Make a quick mental list of your New Year’s resolutions. Is saving money high on your list? If it is, know that saving is a daunting task for most of us, especially if you’re knee-deep in some entrenched habits (like spending without a budget). However, you can do it, and Benzinga will help.

There are literally thousands of savings vehicle options for just about any type of saver, whether your goals are six months from now or 30 years away.

What it Takes to Save Money

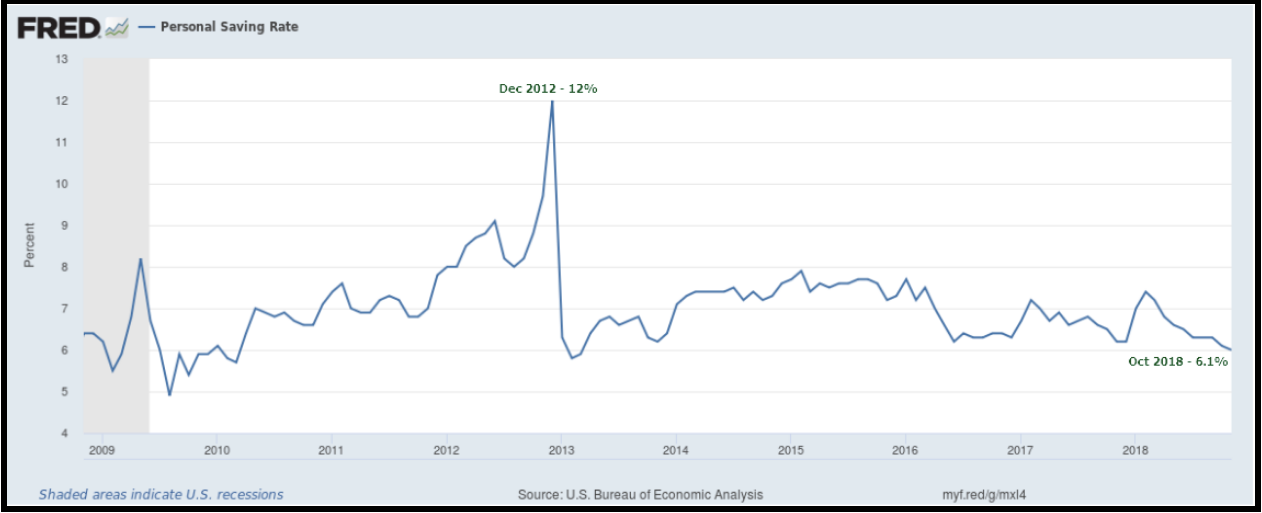

According to the Federal Reserve Bank of St. Louis, the personal savings rate of Americans as a percentage of disposable personal income (DPI) dropped from 12% in December 2012 to nearly half that amount (6%) by October of 2018.

We all save for different reasons. You might save to meet day-to-day expenses, emergencies, vacations or other special events for the future.

Like any successful project, saving money requires a well-thought-out plan and major commitment. Even before you start putting that plan together, it’s imperative that you understand why saving money is so important.

So, how do you start saving money? Benzinga has compiled practical and savvy plans to help you reach your yearly goals.

Step 1: Have a Plan

All good things, including saving money, begin with a plan. Starting a plan is as easy as deciding your goal. How much money do you wish to save and what is the timeframe to accomplish that goal? Consider both short- and long-term savings goals. Best of all, you don’t need expensive software to help you set goals – your bank might offer you its tools for free.

Without clear-cut milestones to guide you, you’ll never know whether your money-saving efforts are a success. More importantly, the plan will help you realize if you are falling short – and by how much, so you can quickly act to get back on track.

Step 2: Begin Budgeting

The first step to implement your money-saving plan is to establish a budget. Budgeting involves establishing realistic targets such as spending on take-out or shopping for clothes.

First, Review Your Income and Spending

Keep track of your paychecks as they come into your bank account. Next, watch how much you spend each month, making sure you never exceed your income. Ideally, your total spending should be less than what you earn. Any excess can then be set aside to meet your saving goals.

Next, Analyze Your Spending

Go through each transaction in your checking account or credit card statement and make sure you update the “actuals” in your budget. Use technology to help you with your budgeting. Most banks and financial institutions will offer you free online budgeting websites and apps.

Part of the analysis process over time is to identify spending that you can either cut back or reduce. Then, divert that money to savings.

Finally, Make a Budget and Stick With It

The only way budgeting can help you save money is if you stick to it. It’s challenging to always meet your budget, but if you want to save, you need to be disciplined.

For instance, if you notice you’ve exceeded spending for the month on a certain line-item like gas or lunch, try and reign it in next month. Use your bike or public transport to get to work for a few weeks, or bring lunch from home for a month.

The secret to saving money through budgeting: Plan. Track. Cut back. Repeat!

Step 3: Store Excess Money Properly

If you’ve managed to stick with your budget, then you’ll likely have some excess money available to save at the end of each month. The next challenge is where to store your extra savings – at least until you are ready to take your savings plan to the next level.

Here are some options to consider:

Checking accounts: Checking accounts are the most common vehicle used by savers to “park” excess funds. However, because they offer low (or no!) interest rates, you may not want to store excess money there for long. Additionally, the bank fees associated with managing and administering these accounts might eat into the savings you’ve fought so hard to accumulate.

Savings accounts: This is another option where you could temporarily save money, especially if you’ll continue to write checks or make ATM (or online) transactions against those funds. With a savings account, you’ll likely earn slightly more in interest than a checking account – but once again, you’ll be paying fees by the transaction.

High-yield savings accounts: These accounts are a great way to store money and get rewarded while you wait and decide how to put those savings to work. Not only do they offer liquidity in the event of an emergency, but they also offer higher interest rates and the convenience of a checking account. You may, however, need to maintain a higher minimum balance to take advantage of those higher rates. Before you open an account, learn more about the high-yield online savings account that’s best for you.

Whether you store excess money in a bank or credit union can also help boost your savings efforts. Learn more about banks vs. credit unions before deciding where to park your money.

Earn rewards on routine purchases:

Upside is a simple and free app that allows you to earn cash back on many of the things you already do. Basically, when you use the app, you can see returns from activities like: gas, groceries, dining and more

When you earn these rewards, you can cash out with a: direct deposit, PayPal deposit or gift cards from Amazon, Target, Starbucks and more.

You can download the app to your Apple or Android device, claim offers that appeal to you and wait for the reward to appear in your account—it usually takes 2 to 4 days. Plus, you can earn up to 3x the cash back you would normally get on particular programs, spanning more than 50,000 businesses.

Step 4: Once You’ve Saved Enough, Start Investing

If you’ve got your savings safely tucked away and growing, it’s time to consider investing what you’ve saved. Revisit your savings goals and decide which of the following investment options is right for you.

Short Term Savings

Short term savings goals (1 to 3 years) are best accomplished through safe vehicles. Know that “safety” is relative to your risk-taking ability, and may not give you the same returns that high-risk investments offer. Here are some options to consider:

- Money market funds: These are among the safest investment choices, but the returns they offer are some of the lowest available.

- Bonds: Bonds offer better rates of return than most checking or savings accounts, and the funds are safe if held until maturity – especially if you invest in U.S Treasury or blue-chip corporate bonds. However, you run inflation and interest rate risks with bond investments.

- Certificates of deposit (CDs): Like bond investments, certificates of deposit are another great way to safely save for the short term. Upon fixed term maturity, you not only get all your money back, but the interest and principal continue to compound over the term.

- Stocks and ETFs: If you’re willing to take on more risk, stocks and ETFs might be great short term investment vehicles. You could start trading stocks, but that requires more skill and a lot more risk. A good compromise might be to invest in bond and equity ETFs.

If you’re new to investing, it might be a good idea to learn how to start day trading and investing before taking that next step.

Long-Term Savings

You can achieve your long-term retirement goals by investing in vehicles that grow over long periods of time – perhaps 15 or 20 years or more. Some of the most popular investment options for long-term investment include:

- Traditional and Roth 401(k) plans: These investment vehicles enable employees to save money and invest it for retirement. Roth 410(k) contributions are post-tax, while a traditional 401(k) is pre-tax money. Savings in both plans grow tax-deferred. Some workers might also have access to employer-matched contribution 401(k) plans.

- Traditional and Roth IRAs: In a traditional IRA, you get a tax break immediately in the year of contribution, but you’ll pay tax on withdrawals in retirement as ordinary income. Roth IRA contributions occur through after-tax dollars, but withdrawals in retirement are tax-free.

All these instruments offer various investment choices such as stocks, bonds, mutual funds, ETFs and more. If you expect to be in a lower tax bracket in retirement, then a traditional IRA may be for you. Roth IRAs may be good for those who expect to earn more and pay more taxes in retirement.

Carefully consider which is the best Roth IRA or 401(k) account or the most suitable traditional IRA or 401(k) account before making your decision.

Here are some of Benzinga's favorite IRA providers.

- Best For:Socially Responsible InvestingVIEW PROS & CONS:securely through Ally Invest's website

- Best For:Forex and Investing AppVIEW PROS & CONS:securely through TD Ameritrade's website

Final Thoughts

Saving money can be challenging, but if you plan carefully and execute diligently, it’s possible to save – even on a limited income. Constantly review your plans and your savings accomplishments and refine them as you go. You’ll get more for your efforts if you use the automated saving feature that most checking or savings accounts offer.