Tax-loss harvesting, also sometimes known as tax-loss selling, is a potentially beneficial tax strategy that lets investors sell an investment at a loss to claim a tax credit against the realized profits from other investments. Using this plan of action can make a lot of sense for tax-savvy investors.

Tax-loss harvesting can be done at any time, although most investors hold off until just before the tax year ends so they can assess their portfolio’s annual performance and how it will affect their taxes.

Read on to find out more about tax loss harvesting, how it works, when is the best time to use it and whether it might benefit your investment portfolio.

What is Tax Loss Harvesting?

Briefly put, tax-loss harvesting is a tax strategy that involves the selling of an asset or security at a loss during a specific time frame that provides a capital gains tax advantage that can reduce your overall tax liability. This loss sale is usually done to offset the quantity of capital gains taxes due as a result of the profitable sale of other assets or securities.

It may help you to know what capital gains are to understand tax loss harvesting better. According to the IRS, “You have a capital gain if you sell the asset for more than your adjusted basis. You have a capital loss if you sell the asset for less than your adjusted basis.”

Even investors who do not presently have capital gains can benefit from harvesting their capital gains losses in a timely manner because they can help offset income or future capital gains. Furthermore, those who have more capital losses than gains on their investments might be able to use up to $3,000 of those losses to reduce their ordinary income in the present tax year, and they can also carry over the balance to use as a deduction in future tax years.

Once the intended loss has been taken, an investor can use the proceeds to buy a similar asset or security to keep their portfolio's overall balance stable. Nevertheless, the investor needs to avoid violating the IRS’s “wash sale” rule, so they cannot repurchase a “substantially identical” asset within 30 days of the loss sale. Doing so invalidates the tax loss write-off.

Note that the IRS defines a "substantially identical security" as one issued by the same company. They can include shares of different classes, a convertible bond issued by the same company, or a derivative contract with the same security as its underlying asset.

How Much of a Loss Can You Harvest?

According to the IRS’ website, if your capital losses are higher than your capital gains, then the excess loss amount that you can claim to reduce your income in a single year is the lesser of $3,000 (or $1,500 if you are married and filing separately) or your total net loss on line 16 of Form 1040’s Schedule D.

You can claim this excess loss on line 7 of either Form 1040 or Form 1040-SR. If your net capital loss is greater than this limit, you can carry the loss forward to use in later tax years.

Long-Term Versus Short-Term Capital Losses

Capital gains or losses can be short-term or long-term in nature, and short-term and long-term capital gains are taxed at different rates. Although some exceptions do exist, if you hold the asset for more than a year before you sell it, your capital gain or loss is generally long term. If you hold the asset for less than a year, then your capital gain or loss is short term.

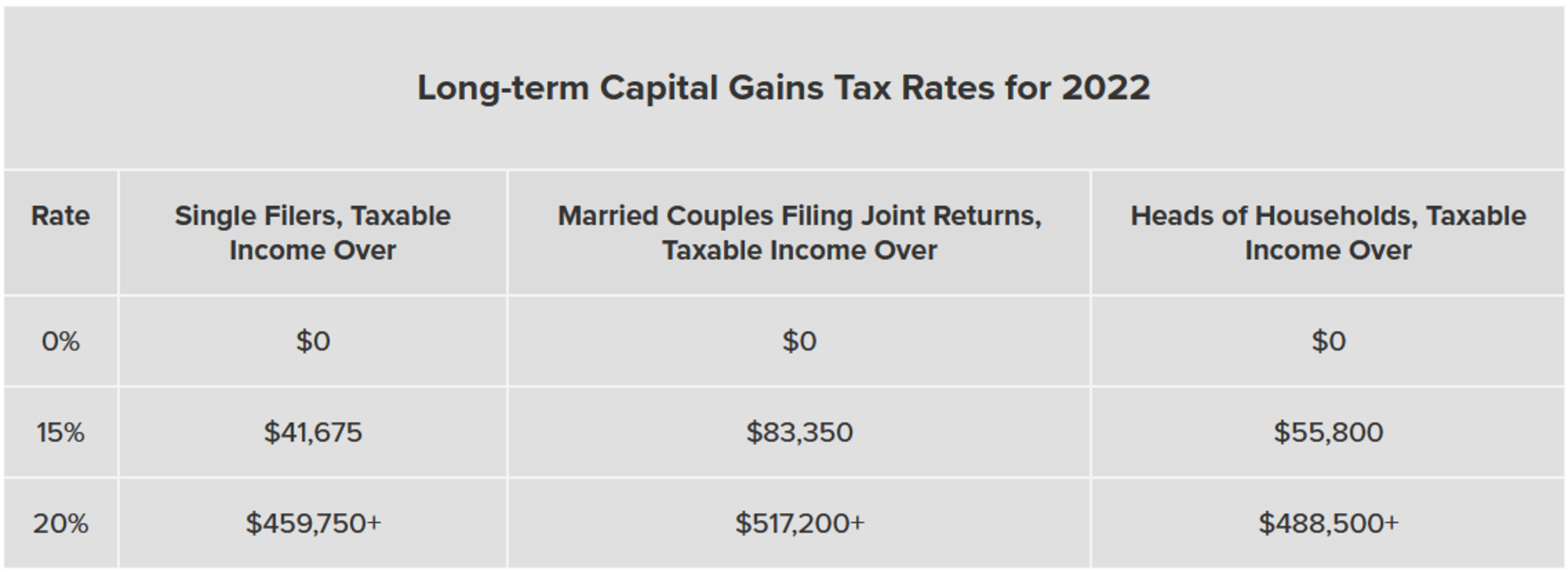

For 2022, the long-term capital gains tax rates appear in the image below. The rate you pay on long-term capital gains will range from 0% to 20% depending on your taxable income and whether you are single, married filing jointly or head of household.

Table of long-term capital gains tax rates for 2022. Source: SmartAsset.

A few exceptions exist where long-term capital gains are taxed at rates greater than 20%. For example, the taxable portion of a profitable sale of Section 1202 qualified stock in a small business stock will be taxed at up to 28%, as are any capital gains from the sale of collectibles like art, antiques or coins. Also, the amount of unrecaptured gain from selling Section 1250 real estate is taxed at up to 25%.

For 2022, the short-term capital gains tax rates appear in the image below. The rate you pay on short-term capital gains will range from 10% to as much as 37% depending on whether you are single, married filing jointly or head of household.

Table of short-term capital gains tax rates for 2022. Source: SmartAsset.

As the above tables illustrate, whether a capital loss is short term or long term matters considerably when using a tax loss harvesting strategy. While tax loss harvesting can be used to offset long-term capital gains, the tax strategy is typically used to reduce taxes resulting from short-term capital gains that incur a higher tax rate than long-term capital gains.

A single taxpayer can deduct up to $3,000 per year of short-term capital losses from their short-term capital gains or up to $3,000 per year of long-term capital losses from long-term capital gains. Long-term capital losses can also be carried forward and spread over future tax years.

Special Considerations for Mutual Fund Investors

Mutual fund investors may get distributions from their fund holdings that can result in short- and long-term capital gains. You will want to take note of the capital gains distribution dates for your larger mutual fund holdings since you may be able to use tax loss harvesting to offset such gains.

Keep in mind that short-term capital gains distributions from mutual funds are considered ordinary income by the IRS that cannot be offset with capital losses, in contrast to short-term capital gains from selling securities held directly.

The Importance of Using the Right Cost Basis Calculation

Those contemplating using a tax loss harvesting strategy should also look at how the cost basis on their investments is computed. Your “cost basis” is the price you paid for an asset including brokerage costs and commissions.

If you have purchased the same security multiple times, perhaps via new purchases or reinvested dividends, you can calculate your cost basis either as an average per share of all purchases (known as the “average-cost method”) or by noting down the actual amount that each purchase of shares cost you (known as the the “actual cost method”).

The actual cost method of cost basis calculation offers a major advantage for tax loss harvesters because it lets you sell higher-cost shares to increase the amount of your realized capital loss.

How Does Tax Loss Harvesting Work?

First of all, if you do not have any losing investments, then you will not be able to do tax loss harvesting. Those who do have losing investments and might stand to benefit from tax loss harvesting will need to make two key decisions to get started. These are:

1. Pick Losing Investments to Sell

Decide which short- and long-term losing investments you want to sell to realize losses that you can use as a tax deduction. Also, you will generally want to deduct short-term losses from short-term gains and long-term losses from long-term gains. You can also roll over excess long-term losses to future years.

2. Pick New Investments to Replace What is Sold

Decide what new investments you would like to purchase, if any, with the proceeds from the losing investments you decided to sell. When planning how to re-invest your money, keep in mind that you cannot purchase a substantially similar investment to the one you sold within 30 days before or after the losing transaction you plan on using as a tax deduction to avoid transgressing the IRS’s wash-sale rule.

If you still like the future prospects of the industry of the losing stock you plan on selling, then you can put the proceeds into an exchange-traded fund or mutual fund that invests in the same industry.

Furthermore, if you get bonuses in the form of stock from your company and those are what you intend to sell, then it would make sense to avoid doing the losing transaction you plan on deducting within 30 days of the bonus stock vesting date or purchase date.

Example

Consider the example of an investor who earns enough income to put themselves into the top short-term capital gains tax bracket of 37%. Based on the 2022 tables above, this would mean they either earned more than $539,900 if they are single or head of household, or more than $647,850 if they are married and filing jointly.

They could substantially reduce their tax liability using tax loss harvesting given the portfolio positions and transactions they made over the past tax year shown in the following table. Note that a realized gain or loss means the position has been closed out, whereas an unrealized gain or loss means the position remains in the portfolio.

| Stock name | Unrealized | Realized | Held for |

| Alpha Company | $100,000 | 500 days | |

| Beta Company | -$50,000 | 650 days | |

| Delta Company | -$70,000 | 100 days | |

| Gamma Company | $250,000 | 400 days | |

| Theta Company | $100,000 | 170 days |

Table of stock positions and transactions in the sample portfolio.

The sale of Gamma Company stock that was held for 400 days involves a long-term capital gain of $250,000 that is taxed at a rate of 20%. The sale of Theta Company stock that was held for only 170 days involves a short-term capital gain of $100,000 that is taxed at a rate of 37%,

Without tax loss harvesting, their tax owed on the sales of the Gamma Company and Theta Company stocks would be:

($250,000 x 20%) + ($100,000 x 37%) = $50,000 + $37,000 = $87,000

If they instead harvested some of their unrealized losses by selling their long-term holdings of Beta Company and their short-term holdings of Delta Company, those losses would help reduce the taxes owed substantially as follows:

($250,000 - $50,000) x 20% + ($100,000 - $70,000) x 37% = $40,000 + $11,100 = $51,100

The tax loss harvesting plan thus saves them the difference of $87,000 and $51,100 or $35,900.

Who Benefits from Tax Loss Harvesting?

As the example shown in the previous section illustrates, tax loss harvesting can be beneficial for those who are facing a substantial capital gains tax liability from the sale of profitable investments, especially if the gains are on short-term investments. While tax loss harvesting generally will not eliminate capital gains taxes completely, it can notably reduce the amount of taxes paid.

Furthermore, an investment loss can be used in two different ways:

- The loss can be used to offset investment gains.

- The loss can offset up to $3,000 of joint income in a single tax year.

Those who find themselves in the higher capital gains tax brackets because of their income and who have also taken a substantial amount of short-term capital gains on their profitable investments will tend to benefit the most from implementing a tax loss harvesting plan.

On the other hand, those who earn less than $41,675 if single, $83,350 if married filing jointly or $55,800 if filing as the head of household and who have only realized long-term capital gains will find themselves in the zero capital gains tax bracket, so they may not be able to benefit from a tax loss harvesting plan in that tax year.

Since unused losses can be carried forward indefinitely, stock market corrections can present a good opportunity for tax loss harvesting. The additional losses can be put into a tax savings account that can offset taxable gains for years to come.

How Does Tax Loss Harvesting Impact Your Portfolio?

The goal of tax loss harvesting is to pay less in taxes so that you have more money to invest in your portfolio, which is generally a good thing to help further your investment goals. Tax loss harvesting can also positively impact your portfolio by giving you a tax benefit for eliminating losing positions you might not want to keep anyway.

By selling losing investments as part of a tax loss harvesting plan and then replacing them with a similar (but not too similar) alternative, you can maintain a comparable investment portfolio while offsetting some of your tax liability resulting from realized investment gains.Taking this action means even a poor investment can do some good for your portfolio by reducing your overall tax burden.

Compare Financial Advisors for Tax Loss Harvesting

Many tax accountants and professional financial advisors working at stockbrokers or independent firms can provide you with useful information on how tax loss harvesting can benefit your tax situation and investment portfolio. To help you get started with tax loss harvesting, Benzinga has compiled the list below of online brokers, stockbrokers with advisors and robo-advisors who offer tax-loss harvesting as part of their core services and can provide expert financial advice on the subject.

- Best For:Quick and Convenient Financial GuidanceVIEW PROS & CONS:securely through Money Pickle's website

- Best For:Comparing AdvisorsVIEW PROS & CONS:securely through SmartAsset Financial Advisors's website

- Best For:High Net Worth IndividualsVIEW PROS & CONS:securely through Empower's website

Frequently Asked Questions

Is tax loss harvesting really worth it?

Tax loss harvesting can be very beneficial in certain circumstances, but any amount you might save on taxes should not detract from your overall investment plan and goals. Be sure to sensibly balance the advantages of tax loss harvesting with the benefits of continuing to hold underwater positions for future gains.

Is tax loss harvesting illegal?

As long as you follow the IRS’ capital gains tax and wash sale guidelines exactly, tax loss harvesting is perfectly legal and may actually be financially advantageous for you.

About Jay and Julie Hawk

About Julie:

Julie Hawk earned her honors undergraduate degree from the University of Michigan before pursuing post-graduate scientific research at Cambridge University. She then started work in the private sector as a business systems analyst for a major investment bank, where she qualified as a Series 7 Registered Representative and received comprehensive training in various financial products. Further honing her skills, she attended the prestigious O’Connell and Piper options training course in Chicago, mastering professional option risk management techniques.

Julie then transitioned into the role of a professional Interbank forex trader, currency derivative risk manager and technical analyst, ascending to the position of vice president over a 12-year career in the financial markets. Julie’s illustrious banking career spanned working for major international banks in New York City, London, and San Francisco, where she served as an Interbank dealer, technical analyst, derivative specialist and risk manager. Her responsibilities included educating, devising customized foreign exchange hedging and risk-taking strategies, and overseeing large-scale transactions for esteemed banking clients, including corporations, fund managers and high-net-worth individuals. As part of her responsibilities, Julie managed substantial portfolios of forex options, spot, and futures positions as a currency options risk manager, earning recognition for executing innovative and highly profitable forex derivative transactions. Julie also spearheaded educational conferences on currency derivatives.

During her banking career, Julie attained world-class expertise in technical analysis, including Elliott Wave Theory, and pioneered research into automated trading and trading signal systems. An active member of the San Francisco Writers’ Guild, Julie also authored trade strategies, educational material, market commentary, newsletters, reports, articles, and press releases. She became a sought-after market expert who was frequently interviewed by financial magazines and news wires such as REUTERS.

Following her retirement from the banking sector, she dedicated 15 years to online forex trading, mentoring and freelance writing for TheFXperts, which she co-founded with her husband Jay. Julie is the co-author of “Forex Trading: A Beginner’s Guide” and “Technical Analysis for Financial Markets Traders,” in addition to five other books on financial markets trading and personal finance. She now focuses on writing articles on financial markets for platforms like Benzinga, although she continues to trade forex online and mentor fellow traders as part of TheFXperts’ financial team.

About Jay:

Jay Hawk grew up in Chicago and Mexico City where he became bilingual in English and Spanish. After taking formal training as a classical guitarist at prestigious music conservatories in Europe, Jay then embarked on a remarkable journey into the financial markets, cultivating his notable expertise through hands-on experience that began on the Midwest Stock Exchange.

His financial career progressed as he started actively participating in various exchange floor trading activities in the Chicago futures and options pits, where he worked his way up the ladder, serving as a clerk, trader, broker, investor and fund manager. Jay then ran a retail stock brokerage desk and managed funds for large institutional investors, leveraging his discretionary trading skills to yield profitable results for clients.

This ultimately led to Jay holding exchange seats and operating as a market maker on options exchanges in Chicago and San Francisco, initially on the Chicago Board Options Exchange. Jay also played a significant role in the Chicago Mercantile Exchange’s evolution, where he contributed to launching and actively trading the first listed currency futures options. After transitioning to the West Coast, Jay then held a seat and ventured into trading stock options and their underlying stocks on the Pacific Options Exchange.

Jay’s comprehensive understanding of fundamental economic and corporate analysis continues to inform his trading and investment activities and has led to his subsequent success as an expert financial writer. Together with his wife Julie, he co-authored “Stock Trading: A Beginner’s Guide”, “Commodity Trading: A Beginner’s Guide” and “Fundamental Analysis for Financial Markets Traders,” among their published books focusing on financial markets trading, market analysis, and personal finance.

As an integral member of TheFXperts’ team, Jay now excels in trading forex online for his personal account, mentoring aspiring traders and writing for financial platforms like Benzinga where he specializes in covering topics related to the stock and commodity markets, as well as investing, trading and reviewing online brokers.