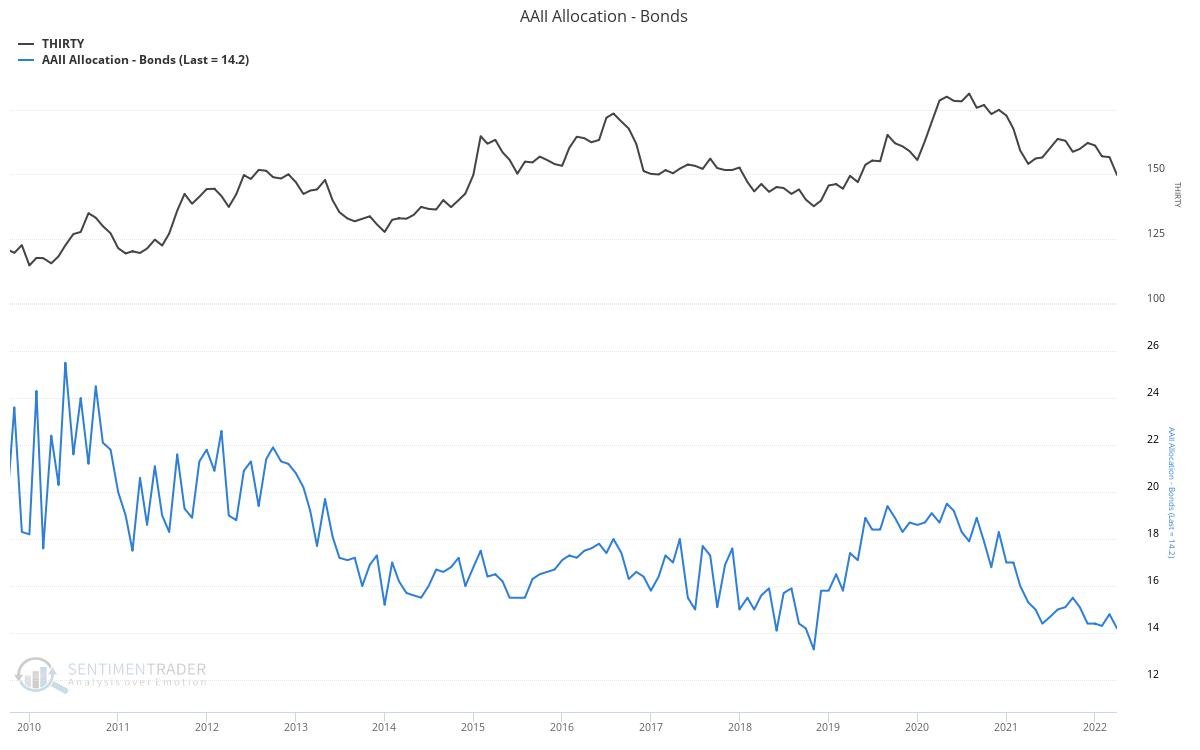

Further weakness in equities over the coming months (a likely scenario when growth continues to roll over) would also do well to have investors reconsider their allocations to fixed income. It is important to remember that, as a function of the TINA trade, investors are currently the most underweight fixed income exposure they have been in the past decade. Everyone is record underweight bonds.

This is a particularly important consideration for pension funds, as for the first time since 2008, their solvency ratio’s lie above 100% (as result of rising yields reducing the value of their liabilities and rising risk assets increasing the value of their assets). This observation was recently flagged by Alfonso Peccatiello, noting that pension funds “will need to lock-in some gains as they are still under-hedged when it comes to interest rate risk, and buying long-end bonds yielding close to 3% will reduce this interest rate risk and provide a hedge against drawdowns in risk assets.”

The longer-term bull market in bonds may no longer be the home-run trade it once was, but for now, the cyclical forces appear favourable for a rally over the next year or so. While the chart of truth breaking and the bond bull market ending is a very real risk, one that may yet occur in the next five years, I suspect we may be a tad early calling for the death of bonds.

Summary and key takeaways

- Current consensus is that inflation is out of control, interest rates are going to the moon and the Chart of Truth is broken. When it has become a standard narrative to talk about structural inflation and rates need to be raised to 10 plus percent, maybe we should start looking at things differently.

- This is the largest percentage increase in rates in all recorded history. There is simply so much priced into the rates market at present.

- The bond trade may not be the home run it once was during a slowing growth environment, but it may still provide a good hedge in the event of a significant deceleration in growth.

- Remember, the US dollar and the US bond market are still the most risk averse assets in the world. Increased geopolitical risks and slowing economy continue to make bonds look more attractive.

- The ideal setup for bonds is not here yet, but it may come sooner than you think.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.