Have you accumulated significant credit card debt over time? Now might be the ideal moment to consider consolidating that debt. Debt consolidation means that you combine multiple debts under a single account and debt instrument. It also means you could save yourself a lot of stress and money, too.

There are several strategies that you can use to consolidate and repay your credit card debt. We’ll cover several options and highlight when each may be appropriate.

Quick Look: Best Ways to Consolidate Credit Card Debt

- Personal Loans from: Sofi, Figure or Lightstream

- Balance Transfer Credit Cards from: Navy Federal, U.S. Bank or Capital One

- Home Equity Loans from: Unlock, PenFed or Bank of America

- Debt Management Plan like: Accredited Debt Relief

- Withdraw From Retirement with: Schwab, Facet or Rocket Dollar

Ways to Consolidate Credit Card Debt

There are several strategies you can employ to get control of your finances and simplify the debt repayment process. By understanding these options and selecting the one that best fits your financial situation, you can take the necessary steps toward credit card debt consolidation and achieving your long-term financial goals. Here are five ways to help you consolidate your credit card debt.

1. Get Personal Loans

- Best For:No origination feesVIEW PROS & CONS:securely through SoFi Personal Loans's website

- Best For:Quick fundingVIEW PROS & CONS:securely through Figure Personal Loan's website

Looking for a way to pay off credit card debt in full using a cheaper alternative? If so, then a personal loan might be the best option for you.

You’ll need to work with your bank, credit union or another lender to secure a personal loan. If you have a good credit history, this type of loan should come with a lower interest rate than most credit cards. You can use the funds to pay off all your credit cards and the only debt you’ll owe will be your lower interest-bearing personal loan and depending on the provider, it won’t impact your credit score.

Though you might make smaller payments regularly, the duration and the size of the loan can make it more expensive over the term of the loan than your credit card debt, so you need to do the math before opting for this strategy.

Let’s use an example to illustrate this point. Assume you owed $10,000 on a credit card debt that charges you interest at 14.25% annually (compounded monthly). If you paid that debt off in 5 years (60 months), here’s what you would end up paying once you settle your debt in full:

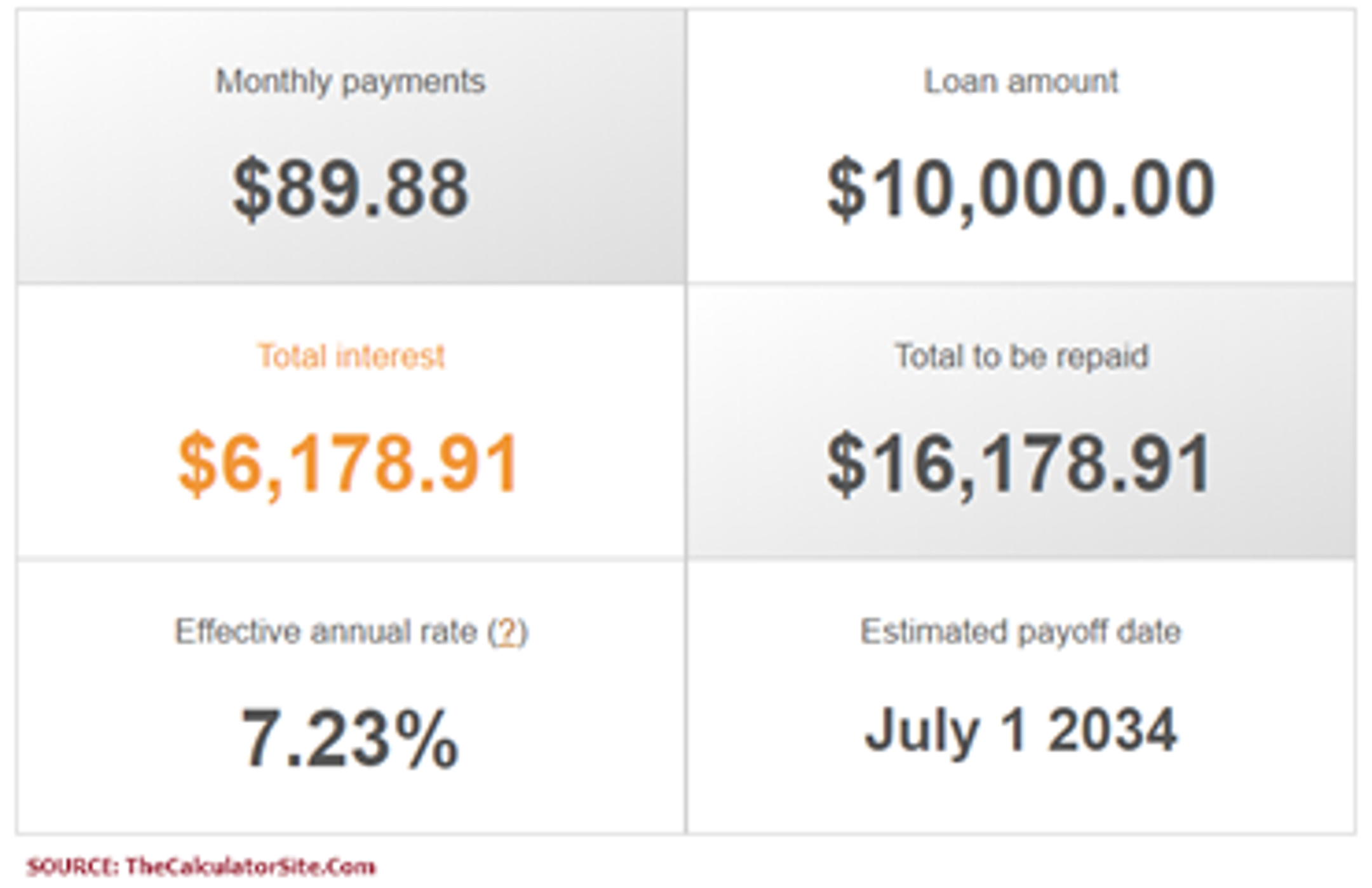

Now, assume you took a personal loan of $10,000, at an annual interest rate of 7% (assuming you have a fair credit score) and used the proceeds to pay off your credit card debt immediately. However, since you are only paying $89.88 per month to service this new debt (as opposed to $233.98 for the previous credit card balance), you decide to repay the loan in 15 years (instead of 5 years for the credit card balance).

Here’s what you would end up paying by the time you fully pay off your personal loan:

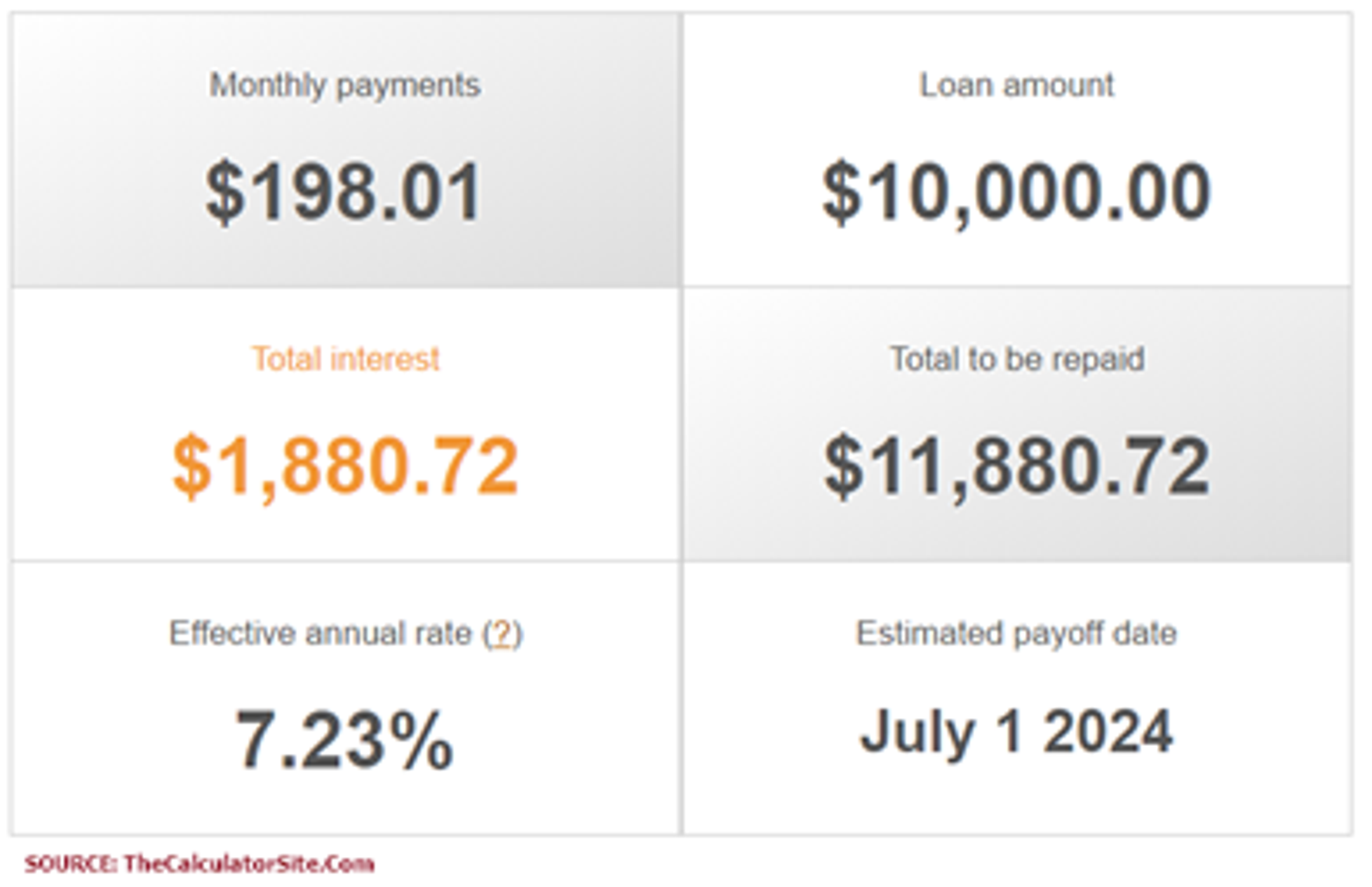

Paying smaller monthly installments over a longer time frame causes you to pay $2,140 more than what you would have repaid on your credit card debt repayment plan. On the other hand, if you plan to repay the personal loan within a 5-year period, you could save more than $2,158 on your debt repayment.

This strategy only makes sense if you want to immediately use the proceeds from the lower-interest loan to pay off the credit card debt and then quickly pay off the personal loan.

Next, compare interest rates and terms from multiple lenders and visit a loan company of your choice to discuss the details. Do an assessment of your credit card debt. Work out how much you owe, what the size of your personal loan will be and when you plan to repay that debt.

Note: You could also get a personal loan from generous friends and/or family members instead of a financial institution.

2. Use Balance Transfer Cards

If you owe money on several high interest-bearing cards and are not comfortable taking on a personal loan to settle that debt, then you might benefit from a balance transfer (BT) credit card. These types of credit cards allow you to transfer outstanding balances from multiple credit cards (or other loans) onto a single balance transfer credit card, thereby simplifying management and payment of that single debt.

Many credit card issuers offer 0% introductory interest rates on balances transferred to them from other credit card companies. Are you paying 18% or 20% on your existing credit cards? Transferring all those balances to a 0% card makes sense.

This strategy only works well if you have a plan in place to pay off the entire balance transferred within the introductory 0% interest period. Typically, the 0% interest lasts for a limited period. Interest rates could then potentially be higher than what you are paying on your existing cards. There may also be balance transfer fees associated with making each transfer, which could be a minimum dollar amount or a percentage of the amount transferred.

Luckily, this method won’t impact your credit score, but avoid using the balance transfer card for regular credit transactions because those will be interest-bearing immediately and not subject to the introductory 0% interest period. You could end up taking on higher-interest debt in exchange for comparatively lower-interest debt consolidation option.

Find a BT credit card with the longest introductory period and the lowest post-introductory APR. Do the math to decide whether it’s is still a viable credit card debt consolidation/transfer option for you.

Use the issuer’s online pre-qualification tool (most issuers have one) to confirm whether you’re eligible to apply for the BT card of your choice. Several factors, including your credit score, could preclude you from applying for one, and this is not like a traditional debt consolidation program because you decide how quickly you’ll pay off this debt, where a debt management program generally puts you on a strict timeline.

3. Borrow Against Your Home

- Best For:Homeowners With Limited Cash FlowVIEW PROS & CONS:securely through Unlock's website

Have you built significant equity in your home? You might be able to unlock some of that value to help pay down consolidated credit card debt through a home equity loan or home equity line of credit (HELOC). Both of these are a type of second mortgage.

You’ll likely need a good credit score to qualify and you may need to wait a while after you get a mortgage to qualify for a HELOC. But there’s an upside. While paying off your credit card debt isn’t tax deductible, you might be able to write off all or some part of the interest on your tax returns.

Just as you would do for a personal loan, you can work with a bank/financial institution to get a home equity loan or HELOC. The physical assets serve as collateral against the amount borrowed. If you default on a payment, those assets can be repossessed and sold by the bank and the proceeds used for settling the loan. Typically, because these are secured loans, interest rates are lower than those paid on credit card balances. Once you have the loan, use it to repay all your high-interest credit card balances first.

Keep in mind that when you implement this strategy, you swap unsecured credit card debt for secured debt. If you’re ever unable to repay the loan, the lender can seize your home as repayment. Even if you manage to pay off the consolidated credit debt, failure to subsequently repay the secured loan in full can hurt your credit profile.

At the same time, a home equity loan could be rolled back into your mortgage, thus reducing your payments and extending the payment period. A borrower who plans to stay in their home could try this method, especially for consolidating credit card debt or massive unpaid student loans—mortgage rates are generally much cheaper than personal loans or credit card rates.

4. Try a Debt Management Plan (DMP)

The best way to save money is to exercise spending restraint. If you can’t stop spending, a credit counselor-assisted debt management plan (DMP) might be what you need.

Typically, DMPs are a last resort recommendation from credit counseling professionals. Counseling services initially aim to help you better manage your debt through financial education and money management discipline. However, these nonprofit organizations can also work with your credit card companies to consolidate all your debt into a single (monthly) payment.

You pay that installment to the counseling agency and they disburse it to the various credit card companies on your behalf. They may also be able to negotiate lower interest rates on your credit card debt or work out a deal for you to pay smaller installments. But there are a few downsides:

- If the negotiated settlement involves writing off some of your debts, the credit card issuers may ask credit rating agencies to make a notation of that fact in your credit file. Should that happen, it might impact your credit score.

- You, not the agency, are still responsible for paying all of your negotiated debt. If the counseling agency misses a payment, for instance, as a result of an administrative issue, it will reflect poorly on your credit report.

Find a credit counselor accredited by the National Foundation for Credit Counseling (NFCC) and discuss your debt situation. This is usually a free service but there may be fees attached to the ongoing administration of your DMP.

5. Try Accredited Debt Relief

- Best For:$20k + in DebtVIEW PROS & CONS:securely through Accredited Debt Relief's website

Accredited Debt Relief is platform designed to help you manage your debts without a loan. You can avoid bankruptcy or experience financial freedom when you set up your savings account with Accredited Debt Relief and make deposits to pay off your debts. The platform negotiates on your behalf, helps you become debt free and doesn’t get you wrapped up in a loan.

6. Withdraw from Your Retirement Savings

- Best For:Holistic Approach to Retirement SavingsVIEW PROS & CONS:securely through Charles Schwab Retirement's website

- Best For:Experienced InvestorsVIEW PROS & CONS:securely through Rocket Dollar Retirement's website

If you find all other credit card debt consolidation options discussed here untenable, you could dip into your retirement funds as a way to pay off all your credit card balances. This is a good option if you don’t want to take on new personal debt to settle older credit card debt. However, since this could have a significant impact on your long-term finances, you should only consider this option as a last resort for personal debt consolidation.

You could withdraw funds from a qualified plan, such as a 401(k) or individual retirement account (IRA) and use it to pay down your credit card debt. You won’t need to worry about your credit score because dipping into your retirement plan won’t affect your score. Depending on your financial circumstances, however, you may need to pay an early withdrawal fee. The amount withdrawn may also be fully taxable.

Understand all applicable rules associated with making such early/hardship withdrawals from your plan. Next, speak with your plan administrator to get the ball rolling and check to see how much money you have in your qualified plan. Only 50% of your balance is eligible for withdrawal. You must also re-contribute the amount withdrawn back into the plan within a particular time.

Why Consolidate Credit Card Debt?

Despite using your favorite budget app to help you manage expenses, you might find that you use your credit card all too frequently. Before you know it, you’ve accumulated a lot of debt on several credit cards and you’re having trouble juggling all your payments.

It may make perfect sense to try debt consolidation so you can manage multiple payments. You also might inadvertently miss a payment, which could adversely impact your credit score.

Credit card debt consolidation might also be a good option for anyone who owes more on their credit cards than they can afford to repay. Through consolidation, you could potentially reduce your overall debt. Credit card debt consolidation also helps restructure repayments into more affordable (smaller) installments.

Put Thought to Your Consolidation Plan

Unfortunately, it might not be feasible to use a single strategy to consolidate and pay off debt with large amounts. Your debt might exceed the amount of money you are eligible to borrow against an unsecured personal loan. In that case, you need to give thought to which other strategies you might use to complement a personal loan and deal with your debt.

For example, you may want to use the snowball method, but you also need to reduce household debt so that you have more money for routine expenses or special things that you feel your family deserves. Your debt consolidation strategy should consider what you WANT versus what you NEED. A financing option like a home equity line or credit could help with other expenses while also paying down your debt load. Plus, you can reduce your credit utilization rate while seeking approval for a much larger loan.

Also, consider what impact a delay in paying off that debt might have on your overall financial plan. For instance, if you choose a BT transfer option and are unable to pay off your balance in full within the introductory period, how will you deal with 25% post-introductory period interest rates?

Finally, try to avoid debt consolidation plans that simply result in swapping old debt for newer debt unless you have a plan to quickly pay it off. You may want to reach out to a debt collector to work out a deal before you every get this far, but that all depends on the installment payments you can make, other credit card payments you will be making, miscellaneous debt balances, your emergency fund, savings balance, potential tax refunds and credit card accounts you want to keep open.

Consolidating and paying off your credit card debt isn’t necessarily a silver bullet for your debt challenges. You’ll also need a long-term plan to help you use credit cards responsibly and to manage that debt effectively.

Want to learn more about budgeting or paying off debt? Check out Benzinga's picks for the best budget spreadsheets, the best online budgeting classes and the best expense tracker apps.

Frequently Asked Questions

Will credit card debt consolidation affect my credit score?

Initially, applying for credit card debt consolidation may result in a temporary dip in your credit score due to the inquiry and new credit account. However, if you make consistent monthly payments on time, your credit score can improve over time.

How long does it take to pay off credit card debt through consolidation?

The time it takes to pay off credit card debt through consolidation depends on factors such as the total amount of debt, the interest rate, and the monthly payment amount. It can take several months to several years to fully repay the consolidated debt.

Can I still use my credit cards after consolidating my debt?

After consolidating credit card debt, it is generally recommended to avoid using the credit cards that were included in the consolidation. Instead, focus on making payments towards the consolidated loan or credit card to accelerate debt repayment.