When buying or refinancing a home, we are often faced with a host of potentially life-altering decisions, like: Which lender should I work with? Which child deserves the bigger bedroom? Will I be left with enough room in the budget to buy that convertible with the cream leather interior? and so on. Making these calculations in addition to normal everyday life can be exhausting. As a result, other important considerations, like: what’s the best term for my mortgage? Should I look at a Federal Housing Administration (FHA) loan? What are VA interest rates? What is the interest rate risk? Can I find the interest rates for home loans on a mortgage rates chart? can fall by the wayside.

I’m here to tell you that choosing the right term for your mortgage can be equally important as budgeting for that dream car. At today’s interest rates on a $300,000 loan, the difference in total interest paid between a 15 and 30-year mortgage is over $150,000. No small amount for these fixed-income investments.

So what makes one program better than the other?

The answer is your goals. Understanding your goals, both personal and financial, and comparing them to the information in this article is a great way to determine whether a longer or shorter loan term is right for you.

15-Year Fixed

Congratulations! The mere fact that you are able to consider a 15-year note means you have a healthy income and low expenses and are able to go the “financially responsible” route. The question is, after considering all factors, how financially responsible is it really?

Strengths

- Lower Interest Rate

The main advantage of a 15-year mortgage is that it carries a lower interest rate than its longer-term counterparts. Yes, while 25 and 20-year terms offer a marginal discount from the 30-year fixed, the 15-year will offer you the greatest savings compared to your larger monthly commitment. Today, you can expect between a 10% to 15% lower interest rate on a conventional 15-year vs a 30-year fixed.

Assuming the difference will be somewhere in the middle of that range, here is what the interest savings would look like on a $300,000 loan over time.

Figure A:

Total Interest Paid

| 30-year at 5% | 15-year at 4.375% | Total Savings | |

|---|---|---|---|

| 5 years | $72,114 | $57,430 | $14,684 |

| 10 years | $137,282 | $95,552 | $41,730 |

| 15 years | $193,535 | $109,655 | $83,880 |

| 30 years | $279,769 | $109,655 | $170,104 |

From the table you might note that your savings increase exponentially over time; the longer you hold onto your loan/ home, the greater your incentive to choose a 15-year with lower interest rates. Mortgage borrowers who can take advantage of these rates should.

2. Amortize Faster (Payoff Faster)

If your goal is to pay off your mortgage, eliminating your monthly payment altogether, a 15-year mortgage can make a ton of sense. In fact, you will pay off your mortgage in exactly half the time (duh), while only contributing 41% more per month in this example. What’s less obvious, however, is the effect of amortization.

If you aren’t familiar with loan amortization and how it works, you should get familiar fast. Many people think that equity is built in a linear fashion. The reality is that building ownership is tilted exponentially against borrowers.

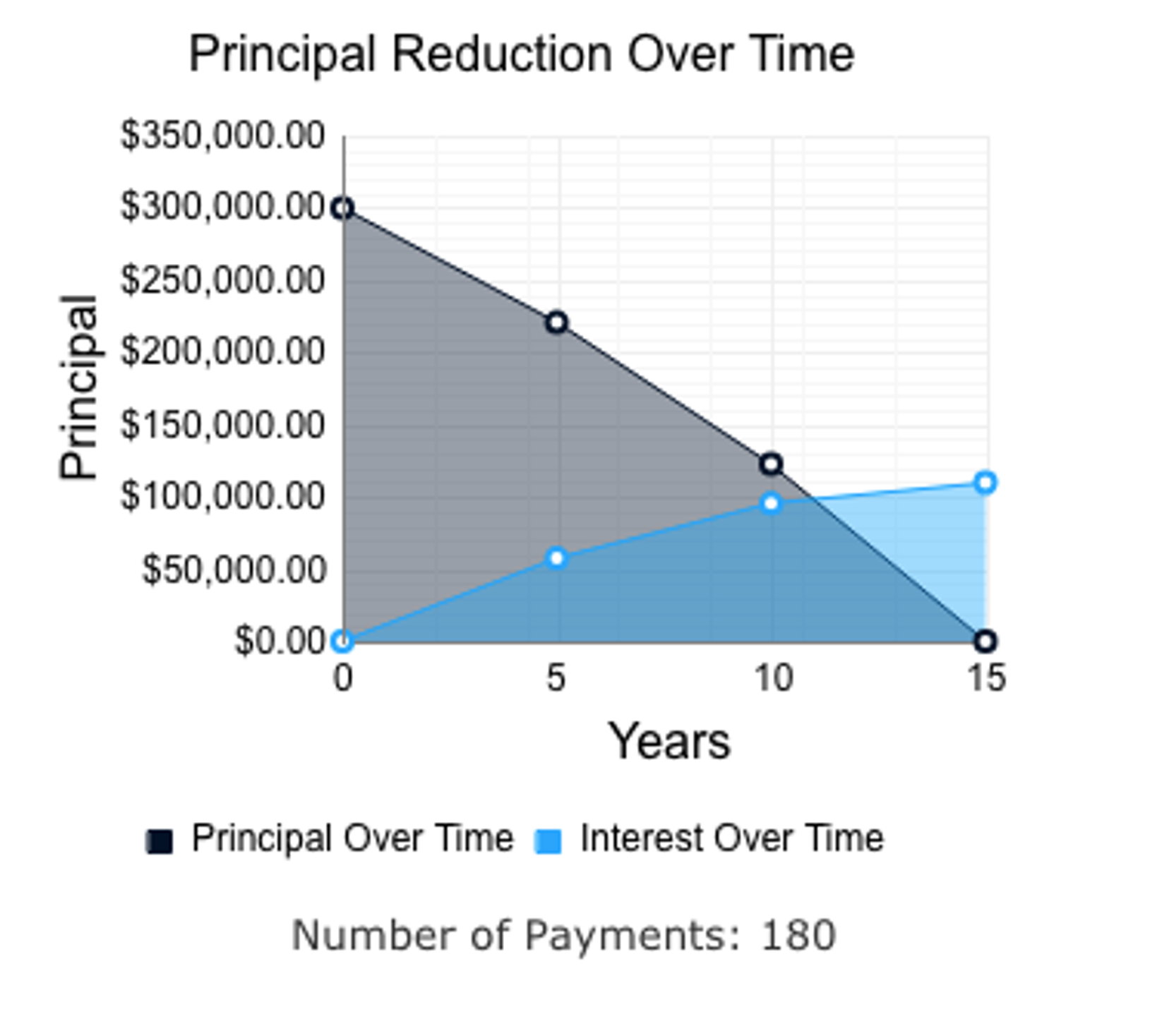

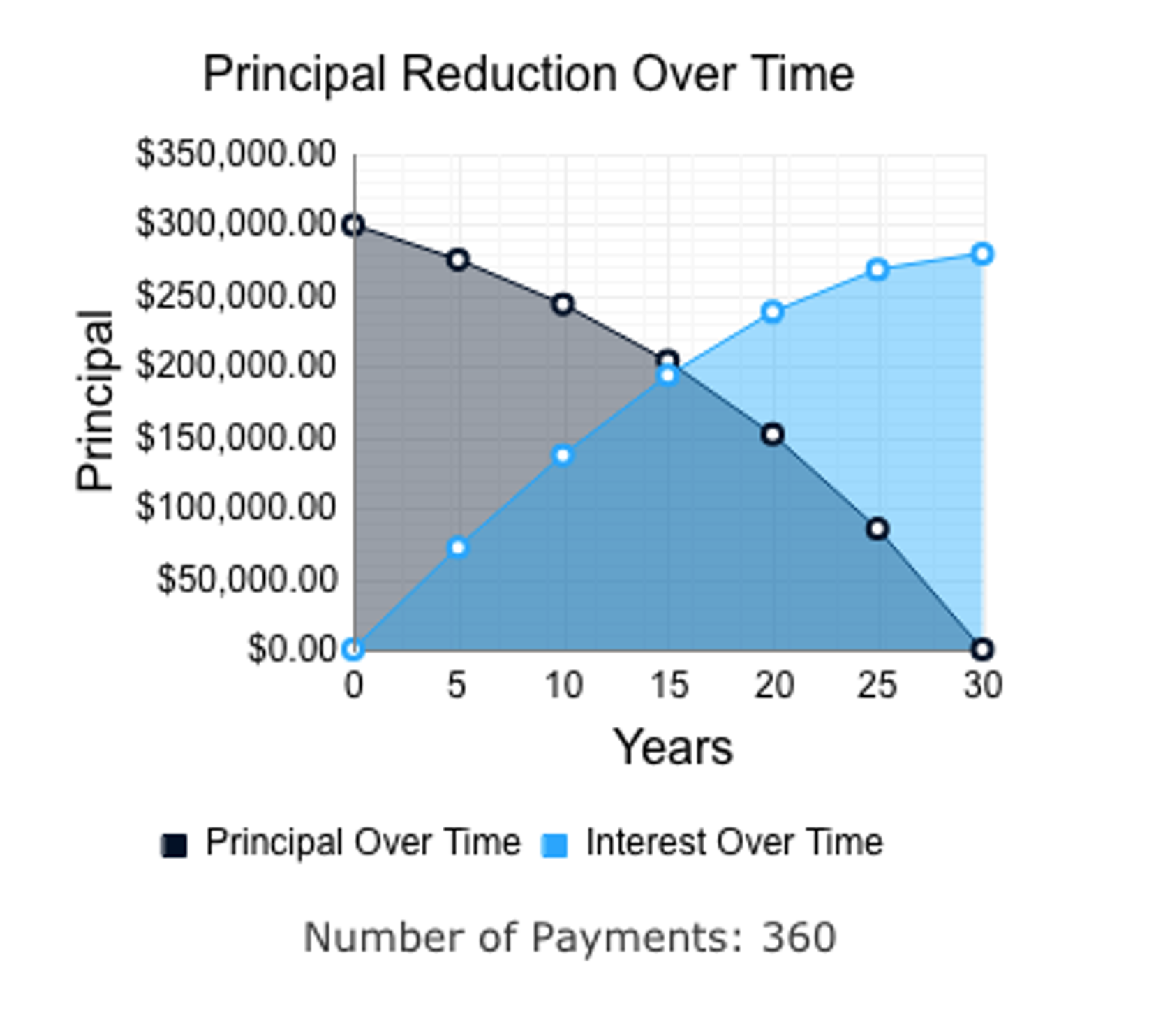

To illustrate, see the figures below which compare amortization schedules using our example from Figure A:

Figure B: 15-Year Amortization at 4.375%

Figure C: 30-Year Amortization at 5%

The black line in these figures shows the amount you would still owe on your home, you’ll notice in both cases principal balance decreases at a faster rate as time goes on. Thus, when although you might make it halfway through your loan’s term, you will not, at this point, have paid your home halfway off. You’ll also notice, by comparing the two, this disadvantage is much more pronounced on a 30-year.

3. Savings will Outweigh ROI on Other Investments

“Savvy” borrowers often argue that it is better to seek a lower payment by choosing a 30-year fixed and contributing the difference to an investment account. In essence, they argue that you can offset the higher interest payments on a 30-year with a greater return on other investments. However, all things equal, this may not be as savvy as one might think.

Staying consistent with our example from Figure A, the difference in your monthly payment (P&I) on a 15 vs a 30-year is $666/month (just a coincidence). If you opt for a 30-year and invest the difference in a diversified portfolio gaining a healthy return of 6% per year, you will end up with $197,000 in assets after 15 years (before capital gains tax). Not bad, right?

Well, let’s take it one step further...

In the previous example, you will have built $103,000 in equity (Down payment & appreciation aside). Add that to the $197,000 you have built-in miscellaneous assets and you get $300,000 in total assets. On a 15-year, with the same monthly contribution and in the same period of time, you will have built $300,000 in equity, accruing $0 in miscellaneous assets for a total of $300,000.

That’s the exact same amount.

Now, consider all the risks you would undertake in the market, consider that regular/ non-mandatory deposits require a great deal of discipline, and, most importantly, consider that you’ll have to pay capital gains on the investment income before you can use it. Not so Savvy anymore, is it?

30-Year Fixed

It is often said that the 30-year fixed is the most expensive mortgage on the market, but is this always the case? If so, then why is the 30-year far and away from the most popular loan?

The answer is yes, the 30-year fixed (in a vacuum), is the most expensive conventional mortgage you can obtain. But that does not mean that it doesn’t have its merits.

Strengths

1.Lower Monthly Payment

If the mortgage rates on a 30-year fixed are at 5%, your principal and interest (P&I) payment equals $1,610 per month, while on a 15-year at 4.375, you’d be at $2,276. As stated before, that’s a difference of $666 every month (30% lower payment) in this case. The added investment may make a difference in your overall wealth over time but most of us are more worried about what we’re going to feed our kids tonight, or whether we can afford those tickets to Cabo this year, and simply can’t afford to look that far down the road.

After all, $666 dollars can handle a pretty hefty car payment, student loans, etc.

2. Lenient Qualification Requirements

Although I’d love to say that we should all seek a home well within our budget and choose a mortgage that puts us in the best financial position over the long term, I realize that in most cases this is not realistic. Sometimes it is simply more important that our home is in the right school district for our kids, that we have enough space for everyone to get along peacefully, or that we have a two-car garage so that extra car doesn’t become a rusted tin can. We just don’t always have the qualifications to seek everything we need in a new home while opting for a larger payment at the same time.

Because your monthly payment is lower, you will qualify for a more expensive home. Loan officers determine the loan amount you will qualify for based on your income compared to your expenses debt-to-income ratio/ DTI. Since smaller monthly payments decrease your DTI you will qualify for a larger loan if you opt for a 30-year.

3. Flexibility

Something to remember about 15-year loans is, although you are saving a boatload over the life of the loan, this is only because you are making a larger commitment. You are essentially promising your lender a significantly larger portion of your income in exchange for better loan terms. That means if you decide to take a fancy vacation, buy a nicer car, or you lose your income for any reason, what is now a manageable payment may turn into a behemoth expense.

The only way to ease matters will be to refinance or, heaven forbid, default.

If you decide to choose 30-year mortgage rates over a 15 on the same-priced home (and same loan amount), you will have more flexibility to use your income elsewhere. Furthermore, most loans these days allow borrowers to prepay; thus, you have the flexibility of a lower monthly commitment, while retaining your ability to pay off your mortgage early, lowering the total interest you will pay.

The Verdict

If my bias isn’t abundantly clear, I feel that the 15-year fixed is the financially responsible choice for most people, including the savvy investor.

Many argue that choosing a 30-year fixed and investing the monthly reminder that you would have otherwise paid on a 15 year will yield you more than if you pay off your home in 15 years and invest that same payment over the remaining 15. The truth is they are right but only if your investments yield an average of nearly 10% for the entire period. If that’s the case, you should start a hedge fund because you are clearly quite good at this whole “investing” thing.

For those of us who are not savants, not robots, and not stonelike in down markets the 15-year fixed is here to keep us honest, remove temptation, and set us on a faster path to financial independence.

Frequently Asked Questions

How do I get pre-approved?

First, you need to fill out an application and submit it to the lender of your choice. For the application you need 2 previous years of tax returns including your W-2’s, your pay stub for past month, 2 months worth of bank statements and the lender will run your credit report. Once the application is submitted and processed it takes anywhere from 2-7 days to be approved or denied. Check out our top lenders and lock in your rate today!

How much interest will I pay?

Interest that you will pay is based on the interest rate that you received at the time of loan origination, how much you borrowed and the term of the loan. If you borrow $208,800 at 3.62% then over the course of a 30-year loan you will pay $133,793.14 in interest, assuming you make the monthly payment of $951.65. For a purchase mortgage rate get a quote here. If you are looking to refinance you can get started quickly here.

How much should I save for a down payment?

Most lenders will recommend that you save at least 20% of the cost of the home for a down payment. It is wise to save at least 20% because the more you put down, the lower your monthly payment will be and ultimately you will save on interest costs as well. In the event that you are unable to save 20% there are several home buyer programs and assistance, especially for first time buyers. Check out the lenders that specialize in making the home buying experience a breeze.