If you rent a home or apartment, you’ve probably dreamed about one day ditching your rental bill and investing in a home of your own. Investing in property has long been a part of the American Dream, but the seemingly insurmountable down payment obstacle stops most would-be homeowners right in their tracks.

If you’ve considered purchasing a home but you’re having trouble gathering the funds, follow our step-by-step guide.

Saving for a Down Payment and Closing Costs

There are usually two major costs associated with buying a home: the down payment and closing costs. Your down payment is an upfront cost that you’ll put down on a mortgage. You need a down payment when buying a home to assure your lender that you’ll be able to make payments on your mortgage and to lessen the burden of debt on yourself.

Though you’re not legally required to put a down payment on your home, most lenders require that mortgage applicants have between 10 and 20 percent of their mortgage ready as a down payment before they approve the remainder of the loan amount.

If you are able to put a larger percentage down, you will enjoy lower monthly payments and possibly a lower interest rate. Closing costs are expenses you’ll pay when finalizing your home’s purchase. Closing costs may go to your mortgage provider, your real estate agent or the person or family you’re buying the home from. Some of the most common closing costs you’ll see include:

- Application fees. Your mortgage lender may request a fee to process your application. Not all lenders charge an application fee and some application fees can often be negotiated.

- Credit check fees. If your mortgage lender does not charge an application fee, you may be asked to pay for a credit check. Credit checks allow lenders to view your credit report and score, both of which play a significant role in determining your mortgage interest rate.

- Closing fees or escrow fees. Some states require that an attorney be present at every home’s closing. Closing fees cover the cost of a real estate attorney to finalize your transfer.

- Pest inspection fees. Pest inspection fees cover the cost of hiring an exterminator or state inspector to ensure that the property is free from termites, dry rot and other types of parasite-related damage. Some states require that a pest inspection must be completed before the transfer of the deed to the home.

- Appraisal fees. In some states, you will be required to pay for an independent appraisal of value before buying a home. This appraisal is then submitted to the state and determines how much property tax you’ll pay.

- Transfer taxes. Transfer taxes are taxes that are paid when the seller passes the title to the buyer.

The specific closing costs you’ll incur depend on the state you’re buying the home from and the specific agents and lenders you work with. You may see some or all of the fees listed above, or you may see additional fees if your state requires different types of transfers or inspections. Consult with a local real estate agent to learn more about closing costs common in your area.

The True Costs of Owning a Home

Many would-be home buyers make the mistake of underestimating the true cost of home ownership. It’s easy to believe that owning a home is a better deal than renting—after all, if the cost of your mortgage is less than the cost of rent and utilities, it’s always a better deal to buy the home, right?

Unfortunately, there are a number of “hidden” costs of home ownership that can actually make renting less expensive in some cases. Some of the most common costs associated with buying a home as opposed to renting include:

Interior Repairs

When you’re renting an apartment, your landlord is responsible for taking care of anything that goes wrong with the amenities in your home. When you own a home, there’s no one to call when something breaks, which means that if your heating system breaks down or a toilet overflows, you’ll need to have an emergency fund to cover the bill.

Exterior Repair and Maintenance

If you live in a condominium or an apartment, your landlord or homeowner’s association is responsible for managing the outside of the property and keeping it clean and safe. After you purchase your home, you are responsible for maintaining your lawn and handling potentially costly repairs and renovations, like damage to the roof or pest infections.

Utilities

If you live in an apartment, you probably have to pay at least a portion of your utility costs. However, when you own your home, you’re responsible for the cost of all utilities you use, including water, electricity, gas, heating, garbage removal and more.

Property Insurance

Though property insurance is not explicitly required by law, it’s strongly suggested that you maintain at least a bit of insurance to protect yourself against damage. Otherwise, a single natural disaster can completely wipe out your property or make it totally unlivable — and leave you with the bill.

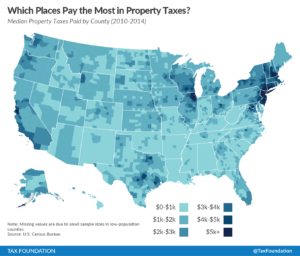

Property Taxes

Property taxes vary wildly from state to state and from city to city. The property taxes that you’ll pay are based on your home’s assessed value, which may be completely different from the housing market value. The average homeowner pays about $3,296 in annual property taxes.

However, you’ll need to consider your specific state and county when determining your individual property taxes; you may end up paying over $8,000 annually if you purchase a home in New Jersey or you may pay as little as $2,400 if your home is in Hawaii. As you can see, the cost of owning a home includes much more than just your monthly mortgage and down payment.

All of these costs are in addition to the down payment and closing costs when you seal the deal. These expenses are one of the reasons why you should be extremely conservative when it comes to deciding how much house you can afford.

How to Save for a House

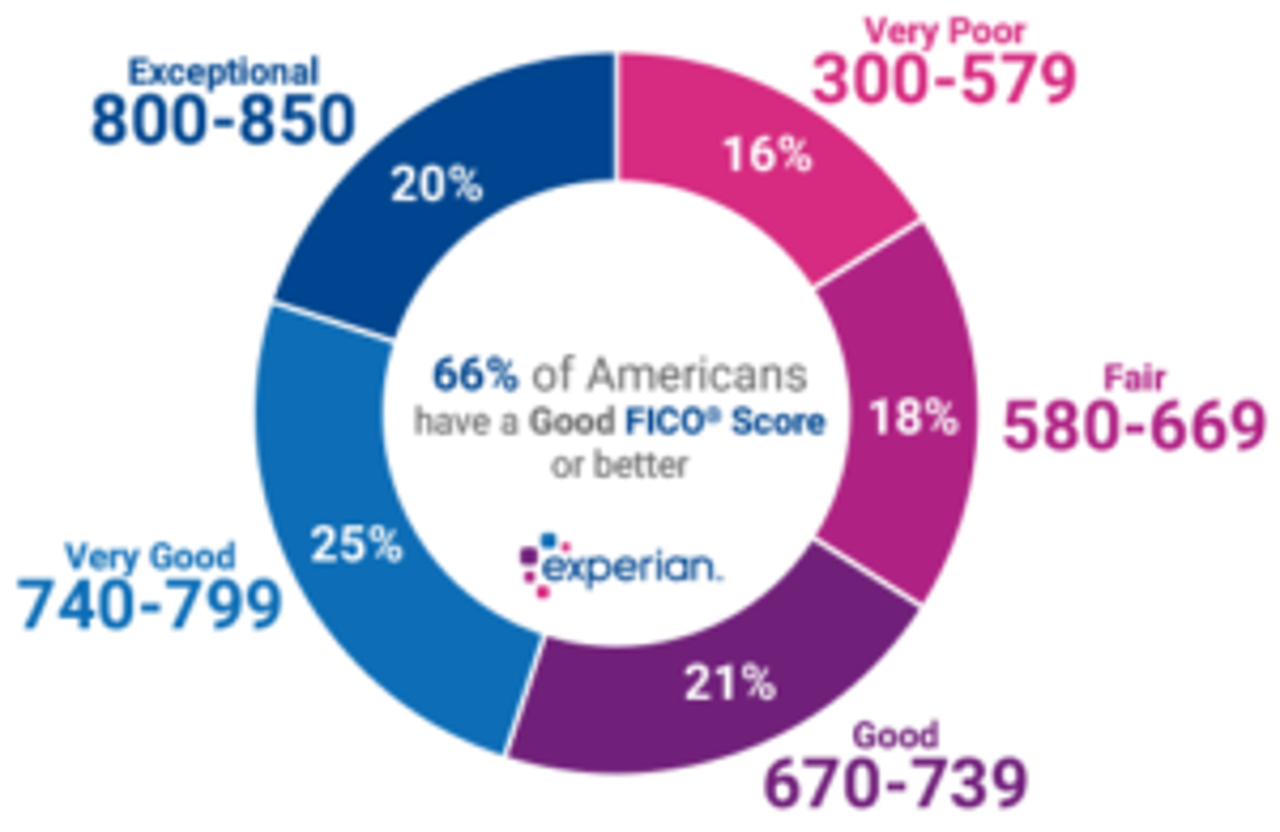

Step 1: Improve Your Credit Score.

If you have bad credit or no credit, take steps to improve your score before you think about buying a home. Maintaining a good or excellent credit score of at least 670 points tells lenders that you’re a responsible spender and you’re likely to make your mortgage payments on time.

Mortgage lenders are more likely to be lenient about down payments with borrowers who have a high credit score, and a good or excellent score can even qualify you for lower interest rates. Make your credit card payments on time, keep a low revolving balance on your accounts, and simply wait until your credit account ages. All can help you improve your score over time.

Step 2: Pay Down Outstanding Debt.

Saving money for a down payment will be more difficult if you also pay down debt every month. Though it may sound counterintuitive, paying off debt before you start to save for a down payment can actually help you save more by reducing what you owe in interest over time.

If you have student loan debt, an auto loan or outstanding credit card debt, create a plan to pay down your debt before you start saving for a down payment. You may want to use a budgeting app to save more money and schedule monthly payments — this will help you avoid accumulating interest because you forgot when your payment was due.

Step 3: Determine How Much Home You Can Afford.

Once you’ve begun to save up a down payment, look at homes within your price range. Your location, debt and your income will determine how “much home” you can afford and how much you can reasonably take on in monthly mortgage payments. Your estimated housing payment should never take up more than 36 percent of your monthly budget.

To determine how much home you can afford, first calculate how much income your household has every month. If you are a salaried employee, you probably already know how much income you can expect every month after taxes. If you are an hourly employee or an independent contractor, open up your bank statements from the last three months and find an average monthly income.

Multiply your monthly income after debt payments by 0.30 to get a conservative estimate of how much you can afford to take on in a monthly mortgage payment, assuming that six percent of your income will go towards utilities, property taxes, and household maintenance. As an example, let’s say that you earn about $4,000 per month after taxes. Let’s also say that you must make a minimum credit card payment of $100 per month and a student loan payment of $300.

To calculate how much home you can afford, you would subtract $400 (your student loan dues plus your credit card payments) from $4,000 ($3,600) and multiply the result by 0.30, or 30 percent. In this example, you would be able to comfortably afford a monthly mortgage payment of around $1,080. Be aware that you may need to slightly adjust this number depending on your county’s property tax rate.

Step 4: Take a Look at Your Household Budget.

Once you’ve calculated how much home you can afford, you can figure out a savings goal to set for your down payment! If you haven’t already begun saving, you may need to analyze your household budget and look for places to cut back. Work together with the members of your household to prioritize saving. Add a goal board to your refrigerator to keep your eyes on the prize of your eventual home.

Final Thoughts

The best way to save money quickly is to prioritize saving as soon as you get your paycheck. Most Americans make the mistake of spending their check first then saving what (if anything) is left over at the end of the month. Instead, pay yourself first by saving a percentage of your income as soon as your direct deposit hits.

You may even want to consider opening a separate savings account to transfer your money to remove the temptation to dip into your funds and help you manage your budget.

Want to learn more? Check out Benzinga's guide to if you should pay down your mortgage or invest, the best budgeting apps and the best budget spreadsheets.

Frequently Asked Questions

What is the fastest way to save money for a house?

The fastest way to save money for a house is to create a budget and stick to it. By carefully tracking your expenses, cutting unnecessary costs, and saving a significant portion of your income each month, you can accumulate funds more quickly. Additionally, you can consider taking on additional sources of income, such as a side hustle or part-time job, to supplement your savings. It is also advisable to explore options like reducing debt, optimizing investments, and prioritizing your savings goals to accelerate your progress towards buying a house.

How much do you need to save to afford a house?

The amount you need to save to afford a house depends on various factors such as the location, size, and condition of the house, as well as your personal financial situation. It is generally recommended to have a down payment of at least 20% of the purchase price, as this can help you avoid private mortgage insurance. Additionally, you should consider other costs such as closing costs, moving expenses, and potential repairs or renovations. It is advisable to consult with a financial advisor or mortgage lender to determine the specific amount you need to save based on your individual circumstances.

Can I buy a house with no down payment?

Yes, it is possible to buy a house with no down payment, but it can be challenging. There are certain loan programs and options available that allow for zero or low down payment mortgages. However, these options often come with stricter eligibility criteria and may require the borrower to pay private mortgage insurance (PMI) or have a higher interest rate. Additionally, not having a down payment means borrowing a larger amount, which can increase the monthly mortgage payments and overall cost of the loan. It is advisable to thoroughly research and consult with a mortgage professional to understand the options and implications before pursuing a no down payment home purchase.

About Sarah Horvath

Sarah is an expert in the insurance, investing for retirement and cryptocurrency space.