SHORT ANSWER: The top investment options for young adults consist of index funds, real estate and retirement funds.

Most young adults would like to begin investing and saving for retirement but have no idea where to start. Whether you’ve just received your diploma, are starting your career or you’re ready to invest in an IRA or 401(k) account, we’ve created a guide to help you invest your money. Here are Benzinga's recommendations for the best investments for young adults.

Quick Look at the the Best Investments for Young Adults:

- Index Funds

- Real Estate Property

- Retirement Fund

- Eliminate Debt

- Higher Education

The Best Investments for Young Adults

Check out the best ways to handle your money, starting now.

1. Invest in Index Funds

The stock market is one of the best places to invest your money, but you may not understand how to value stocks, what stocks are worth purchasing and how to effectively diversify a portfolio to avoid losing money.

Index funds are prepackaged bundles of stocks that track a particular segment of the market. Many index funds track the S&P 500, which is an index that’s widely considered to represent the health of the economy of the United States as a whole.

Index funds offer novice investors an easy way to build a portfolio quickly with expert assistance. They frequently require lower fees when compared to other types of mutual funds because they are not actively managed by a team of investors and financial advisors.

Want to start investing in index funds? Check out some of Benzinga’s favorite brokerages and open an account.

- Best For:Forex and investing appVIEW PROS & CONS:securely through TD Ameritrade's website

2. Invest in Property

Many young adults who rent believe that they should buy a home as soon as possible. After all, if the price of rent and a monthly mortgage are comparable, why not own the property? Unfortunately, the rent vs. buy debate is about more than just the monthly mortgage price. Owning a home is a significant investment and one that should not be taken lightly.

For example, when you live in an apartment, you can call your landlord up to handle expensive home issues. A $4,000 furnace that dies in the middle of the winter is the landlord’s problem when you live in an apartment. When you own the home, there’s no one to call except the local heating repair company. Learning more about the true costs of home ownership can help you understand if you’re really ready to buy.

- Best For:Low Cost Real Estate InvestingVIEW PROS & CONS:securely through Diversyfund's website

- Best For:Diverse Range of Alternative AssetsVIEW PROS & CONS:securely through Yieldstreet's website

3. Start a Retirement Fund

Back in the 1950’s, it was a common practice for employers to take care of their employees after they retired with a generous pension plan crafted by the company in exchange for years of service.

As people began living longer and wages failed to keep up with inflation, it slowly became the responsibility of employees to handle their own retirement funds through contributions to a 401(k) or Individual Retirement Account (IRA).

Baby Boomers face a serious problem — many do not have enough money to make it through retirement and are forced to work past the retirement age of 66. Young adults who begin saving now can avoid this problem by growing their money over time.

- Best For:Comparing AdvisorsVIEW PROS & CONS:securely through SmartAsset Financial Advisors's website

4. Eliminate Debt

If you’re a Millennial or Generation X member, chances are that you’ve got some kind of debt. According to a survey from Young Adult Money, 43% of young adults have some form of student loan debt and 83% of those with student loan debt say that paying back their debts seriously affects their ability to meet their other financial goals.

Even if you haven’t taken on any student loan debt, credit card debt may still lurk on your credit profile — 7 out of 10 young people constantly carry a balance on their credit cards and 50% say they have too much debt.

Debt does nothing to help your financial situation, and if left unchecked, accumulating interest can cause you to pay sometimes twice your principal balance by the time the debt is repaid. If you have a student loan, an outstanding auto loan or an unpaid credit card balance, paying it off can set you up to more effectively meet your investing goals.

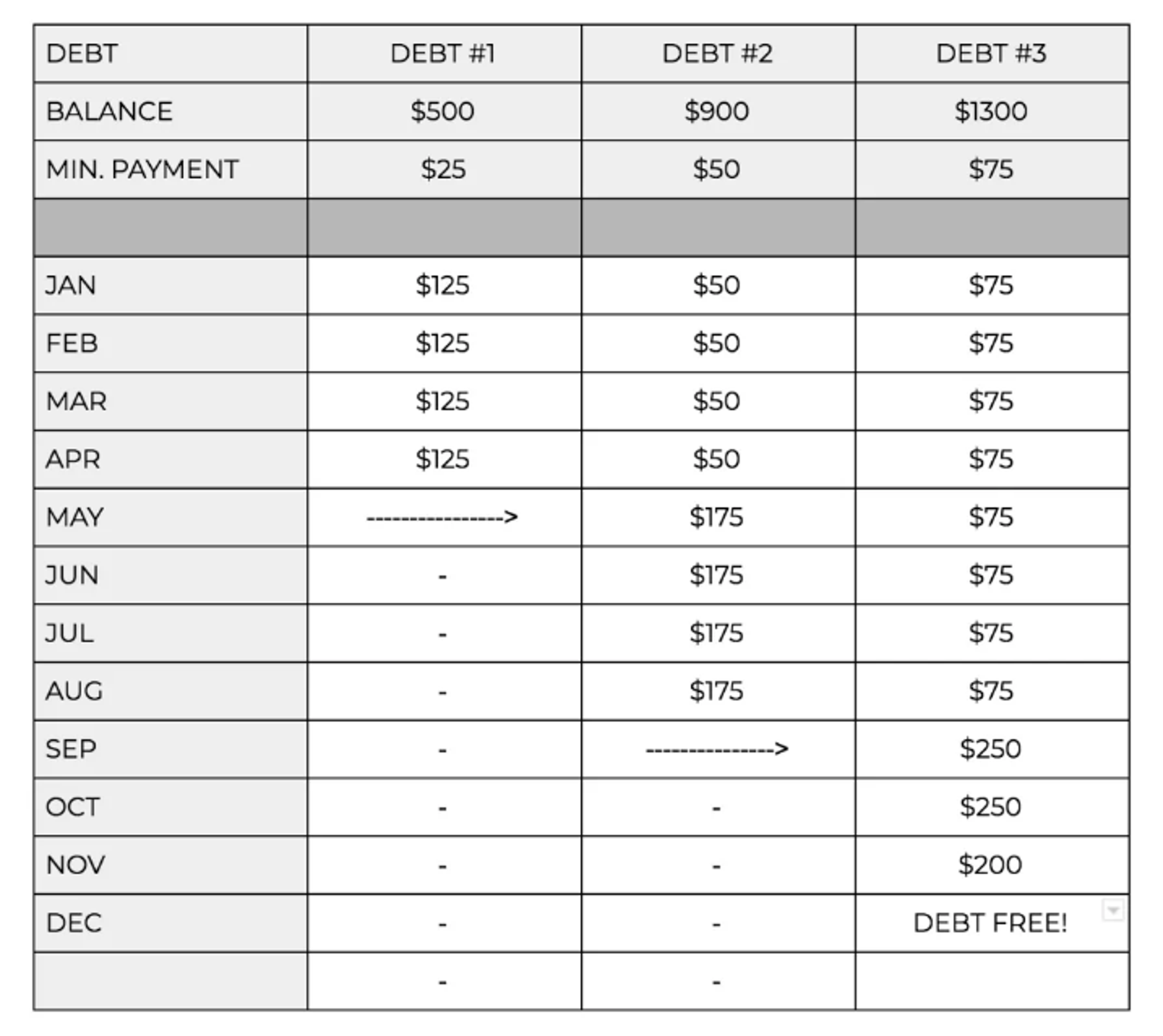

Have more than one debt you need to pay off? Use the “snowball method” to slowly reduce your debts over time without missing a minimum payment. Identify your smallest debt and put all of your available funds toward reducing the debt while you pay the minimum balance on your other outstanding accounts.

After your smallest debt has been paid in full, devote all of your funds to your second-largest debt and so on until you are debt free. While paying off your debts is not an investment in the traditional sense, eliminating your debts will set you up to be in the best possible position to save more in the future.

5. Invest in Higher Education

Young adults today are a part of the most educated generation of Americans ever. The decision of whether or not to go to college is one of the most difficult (and expensive) decisions that you'll ever make. Some of the factors that may make a university education worth the investment:

- You’re interested in pursuing a career that requires a degree. Some occupational pursuits (like jobs in the medical or legal field) require you to hold an advanced degree. In most other fields, individual employers choose to give more weighted consideration to applicants who have a college degree.

- You’re looking to move up your current corporate ladder. Most corporations hire entry-level employees without higher education. However, if you are unsatisfied in your current role, earning your degree can open the door to consideration for a higher position. Ask your employer about the company’s tuition reimbursement program. Many employers will help student employees with the cost of tuition or other learning.

- You can’t find a job in your field. If you can’t seem to find a job that covers your bills in your area, an advanced degree can help you begin a new career. According to data from the U.S. Bureau of Labor Statistics, those with a bachelor’s degree typically have a higher median income and have less trouble finding gainful employment.

If you’ve decided that a college education is a good investment for you, researching local scholarships is a great place to start. Each year, thousands of dollars of scholarship money goes unclaimed because no one applies for them!

6. Get a Robo Advisor

When you invest, you need a broker. Why not choose a Robo advisor, also called an automated investing service or online advisor? Robo advisors function by using computer algorithms and advanced software to build your investment portfolio. Your Robo advisor does everything for you with little human interaction required.

When you opt for a traditional broker or financial advisor, you pay more money. Robo advisors' low costs let you get started cheaply and quickly. You can often input your contact information and get started investing right away.

The Importance of Investing Early

Nearly every financial expert will tell you that one of the most important steps you can take is to begin investing and saving money early. The benefits of getting started early include the following concepts, which you can deploy in your own time.

Compounding Interest

Compounding interest is a fancy way to say “interest earned on the interest that you’ve previously accrued” and it’s a powerful force when it comes to building wealth.

Let’s say that you invest $5,000 a year beginning at age 25 and stop investing when you turn 35. Assuming a rate of 7% interest, you would have a whopping $602,070 by the time you retire — without saving another dime past the age of 35!

Compare that to someone who doesn’t start saving until 35 but saves $5,000 annually from age 35 to 65. In total, this older saver will have invested $150,000 (three times the amount you did) and will still only have $540,741 by retirement. The earlier you invest, the more effectively you can take advantage of the principles of compounding interest.

A Fighting Chance Against Inflation

In the year 1958, the average price of a home was $10,450, gasoline was $0.52 a gallon and a brand new car would set you back anywhere from $1,967 to $3,929.

As a general rule, money becomes less valuable over time due to inflation. Investing at a younger age can help you outpace inflation by accumulating interest.

Tackle Investing When You're Young

The best investments for young adults is to save often and early and to learn to live within your means. Put away more money now and learn about your investment options to improve your chances of financial success in the future.

Frequently Asked Questions

What are suitable investments for a young person?

Young people may want to consider investing in index funds, REITs and buying a property.

Is it wise to start investing when you are young?

Investing when you are young gives you the time, flexibility and time for your invested money to compound.

Should I start investing when I have debt?

For the best success, you should eliminate your debt before you begin investing.

About Sarah Horvath

Sarah Horvath is a seasoned financial writer with a specialization in investing content. With a keen eye for market trends and a deep understanding of investment strategies, Sarah delivers insightful and informative articles tailored to investors. Her dedication to providing valuable content empowers readers to make informed decisions in the dynamic world of finance. Sarah’s expertise extends across various investment vehicles, including stocks, bonds, cryptocurrencies, and real estate. Whether analyzing market movements, evaluating investment opportunities, or demystifying complex financial concepts, Sarah’s writing is characterized by clarity, accuracy, and actionable insights. Through her engaging content, Sarah strives to educate and guide investors on their journey towards financial success.