Credit drives the world we live in today, and knowing where you stand is critical. It’s possible to use various entities, such as Vantage Score, created by the three major credit bureaus, and FICO scores, created by the Fair Isaac Corporation (FICO). It’s the latter that’s the most widely used today.

FICO scores have been around since 1998. Since then, the company has regularly revised its algorithm to calculate these scores, but the underlying principles haven’t changed. Your FICO score provides potential lenders – banks, insurance companies, mortgage providers, auto loan companies – a measure of the risk they’ll take if they allow you access to credit.

Why You Need to Check Your Credit Score

A majority of U.S. financial institutions use some version of credit as their preferred lending risk predictor, meaning you could have more than one FICO score.

When FICO releases a new version of its formula to include newer risk scenarios and changing consumer credit behavior, companies have the option to update to the newer version or continue to use the older version of the algorithm. As a result, two institutions checking your FICO score could get different results.

FICO relies on data from consumer reporting companies like TransUnion, Experian, and Equifax, so differences in your credit report at each of those agencies could also impact your FICO scores.

The most compelling reason for you to know your credit score is so you can be proactive about managing it. Once you learn how to read your credit report and find that your score needs improvement, you can do something about it before you apply for a loan or a credit card.

Other important reasons include:

- You’ll know what to expect before applying for credit: Your credit score determines how much credit a lender might offer you, and at what terms (rate, length of repayment etc.) Knowing your score will give you a fair idea of what to expect.

- You can forestall credit inquiries that might hurt your credit score: Lenders usually publish the minimum score required for borrowers to qualify. Each time a lender makes a new inquiry, it impacts your score. If you don’t meet the lender’s minimum criteria, knowing your score can help you squash damaging credit inquiries.

- Know which of your risk factors, such as payment history or outstanding debt, might be weak, and then work to improve them: If a lender declines your credit request, federal law requires the lender to disclose why. You’ll already know the risk factors that make you susceptible for a potential credit decline and can then work to improve those specific factors before reapplying for credit.

Know whether you’re looking at an educational score or the score that lenders use. The educational versions are proprietary models used by credit bureaus such as Equifax and TransUnion, and may differ from what lenders use, which could be a blend of FICO scores with other credit factors.

The Consumer Financial Protection Bureau’s guide is an excellent source for learning more about this.

Where You Can Get a Free Credit Score

All three major credit bureaus provide free annual credit reports upon request, but these will not necessarily show you your credit score. In addition to FICO itself, you can access your score through a network of authorized retailers and third-party partners through the company’s Open Access program. Many of these providers offer FICO scores for free.

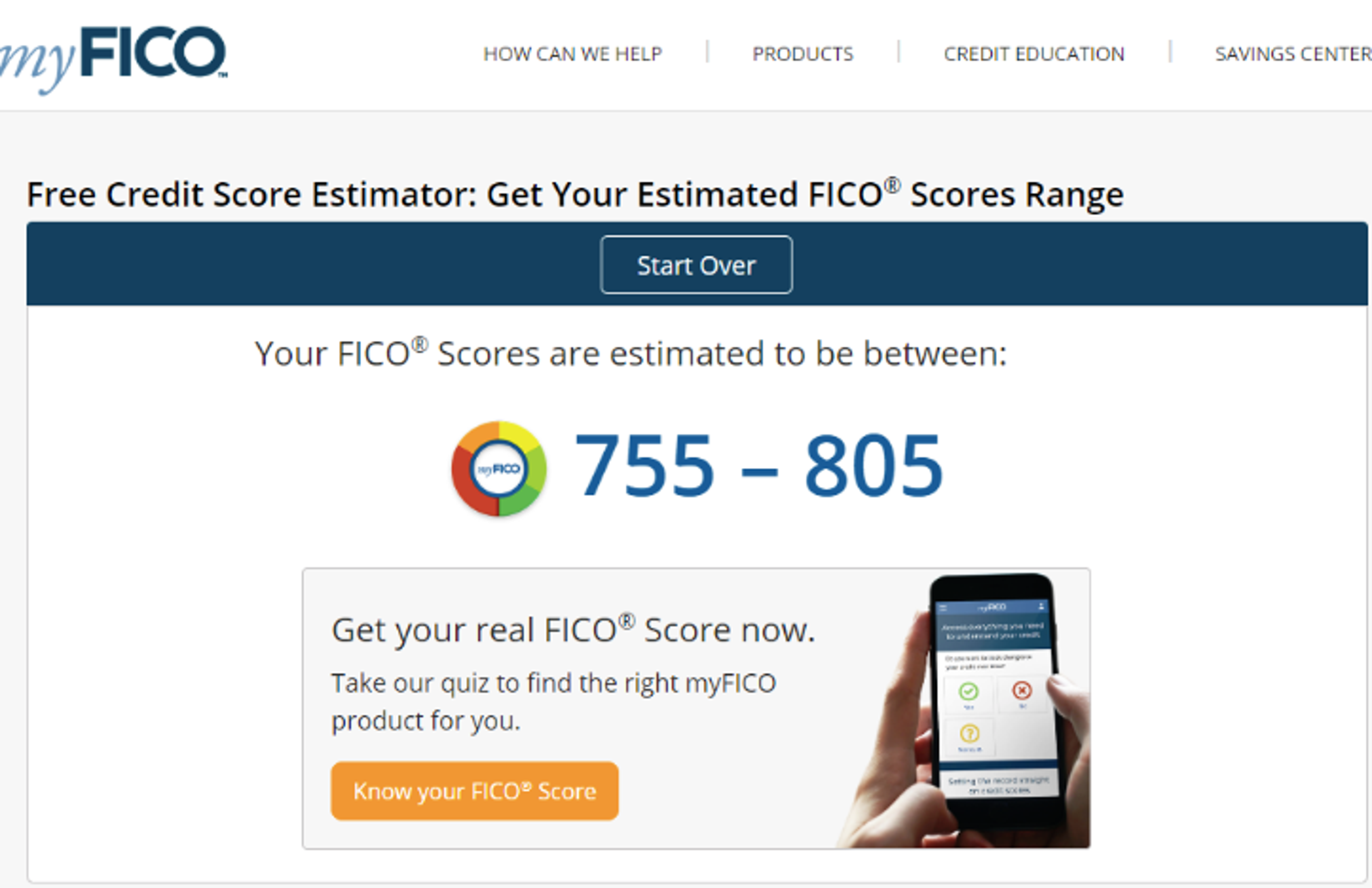

Place 1: Free Estimated Credit Score From FICO

If all you want is an estimate of your FICO score, you can go to myFICO and use the credit score estimator to get yours for free. There’s no need to create an account or to login.

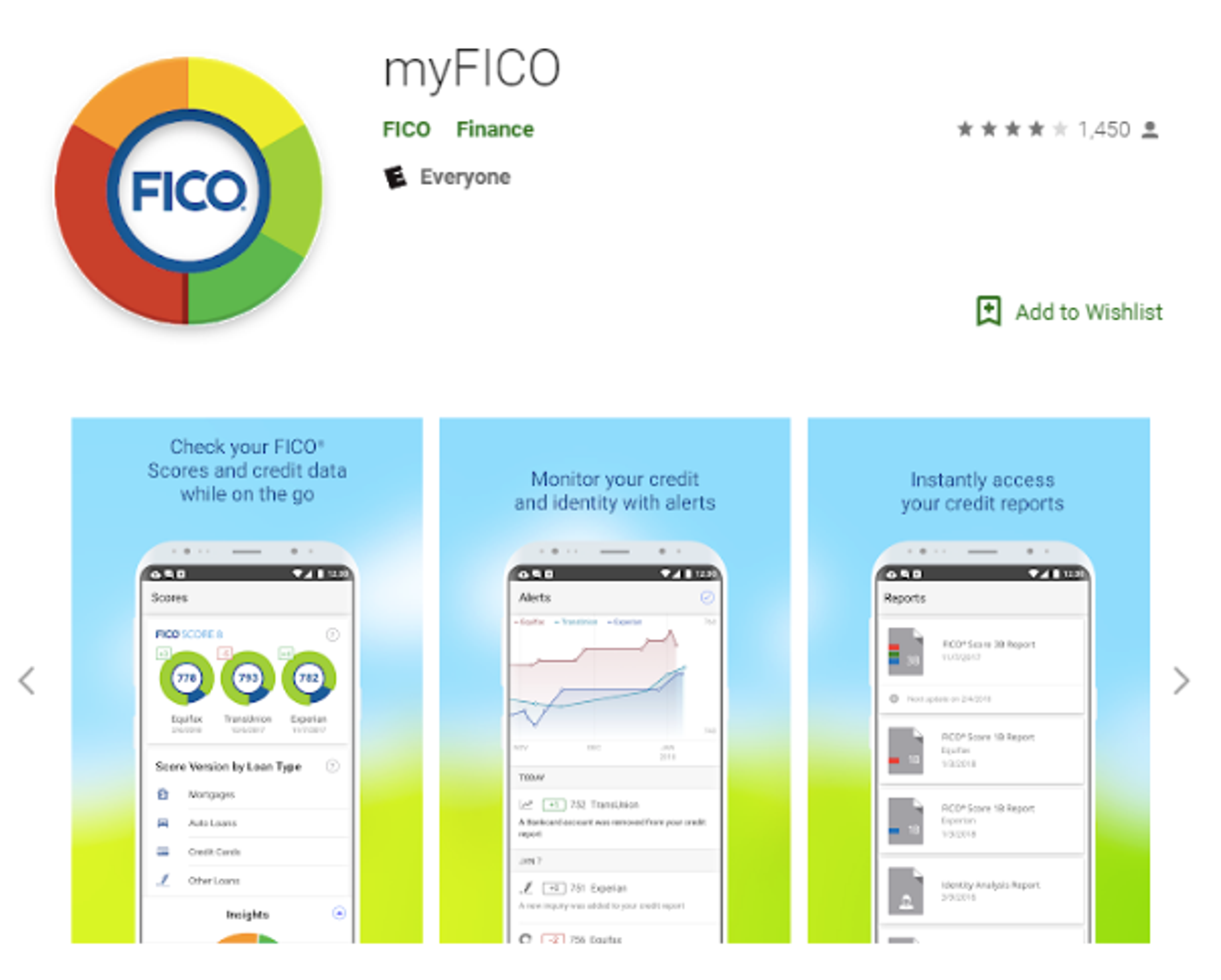

Place 2: FICO App

You can download the free myFICO app from GooglePlay and access a range of FICO data from your credit profile. The app is free, but you’ll need to subscribe to one of the FICO paid packages.

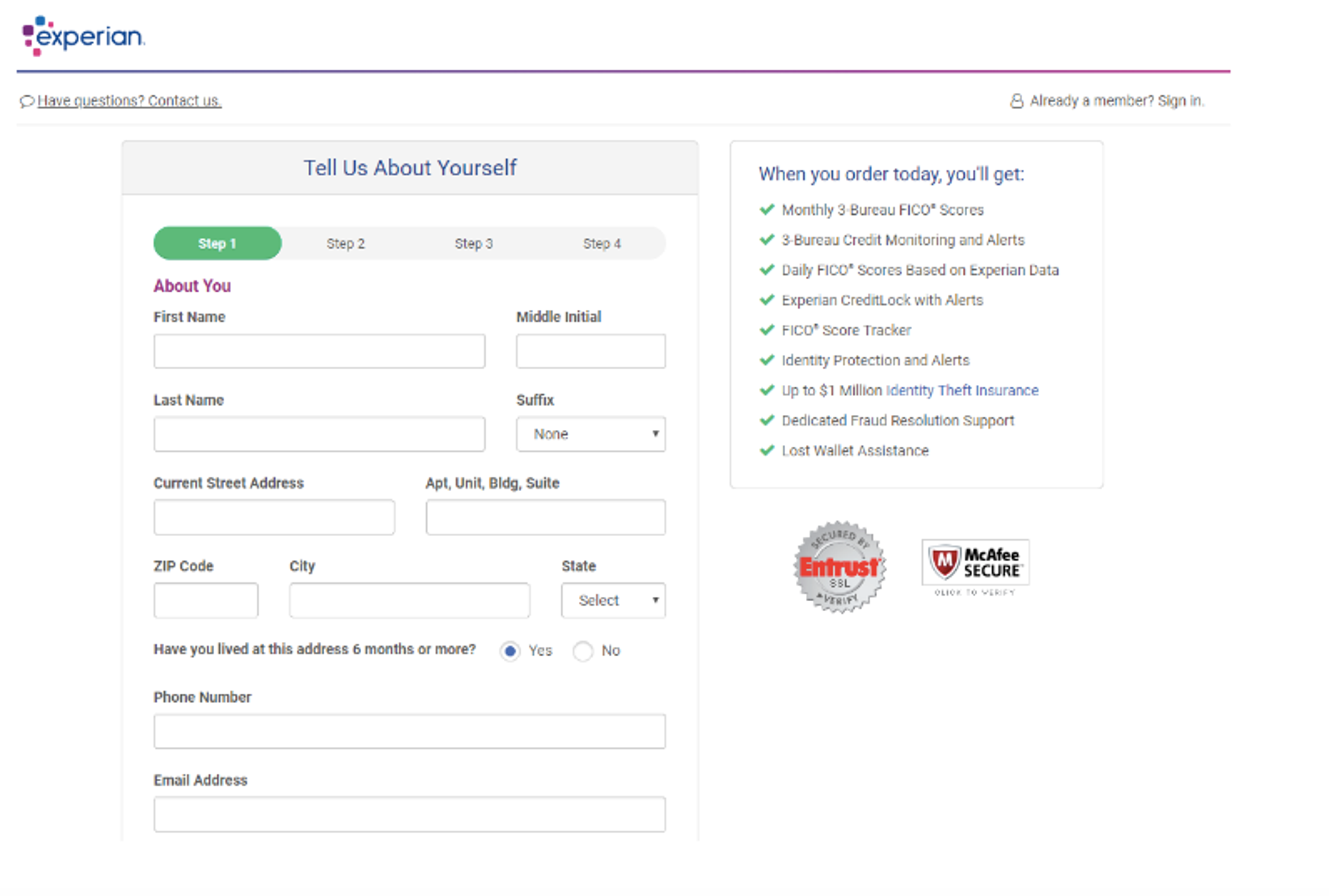

Place 3: Experian

Credit bureau Experian also offers access to free FICO scores, but you’ll need to register and provide some personal details first.

Place 4: Credit Card Issuers

Many credit card issuers provide credit scores (including FICO scores) on your monthly statement. You might also get your free credit score when you log into your online credit card account.

If you are a Discover card holder, you can access your free FICO score from here, and American Express Basic Card members can access their free FICO score from here.

Place 5: FICO Score Open Access Program

Over 160 financial institutions provide free FICO scores to their customers:

Over 100 credit counseling organizations also provide free access to FICO scores to their clients:

Place 6: Equifax

You can also get a copy of your credit score from Equifax for a fee. The service provides you with other details too, in addition to your credit score. However, this service is based on the Equifax Credit Score™ model.

Other Free Credit Score Sites

You can also view your credit score for free at several credit reporting sites such as Credit Karma and Credit Sesame. These sites offer an educational score, however, and you’ll need to sign up, create an account and provide some personal information.

Experian, Equifax and TransUnion have collaborated to create their own version of a credit score, called Vantage Score™. These use some of the same criteria that FICO uses, but includes some proprietary characteristics as well. You can access your VantageScore for free through a network of lenders and non-lender partners.

Final Thoughts

Experts recommend that you check your credit report at least once a year. However, that does not guarantee that you’ll find out what your credit score is. At a minimum, you should check your credit score before making an application for new credit, whether for credit cards, mortgages or car loans.

Whether it’s a FICO score, a Vantage Score™ or an educational score, you have both free and paid access to them all. Armed with knowledge of your credit score, you’re in a much better position to negotiate credit with prospective lenders.