If you're thinking of opening a brokerage account and have narrowed it down to Vanguard and Wealthfront, you're in the right place. Let's explore both platforms so you can decide what brokerage is best for you.

Overview: Vanguard vs. Wealthfront

Vanguard has stood at the forefront of financial service providers since the 1970s—founder Jack Bogle invented the index fund, and the company has pioneered wealth management ever since.

The company services clients through its Personal Advisor Services, and its strength lies in Vanguard’s own mutual funds and ETFs sold through brokers and representatives. For more information, check out Benzinga’sVanguard Review. In contrast, Wealthfront, a much newer company with $12 billion under management, offers investment services through an automated system you can customize for your investment objectives and risk tolerance.

Wealthfront’s investing strategies were developed by a team led by Random Walk Theory pioneer Dr. Burton Malkiel.Wealthfront can analyze your financial habits and determine likely future scenarios. In addition, Wealthfront offers a low-cost automatic investing option if you’re interested in investing your savings. Read Benzinga’sWealthfront Review for more information.

Wealthfront vs. Vanguard: Platform and Tools

Wealthfront offers a sophisticated platform for desktop and mobile and Vanguard has no platform. Vanguard only accepts limited order types online and gives you the option of speaking to a financial advisor.

What Wealthfront Offers

In addition to mobile, web and desktop platforms, Wealthfront’s dashboard displays an in-depth look at your portfolio’s performance. Basically, you input all of your financial accounts into Wealthfront, which then analyzes and evaluates your finances. The software provides recommendations for diversification, taxes, fees and more, which are personalized to your specific financial profile and risk tolerance level.

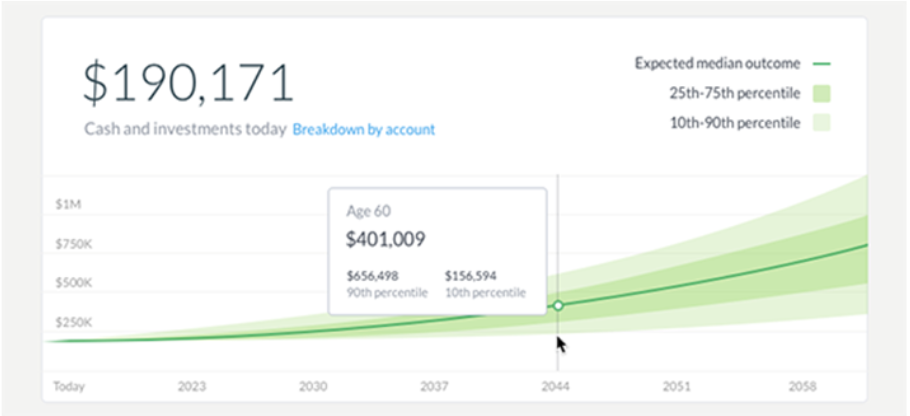

Wealthfront also offers an interactive version of Wealthfront’s desktop graphic that uses savings and investment returns to determine retirement spending targets. In addition to the dashboard, Wealthfront created Path, a comprehensive financial planning and investment solution that analyzes your financial habits and determines future outcomes. Path gives you the answer to questions such as “How much will my net worth be by retirement?” or “How much should I be saving today?”

What Vanguard Offers

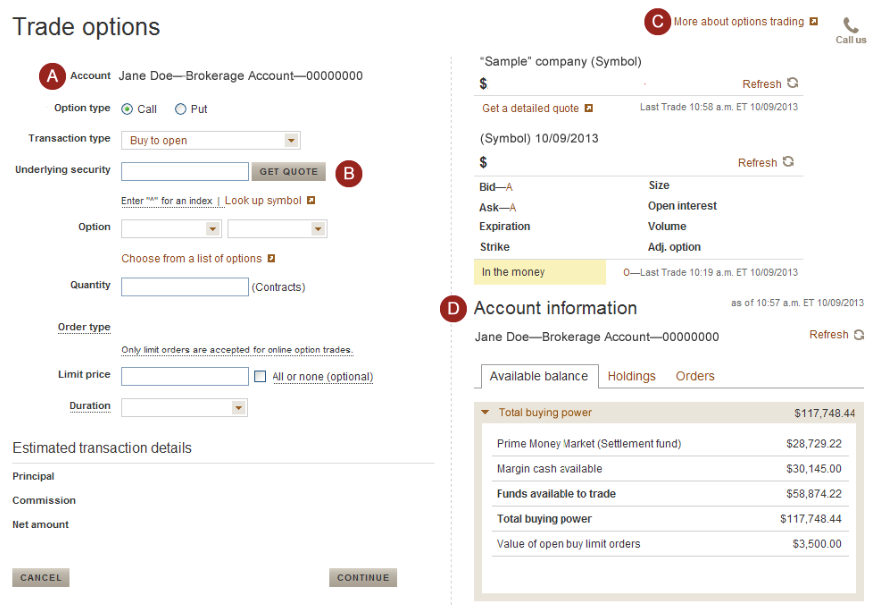

Vanguard has built its empire on the personal advisor model, which doesn’t cater to online and automated app users. Though it doesn’t have an online trading platform, Vanguard has over $5 trillion under management and continues to be the largest mutual fund and second-largest ETF dealer in the world.Vanguard offers clients a detailed order-entry page on its website, where clients can enter buy, sell, stop and stop-loss orders for ETFs and mutual funds. An example of one of Vanguard’s order entry pages can be seen below:

Bottom Line

Wealthfront’s main and mobile platforms have little competition from Vanguard since the two companies seem to be on opposite ends of the financial services spectrum. The old-school personal advisor-based financial management model that Vanguard offers differs notably from the automated algorithm-based robo-advisor model Wealthfront offers. Depending on what you need, either company could be a good fit.

Wealthfront vs. Vanguard: Research Offerings

Both companies do their own research; Wealthfront’s team uses proven algorithm-driven investment strategies. In contrast, Vanguard takes a more traditional approach.

What Wealthfront Offers

Much like other automated investment advisors, Wealthfront bases its strategies on modern portfolio theory (MPT). Its software then determines the best strategies depending on your goals and optimizes your portfolio.

To create a portfolio, Wealthfront begins by identifying the types of asset classes that would work best for your objectives. The program evaluates historical data to determine risk-reward relationships for each asset class, including foreign and domestic stocks, bonds, etc. The program then allocates investments geared to your particular risk tolerance level and financial situation.

Once in place, the system monitors and rebalances your portfolio periodically.Wealthfront also offers tax-loss harvesting, which sells a declining ETF once the asset meets certain conditions. A highly-correlated ETF then replaces the ETF that was sold. You can then apply the realized loss to lower your taxes, while the ETF you purchased maintains your position in the market.

Wealthfront offers a more advanced version of tax-loss harvesting using stocks instead of ETFs. Known as stock-level tax-loss harvesting, the program finds suitable tax-saving opportunities for your portfolio using single stocks.

What Vanguard Offers

Vanguard’s website features a research and commentary section which mostly contains the company’s own in-house research and articles. The well-written articles focus on global investment markets, macroeconomic news and wealth management.

A large number of articles focus on fixed-income markets and target retirees or those preparing to retire.In addition to the research on their website, Vanguard hosts a monthly investment commentary podcast with a focus on client issues. The firm also offers another program called ETF Perspectives that features outside ETF experts.

Bottom Line

In the realm of research, both companies perform their own research and invest clients’ money, but a decision between the two largely depends on your financial objectives, tax situation, and other considerations.

Wealthfront vs. Vanguard: Commissions and Fees

Both companies lead the industry in low cost. Wealthfront’s 0.25% yearly charge on funds under management are at the low end and Vanguard’s funds also keep investor costs well below the industry standard.

Wealthfront’s Commissions and Fees

Wealthfront charges an annual fee of 0.25% of funds under management and requires a minimum of $500 to open an account.

Vanguard's Commissions and Fees

A Vanguard account can be opened with the purchase of at least one ETF share, which costs between $50 and $400. Vanguard’s fee schedule is a bit more complex than Wealthfront’s and begins at $7 for the first 25 online stock trades.

Afterward, Vanguard charges $20 for trades under $50,000 and Vanguard ETFs (over 1,800) incur no fee. The cost is $7 for online trades from $50,000 to $500,000 for Voyager Services Vanguard products and $2 for online trades from $500,000 to $1 million for Voyager Select Services Vanguard products.

Bottom Line

Wealthfront’s straight 0.25% fee on managed funds compares favorably with Vanguard’s rather complicated fee schedule. Vanguard discourages short term trading and favors clients who just want the company to manage their funds.

Wealthfront vs. Vanguard: Security

Both companies offer Securities Investment Protection Corp. (SIPC) protection and use advanced encryption for client security.

What Wealthfront Offers

As a member of the SIPC, Wealthfront Brokerage Corporation protects the securities of its members up to $500,000, which includes $250,000 for cash claims. In addition, all fully-paid (not margined) securities are held in the broker’s name.

Wealthfront only invests in SIPC-covered securities registered in its name at the Depository Trust Company, or DTC.Securities held by Wealthfront on your behalf are held in separate accounts. Neither Wealthfront nor Wealthfront Brokerage Corporation trade in securities for their own accounts; Wealthfront only makes trades on behalf of its clients' accounts.

What Vanguard Offers

Also a member of the SIPC, Vanguard insures up to $500,000in segregated accounts with a limit of $250,000 insured for uninvested cash balances. Also, large balance accounts have insurance issued by Lloyds of London up to an aggregate of $250 million.

Bottom Line

Both companies offer the same account insurance from the SIPC, and both companies hold client securities and cash in segregated accounts. Therefore, very little difference in security measures exists between the companies, with the exception that Vanguard insures large accounts with an aggregate policy of $250 million from Lloyds of London.

Wealthfront vs. Vanguard: Customer Support

Vanguard offers customer support via telephone during the week. Wealthfront has a more cryptic support system that involves filling out a form on a webpage and then waiting to hear back from their support team.

What Wealthfront Offers

Wealthfront’s client support page states that its service specialists, which are all Series 7 certified, can be reached via phone or email. Nevertheless, no phone number can be found on its help center page.To get online support at Wealthfront, a request form must be filled out with all the necessary information carefully detailed, including a return email address and phone number.

Wealthfront states that general requests get answered within 24 business hours; however, some requests may require significant research, which could delay response.

What Vanguard Offers

Vanguard’s website has a client support center page that gives their clients a choice of 16 boxes with different FAQs describing brokerage services, ETFs, IRAs, etc. While some of the FAQs link to web pages, others require the client or potential client to mail in a request for information from Vanguard’s headquarters.

Bottom Line

Neither company offers a live chat button on its website. Vanguard offers telephone service, while Wealthfront also has a customer support phone line, but it does not appear on its help center webpage. When it comes to customer service, Vanguard seems more service-oriented and is preferable for investors who like that feature.

Wealthfront vs. Vanguard: Tradable Asset Classes

Wealthfront offers ETFs and stocks as principal tradable assets, while Vanguard includes its family of mutual funds and ETFs.

What Wealthfront Offers

Wealthfront offers ETFs which include U.S. and foreign stocks, dividend stocks, emerging market stocks, natural resources, real estate, U.S. government and corporate bonds, U.S. Treasury Inflation-Protected Securities (TIPS), municipal bonds, emerging market bonds, and risk parity.

What Vanguard Offers

Vanguard offers mutual funds and ETFs, which have a wide range of market options. In addition to its own mutual funds and ETFs, Vanguard offers other companies' funds and ETFs, plus trading in individual stocks, CDs, and bonds.

Bottom Line

Despite the limited types of products available to trade on Vanguard, the variety within the individual choices could be sufficient for an investor who would rather “set it and forget it.” Wealthfront’s limited offerings would definitely suffice for automated investments and clients who do not wish to manage their own accounts.

Wealthfront vs. Vanguard: Ease of Use

You can feel at home on Wealthfront’s platform, with its intuitive nature and easy-to-read interface. Vanguard’s order entry page also seems easy to use and only takes a few steps to enter orders.

What Wealthfront Offers

Wealthfront’s platforms are easily accessed through the web, on a desktop computer or mobile device. The company also has an easy-to-use interface. You can consolidate all of your investments seamlessly.

The software allows you to compare different investments and accounts, like your stock holdings with your real estate holdings. The software also lets you transfer money directly on all platforms, including mobile. The risk tolerance score must be changed on a computer, not on your mobile. Wealthfront also provides ease of use when it comes to managing your money.

They have a Cash Account that currently has an APY of 2.51% with a $1 minimum and is FDIC-insured up to $1 million. They also have a Portfolio Line of Credit that allows clients with at least $100,000 invested in a taxable account to instantly access their funds with no paperwork or credit check.

Investors can access up to 30% of the account's value and, in most cases, can receive their funds in less than 24 hours.

What Vanguard Offers

With respect to simplicity and ease of use, entering orders on Vanguard’s webpage could not be easier. Vanguard’s nonexistent trading platform forces its clientele to use the personal advisor system that the company was founded upon. Also, Vanguard charges an extra $25 for handling phone-assisted orders.

Bottom Line

Wealthfront’s intuitive mobile, web and desktop platforms make managing your money extremely simple. Vanguard’s old-school interface and the fact that you must pay extra to interact with an account representative over the phone makes Wealthfront a preferable choice.

Final Thoughts

Both companies deal with similar types of securities but stand worlds apart with respect to technology and automation. Vanguard is ideal for a more seasoned investor because of its low costs and in-house mutual funds and ETFs. On the other hand, Wealthfront appeals to less hands-on, less experienced investors.Learn more about some of Benzinga’s best ways to invest. ;

Broker | Best For | Fees | Minimum Balance | Opening Deposit |

| 0.25% per year | $500 | $500 minimum opening balance | |

|

| $0 | One share of an ETF that costs between $50 - $400 |

About Jay and Julie Hawk

Jay and Julie Hawk are a married financial writing and authorship team who co-founded TheFXperts, a notable financial writing services provider. The Hawks each worked professionally in the financial markets and have more than 40 years of trading experience among them. Together, they write books, trade forex online for their own account and others, mentor traders, and have worked actively as professional freelance writers specializing in financial topics for over 15 years.