A 401(k) is a retirement savings plan sponsored by an employer that allows employees to save and invest a portion of their salary before taxes are taken out.

A 401(k) is a powerful tool for saving for retirement. If you are employed, you may qualify for a 401(k) retirement plan. If you are eligible and have not yet enrolled to contribute, visit your human resources office promptly. Why?

A 401(k) is a type of retirement savings plan that allows employees to contribute a portion of their salary to a tax-advantaged investment account. Your employer might also offer an employer match program which means free money that has the potential to grow exponentially in your retirement account. While the concept may sound simple enough, there are various rules and guidelines that come into play when it comes to managing a 401(k) effectively. Benzinga breaks down everything you need to know about 401(k) plans and how they can benefit your retirement savings.

What Is a 401(k)?

401(k)s are a tax-advantaged savings and investing plan that employees can use to save for retirement. It allows you to contribute a fixed amount or percentage of your earnings and deduct that amount from your pre-tax income.

One of the benefits to contributing to a 401(k) is you don’t even have to think about it; it’s automatically deducted from your paycheck in the fixed amount or percentage you choose. In other words, you’re in total control of how much you contribute and what your investment choices are.

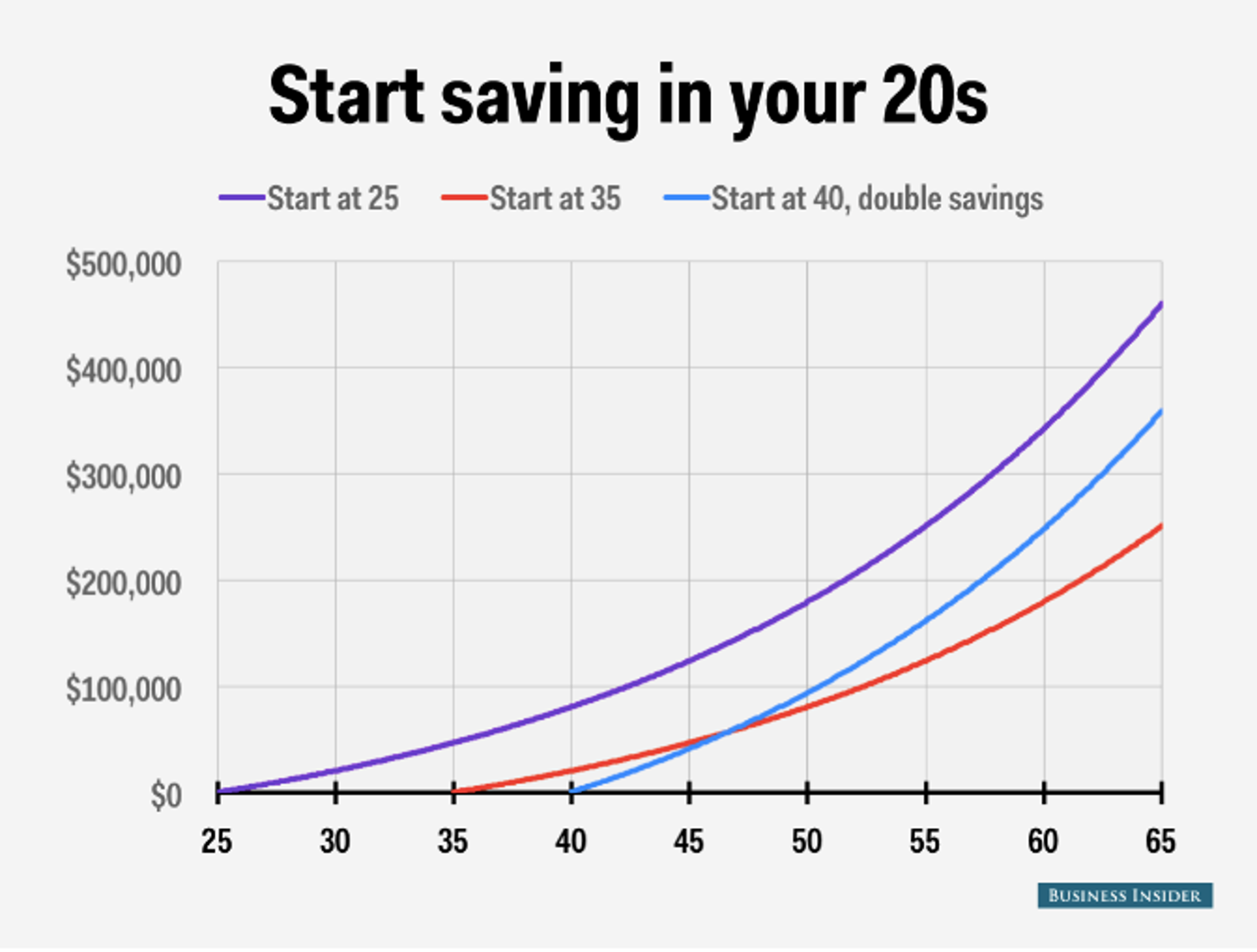

If funded early, the 401(k) is a perfect case study of the miracle of compound interest. The earlier you begin saving money in a 401(k) retirement savings plan, the better off you’ll be in your golden years.

Check out the chart for proof of why you’ll want to start earlier instead of later (although if you’re in your 40s and haven’t started saving, it’s never too late to start!)

How Does a 401(k) Work?

A 401(k) is a retirement savings plan offered by many employers in the United States. It allows employees to contribute a portion of their pre-tax earnings to a retirement account. The money you contribute to your 401(k) is typically invested in a variety of funds based on your risk tolerance and investment goals. Over time, your contributions, along with any employer matches and investment earnings, will grow tax-deferred until you begin withdrawing funds in retirement.

There are two main types of 401(k) plan. The main difference between a traditional 401k and a Roth 401k is how they are taxed:

- Traditional 401(k): In a traditional 401(k), contributions are made pre-tax, meaning you don't pay taxes on the money you contribute until you withdraw it during retirement.

- Roth 401(k): With a Roth 401(k), contributions are made after-tax, so you pay taxes on the money you contribute now, but withdrawals in retirement are tax-free.

401(k) Contribution Limits

You set the amount regularly deducted as a 401(k) contribution as long as you don’t go over the annual limit. The maximum amount an employee can contribute to a 401(k) plan is adjusted periodically to account for inflation. For the year 2024, the annual limit on employee contributions to a 401(k) is $23,000 for workers under the age of 50. However, for individuals aged 50 and over, they are eligible to make a catch-up contribution of $7,500 on top of the annual limit.

Employer Matching Contribution Limits

Employers may also contribute to their employees' 401(k) plans. Some employers have waiting periods before allowing contributions to retirement accounts, and some require a certain amount of time before becoming fully vested. Employers may also match employee contributions up to a certain percentage.

When considering both employee and employer contributions, there is a total maximum contribution limit for the year. For workers under 50 years old, the total employee-employer contributions cannot exceed $69,000 annually. If the catch-up contribution for those 50 and over is included, the limit is increased to $76,500.

At a minimum, it’s a good idea to contribute the amount your employer is willing to match because each dollar matched equals a 100% gain. Those employee contributions can then be itemized as deductions from adjusted gross income by your tax preparer.

401(k) Withdrawals

Here are some things to keep in mind before making 401k withdrawals.

- 401(k) withdrawals before the age of 59 ½ can result in early withdrawal penalties, typically around 10% of the amount withdrawn, as well as income taxes.

- Hardship withdrawals may be allowed for specific reasons such as medical expenses or preventing eviction, but they are still subject to income taxes.

- Taking out a loan from your 401(k) may be an option for major expenses, but leaving your job before repayment can result in taxes and penalties on the remaining balance.

401(k) Required Minimum Distributions (RMD)

The purpose of RMDs is to ensure that individuals are taking distributions from their retirement accounts and not just accumulating wealth indefinitely. Important things to remember include:

Required minimum distributions (RMDs) are mandatory withdrawals that individuals must take from their traditional 401(k) accounts when you reach age 72 (73 if you reach age 72 after Dec. 31, 2022).

RMDs are calculated based on life expectancy and withdrawals from traditional 401(k) accounts are considered taxable income.

Roth 401(k) accounts offer a tax advantage as qualified withdrawals are not subject to taxation, making it important to understand the rules and requirements surrounding RMDs for traditional accounts.

Pros and Cons of 401(k)s

As with most things, there are prons and cons to 401(k)s. Here's an overview of the benefits and drawbacks of having a 401(k) plan.

Pros

- They offer of a substantial tax deduction

- Long-term tax-deferred growth

- Portability should employment change

- Regular monthly contributions allow you to take advantage of dollar-cost averaging

Cons

- Smaller companies may depend more on in-house staff as the employees’ point of contact with their retirement plan, instead of an actual plan administrator

- An account holder can also create problems with investment choices and when rolling over a distribution to another firm, so choose with care

- Limited investment choices offered by your 401(k) provider

- High expenses due to fees built into your 401(k) plan

Best 401k Advisors

Not sure what to do with you 401(k)? Get advice from one of these professionals.

- Best For:Comparing AdvisorsVIEW PROS & CONS:securely through SmartAsset Financial Advisors's website

- Best For:Virtual Financial PlanningVIEW PROS & CONS:securely through Money Pickle's website

What Happens to My 401k if I Quit?

When you leave a job, it’s natural to want to take your old 401(k) with you to your new job. However, that’s not the only option. There are actually four options you can consider:

- Cash out your 401(k)

- Leave your money in your old 401(k) plan

- Transfer your money over to your new job’s 401(k) plan

- Roll over your money into an IRA

Each has its merits, but you’ll want to watch the first one. You’ll be shouldered with a hefty tax bill (10%) if you decide to cash it out, not to mention, you’ll lose out the money you’ve saved for your golden years.

If you do decide to roll over your 401(k) because of a change in employment, your old 401(k) should be rolled over by requesting a full distribution and deposit into an IRA or a 401(k) within 60 days.

There could be some solid reasons you decide not to roll over your money and keep it in your old account: Your fees in your old plan could be lower or you could be happy with your old 401(k)’s performance and investment options. Ultimately, you’ll need to carefully consider which is more advantageous to you.

It is important to understand the specific rules and regulations regarding your 401k plan and consult with a financial advisors and tax experts before making any decisions.

Roll Over With Beagle

Beagle fills a unique niche in the 401k space by recognizing that millions of Americans have left behind 401k accounts when they’ve changed careers, switched jobs, moved from one company to another or lost a loved one who had untapped retirement savings. This is a new take on a traditional rollover with two main services:

- Search and rollover services, allowing you to find old 401k accounts and roll them into a new account

- 401k loans, allowing you to take loans from your old 401k accounts at net 0% interest

Plus, Beagle offers the option to build a new 401k account for your rollover with a $3.99 monthly maintenance fee. You can unlock previous saving potential, start planning for retirement, bolster your current retirement portfolio and take back money you contributed long ago.

Start Your Retirement Savings With 401(k)s

If you have the opportunity, invest in your company’s 401(k) plan because of the ever-popular matching contribution.

Know where to go and which questions to ask, too. Most often, your point of contact with your company’s 401(k) starts with the financial statement issued by your company’s administrator. There, you’ll find contacts that may include your company’s human resources or benefits department, the administrator hired to establish the plan or your retirement funds custodian. Every administrator has a slightly different procedure for making changes to investments, contributions or distributions.

Another point of contact may be the custodian who acts as investment manager, holding the assets and issuing financial statements. Only by further investigation can you determine where, how and by whom changes are made.

Don’t have a 401(k) option through your employer? Read more about how to start investing for retirement.

Frequently Asked Questions

Is 401k same as IRA?

No, 401k and IRA are not the same. A 401k is an employer-sponsored retirement savings plan, while an IRA (Individual Retirement Account) is a personal retirement account that individuals can open on their own. It allows individuals to contribute a certain amount of money each year, which is then invested in a wide range of investment options, such as stocks, bonds, mutual funds or other investment vehicles.

How does a 401k make you money?

A 401k is a retirement savings account where individuals can contribute a portion of their salary before taxes, which provides tax benefits. The money is invested in stocks, bonds, and mutual funds, allowing it to potentially grow over time. Employers may also offer matching contributions. However, it’s important to note that the performance of investments in a 401k can fluctuate, and there are rules and restrictions regarding when and how the money can be withdrawn.

Are 401k good or bad?

A 401k can be a good way to save for retirement due to tax advantages and potential employer matching contributions, but some may see it as having limited investment options and control over savings. It’s important to consider factors like investment options, fees, and employer contributions before deciding if a 401k is right for you.

About Melissa Brock

Melissa Brock is a versatile freelance writer and financial editor, recognized for her expertise in higher education, personal finance, and investing. With over a decade of experience in online content creation, Melissa has established herself as a trusted source for insightful financial advice and educational resources. Her writing prowess extends to diverse topics, including trading, cryptocurrency, and college savings. Melissa’s commitment to empowering readers with practical knowledge and actionable insights is evident in her contributions to various reputable platforms. As a dedicated financial editor, she meticulously covers the complexities of personal finance, ensuring readers have the tools they need to make informed decisions. Melissa’s work exemplifies her passion for educating and informing audiences on matters of financial literacy and investment strategies.