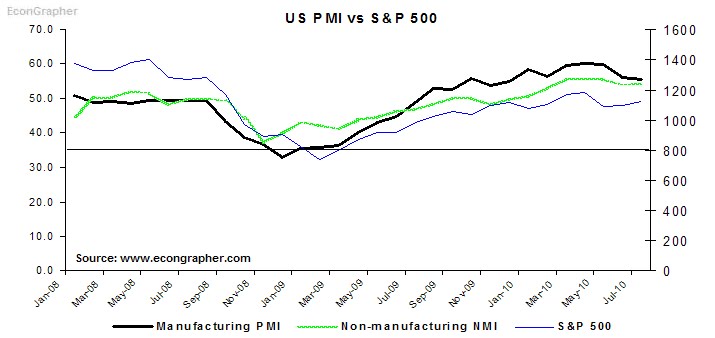

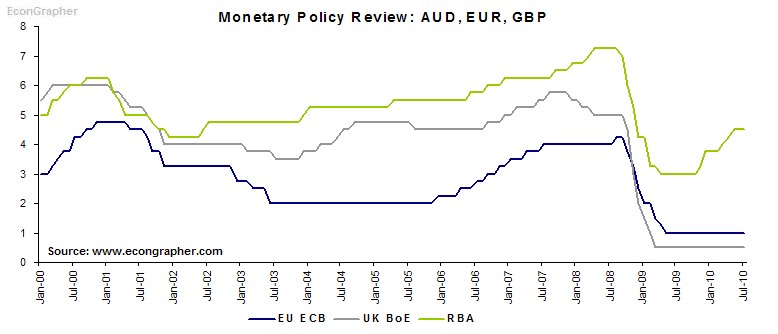

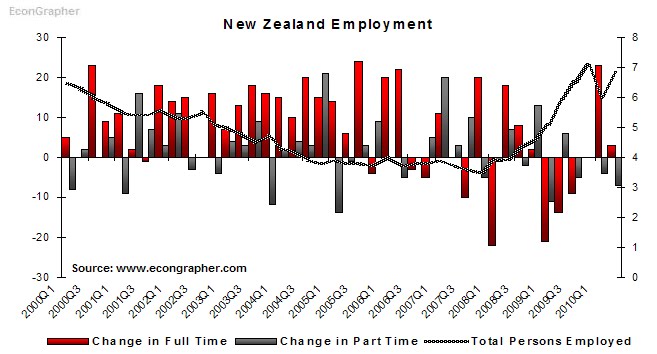

This week we look at the faltering PMI stats from China, and a relatively stable but mixed PMI result from the US for July. We then review the monetary policy decisions this week from the RBA, BoE, and ECB, then we analyze the employment reports from the US and New Zealand.

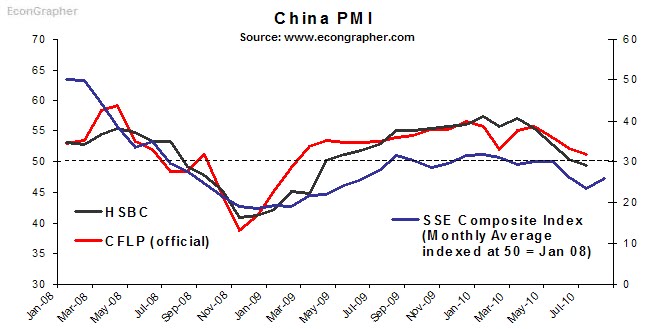

1. China PMI

The Chinese PMI indexes both fell in the July reading, with the official CFLP index falling to 51.2 from 52.1, and the HSBC index dipping below 50 for the first time since March 2009, at 49.4 vs 50.4 in June. The PMI numbers are showing an easing of industrial activity in China, but the numbers are still above the low point reached late 2008 to early 2009. The July industrial production result is likely to come in lower again next week when the monthly data release comes out (which also includes CPI, fixed asset investment, PPI, and retail sales). The biggest question around the PMI result is whether or not it's temporary; is it a seasonal movement? is it the result of artificial tightening moves? or is it a more fundamentally driven decline? Next week will surely bring extra pieces to the puzzle.

© 2026 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.