Looking for the best rate and coverage for life insurance? Consider Sproutt.

Is life insurance worth it? It may not seem like it -- until it's too late. Contemplating what will happen after your own death may seem morbid, but consider what it can do for your loved ones. Have you prepared for their financial security when you pass? It’s doubly important if you have young children and/or family members (such as a spouse or aging parents) who financially depend on you.

Life insurance could be the answer. But like all other financial decisions, you need to understand whether you need it, what you’re buying and assess whether it makes sense for your specific situation.

How to Determine if Life Insurance is Worth It

Follow these steps to figure out if life insurance is right for you.

- Consider the type of coverage you may need.

- Think about your budget and what you can afford to pay per month. Does this limit what type of coverage is available to you?

- Consider your unique situation, including who depends on your income, what you can reasonably afford, your health, lifestyle, occupation and more.

Once you've answered these questions, you can compare plans from trusted providers to find one that makes sense for you.

Step 1: Consider the Type of Coverage You May Need

You’ll need to buy a life insurance policy that meets your needs. Before you do that, understand the types of coverage offered by life insurance companies. Coverage needs and the types of insurance products to meet those needs might differ for individuals, depending on several factors:

- Age

- Income

- State of your health

- Family status (single, married, with or without children)

- The number of people financially dependent on you

- The amount of income that the coverage must replace

At a very high level, there are two types of life insurance. There’s term life coverage, in which you pay premiums to an insurer for a set (5-, 15- or 20-year) term, which comes with a death benefit. If you die during the term, the insurer pays the death benefit to your beneficiaries. Term life comes with no surrender value or payouts when you’re still alive. Outliving the term or canceling the policy during the term yields you no benefits or refunds.

Permanent life coverage does have the ability to pay the policyholder during his or her lifetime. Different types of permanent life policies offer varying degrees of coverage, which include whole life, variable life, universal life and variable universal life coverage.

These types of policies usually have what’s called a cash value, or a component of the premiums paid by you that are set aside (and invested) by the insurance company.

Once the policyholder dies, beneficiaries receive the death benefit. These policies may also offer other options, such as the ability to borrow money against the cash value, use the cash value to pay premiums or withdraw the accumulated cash value entirely by surrendering the policy.

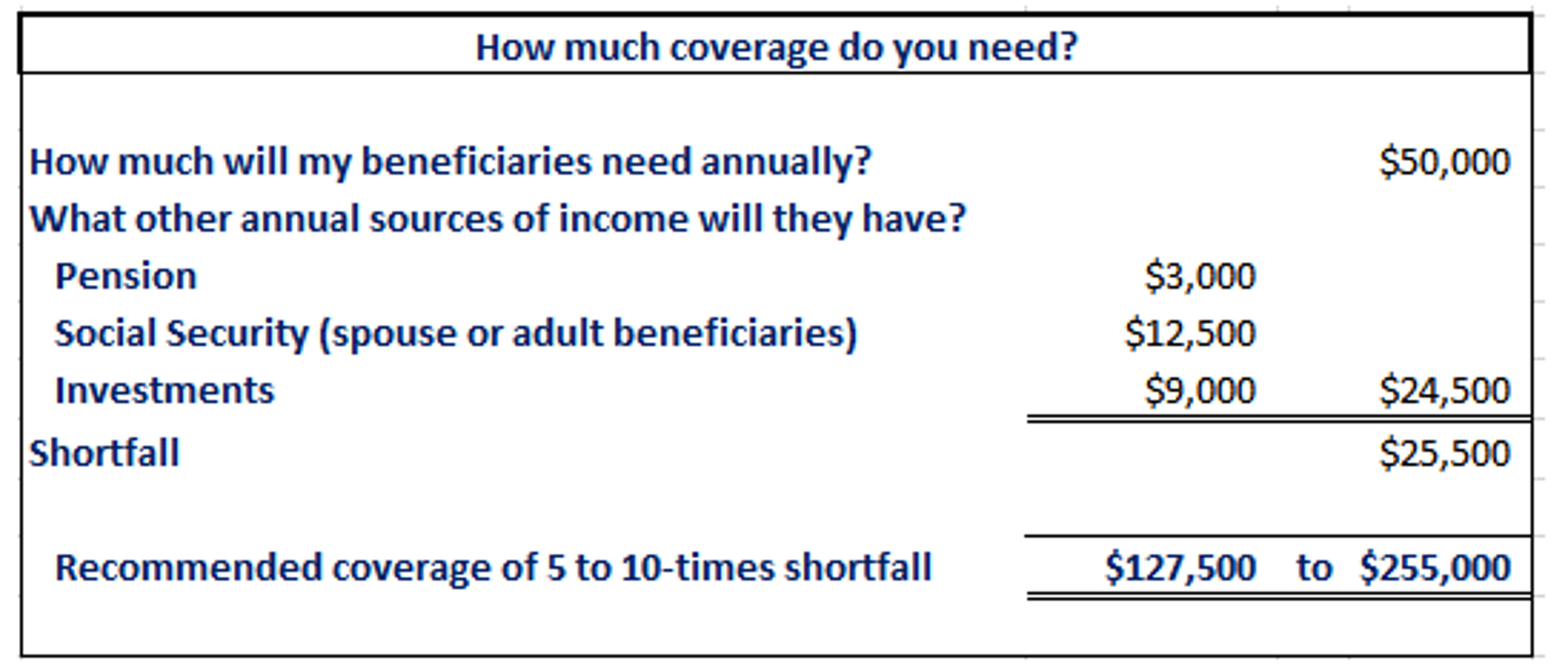

A general rule of thumb to determine the amount of coverage you need is to assume 5 to 10 times your annual income.

Figure out what your beneficiaries need annually to meet their financial needs. From that amount, subtract other financial resources they’ll have available to them upon your passing. The result is the income shortfall you’ll need to plug through life insurance.

Use 5 to 10 times that amount to determine your coverage needs. Consider the type of coverage you’ll receive and other features of the policy that might fit your needs.

Step 2: Think About Your Budget

Life insurance policies come with a cost, measured in the form of monthly or annual premiums that you pay for the coverage you receive. Before you buy a policy, ensure that you can afford to make those regular premium payments.

A good first step in budgeting for life insurance is to take stock of your current stage in life and assess:

- Who your beneficiaries are and what their financial needs might be in the future.

- The assets you might accumulate over the life of the insurance term.

- Your current and future expenses (including buying a home or putting the kids through college) and whether your savings and investments will be enough to meet those needs.

- The likelihood that you’ll need money to fund plans for your future, such as starting a business or retiring early.

- Any existing insurance coverage you might have and the type of coverage it provides.

You could also use commercially available insurance needs estimators to help you address some of these questions. It may also help to learn more about policy payouts at different ages.

Based on those findings, you can plan for the specific type of insurance policy you can afford and how to pay for it.

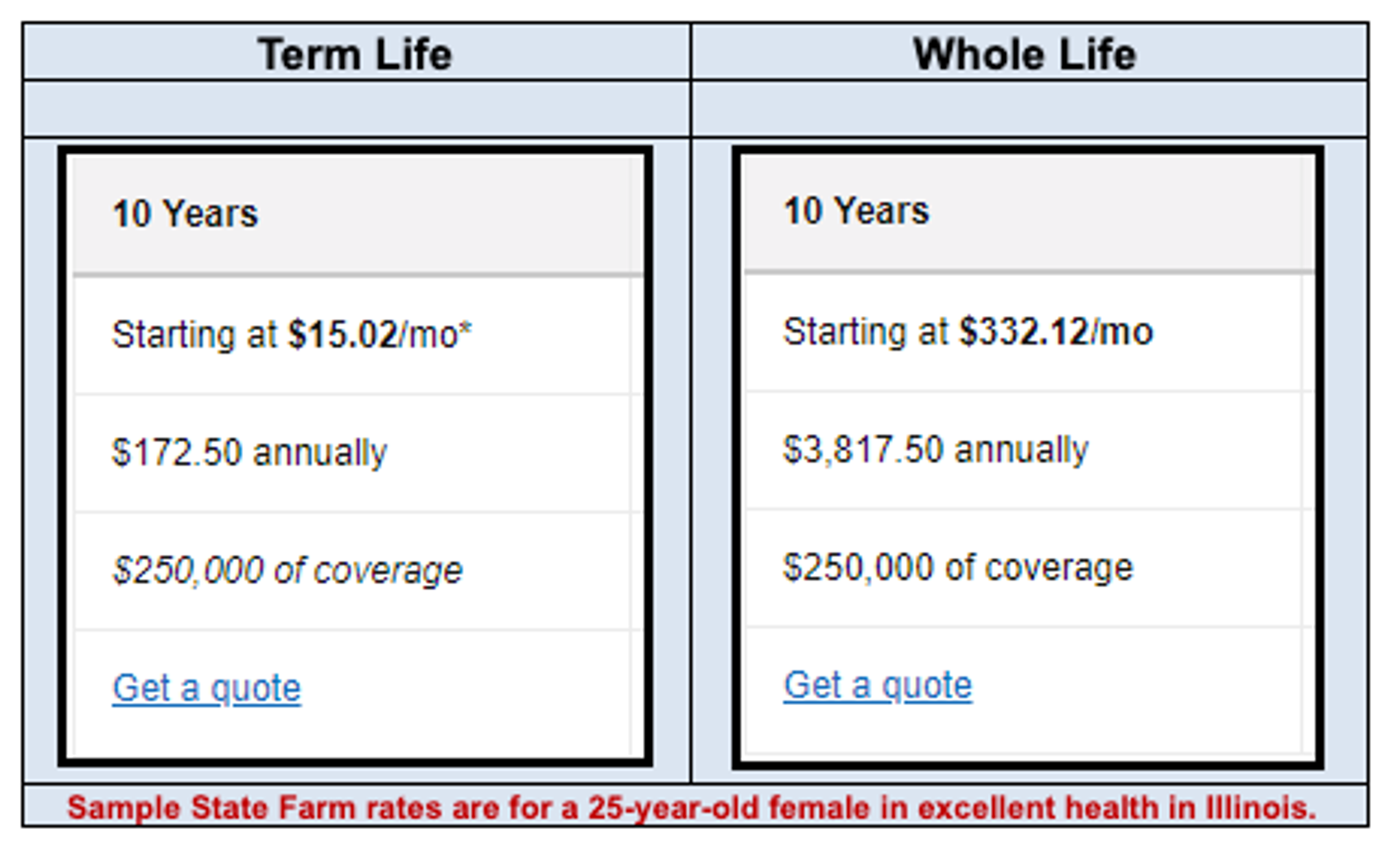

Some of the best life insurance companies offer products with different cost structures. As indicated by the sample quotes here, whole-life policies are typically more expensive — sometimes by a factor of 15 or 20 times — compared to equivalent coverage-providing term life policies of the same duration. Permanent life policies could potentially offer periodic dividends which may offset some of the budgeted costs of your premiums.

Consider what you might do with your policy if you lose your job or are temporarily unable to earn an income. Can you continue to pay your premiums or is that money better spent addressing household needs instead?

Do the math and set aside the required monthly premiums when planning your household budget, just as you would for your mortgage, rent or groceries.

To get an estimate of monthly premiums, you can get a quote here.

Step 3: Determine If It’s Worth It for Your Unique Situation

Life insurance does offer certain benefits but it might not necessarily be worth the cost in your particular situation.

When It’s Worth It

You may want to buy life insurance if:

- You aren’t confident that your investments and savings will be enough to support your loved ones when you die.

- Your employer-provided life insurance coverage isn’t enough for your needs, and you need to supplement it with additional insurance.

- The environment in which you live or work poses a significant risk to your well-being. For example, you might live in a conflict zone or work in a high-risk profession -- if this is the case, look into a standalone or add-on accidental death insurance plan.

Life insurance could also be a way for high-net-worth individuals to strategically plan to leave a tax-free legacy to their beneficiaries. It can also be a great succession plan or estate transfer mechanism for business owners and entrepreneurs.

Some permanent life insurance policies can also help pay for medical expenses if you opt for specific policy riders. Is permanent life insurance worth it? It's a possibility if you believe your spouse’s long-term care or chronic illness-related medical bills will be insurmountable in the future.

When It’s Not Worth It

Some circumstances where life insurance may not be worth it include:

- When you are relatively young, in prime health and have no dependents or a spouse.

- When you’ve already got other safety nets in place for your loved ones, such as sizable investments or a great employer-sponsored pension plan.

- Some smokers, those with other substance dependencies or chronic health conditions might find it too expensive (or not at all cost-effective) to acquire a life insurance policy.

- You don’t need to cover a mortgage or dependents, or other financial obligations are no longer a concern. For example, if your kids are out of the house and your home is fully paid off, you may not need life insurance.

A life insurance policy could cost you way more in premiums than the income you plan to replace by purchasing it, so it might also not be worth acquiring.

Some people believe that it is a good idea to buy life insurance for a child or a parent. That might not be such a great idea if income replacement and/or the welfare of those left behind is a primary motivation for buying life insurance. Young children and aging parents are not likely to earn the income to justify the cost of the premiums. Anyone insured at that stage in life is unlikely to have beneficiaries who financially depend on them.

Find the Best Coverage for You

Finding the right life insurance product for you and/or your family really depends on your needs. A term life policy is a great option if you expect significant life events to occur within the course of the term.

In some situations, the best coverage strategy might be to purchase multiple term life products of varying terms. You then allow each policy to lapse when they’re no longer needed.

Buying permanent life insurance might be the right fit due to the investment component attached to the policy. Universal life, whole life and variable life insurance policies are good examples. Insurance companies invest a component of the premiums paid, which then grows until the payout. If emergency access to funds is a priority, these policies sometimes also allow policyholders to tap into the accumulated balance of the invested component.

Look for other features offered by various types of coverage before deciding what’s right for you. Some term life policies are convertible to whole life policies, which could be attractive.

Pacific Life is also one of the most affordable life insurance providers for smokers. While smokers looking for a policy with Transamerica may pay as much as $50 a month for their coverage, plans for tobacco users are available from Pacific Life for as little as $17 a month. If you aren’t quite ready or able to quit, Pacific Life might have the key to affordable insurance.

Best Life Insurance Companies

Protecting your family doesn’t have to be expensive. It’s never been easier to get a cheap life insurance policy for just a few dollars a month. Start your search with our favorite low-cost life insurance policy providers.

1. Life Insurance by Bestow

With plans starting at just $8 a month Bestow is perfect for anyone on a budget. This affordable term life insurance allows you to skip the doctor's appointment and say “no thanks” to the stacks of paperwork. You can get a quote quickly and when it’s convenient for you because everything is 100% online. Answer a few simple questions and get a decision instantly.

There is no need to enter your name, email or phone number to get a quote. Bestow relies on data rather than feedback from a medical exam. Take life into your own hands by applying with Bestow, the ideal combination of age-old quality fused with modern technology to deliver one of the best companies on the market.

10 and 20-year policies are available, just another reason why this customizable life insurance makes our top list.

- Best For:Term life insuranceVIEW PROS & CONS:securely through Bestow Life Insurance's website

2. Haven Life

Haven Life is an innovative life insurance agency that offers a simple way to obtain term life insurance for those between the ages of 18 and 64. You can choose a term length of 10, 15, 20 or 30 years. What’s unique about this term life insurance is the way you can complete an application online and, if approved, digitally purchase coverage.

Haven Life is backed and wholly owned by MassMutual, a nearly 170-year-old life insurance company with a long history of claims-paying ability. Also available is Haven Life Plus, a no-cost rider to the Haven Term policy for customers in eligible states. Some of the great services included with Haven Life Plus are:

- A world-class fitness app with thousands of workouts and (most importantly) great music

- An app that combines the latest sleep and neuroscience research to help prevent jet lag

- A customized, state-specific, legally valid online will

Affordable and dependable, Haven Life offers protection for your family in the event of an unfortunate loss. A 20-year, $500,000 Haven Term policy, issued by MassMutual, for a healthy 35-year-old woman, is $23.34 per month. For perspective, the average American adult spends around $50 every month on subscription services. Apply for Haven Life to help financially protect your loved ones.

3. Ladder

Ladder term life insurance is available to those between 20 and 60 years old. Ladder doesn’t provide any permanent life insurance policy but its term life insurance is a good fit for most situations. The general philosophy is to buy term, invest the rest.

Ladder allows you to purchase a term life insurance policy without a medical exam for coverage up to $3M.

Ladder is unique because it lets you change your coverage along the way. It provides Ladder Up and Ladder Down options so you don’t need to cancel your existing policy to adjust coverage.

Apply to increase your policy’s face value with Ladder Up. Your additional coverage is priced separately, and your premium is adjusted based on the new changes. Use Ladder Down to decrease your coverage amount and your premium will decrease proportionally.

You have the option to choose a term length of 10, 15, 20, 25 or 30 years. Coverage ranges from $100,000 to $8 million.

There are restrictions related to the term length based on your age. Your current age plus the term length shouldn’t exceed 70 years.

- Best For:Adjustable coverageVIEW PROS & CONS:securely through Ladder Life Insurance's website

Looking Beyond Death Benefits

Is life insurance worth it? Life insurance can deliver much more than death benefits to your beneficiaries. It can serve as an invaluable component of an overall financial plan. Life insurance delivers peace of mind, but also consider that your needs change with time. Ensure you always have the right coverage by reassessing your life insurance needs periodically.

What's the difference between term life insurance and whole life?

Term life insurance only lasts for a predetermined term, but whole life insurance lasts as long as you pay the premiums.

Can a life insurance policy help pay for my funeral?

Yes, a life insurance policy can help your loved ones pay for you burial and funeral expenses.

Do life insurance policies have a cash value?

Some life insurance policies do build a cash value, but it can take years to accumulate enough money to make it substantial.

Methodology

Benzinga crafted a specific methodology to rank life insurance. To see a comprehensive breakdown of our methodology, please visit our Life Insurance Methodology page.

About Sarah Horvath

Sarah Horvath is a highly respected freelance senior copywriter specializing in insurance content. With a wealth of experience, she is recognized as one of the top insurance copywriters in the industry. Sarah’s expertise encompasses various aspects of insurance, including home warranties, life insurance, health insurance, and more. Her insightful articles and guides are regularly featured on major finance sites, providing invaluable information to readers seeking to navigate the complexities of insurance policies. Known for her clear, concise writing style and comprehensive understanding of insurance products, Sarah is dedicated to empowering individuals with the knowledge they need to make informed decisions about their insurance coverage.