In 1974, the Employee Retirement Income Security Act (ERISA) was born. ERISA legislated regulations for pension, retirement, benefit and healthcare plans as well as established the Individual Retirement Account (IRA). But, even when you reach your contribution limit every year and build your retirement account responsibly, there are times when you need to roll over. So, what do you do and how to make the most of a retirement account that’s changing?

IRAs: What Are They?

As an incentive for individual taxpayers to save privately for their own retirements, ERISA allowed for up to a $2,000 tax deduction (now $6,000) if that amount were deposited into an IRA.

For over a decade, the IRA deduction was a no-brainer for tax preparers as the deposit could be made on the filing date, April 15, and taken as a deduction from taxable income for the previous year.

A $2,000 IRA contribution could mean over $1,000 tax savings at 1970s tax rates. But the Tax Reform Act of 1986 phased out deductions for high-income taxpayers who were also covered by an employer’s ERISA qualified plan like a 401(k). Yes, you’re getting the tax benefit of these accounts, and you could be much more flexible in how you managed them.

Why IRAs are Advantageous

The tax deduction makes the IRA a popular retirement strategy, but it is the deferral of taxation on annual earning that makes the IRA a superior long-term wealth builder. Used as a workplace retirement account, employers can add these accounts to a benefit plan, match an employee contribution, avoid tax consequences themselves and keep everyone happy.

The IRA account holder does not pay income or capital gains tax on annual IRA investment earnings. Instead, the IRA holder pays ordinary income tax on distributions taken in retirement.

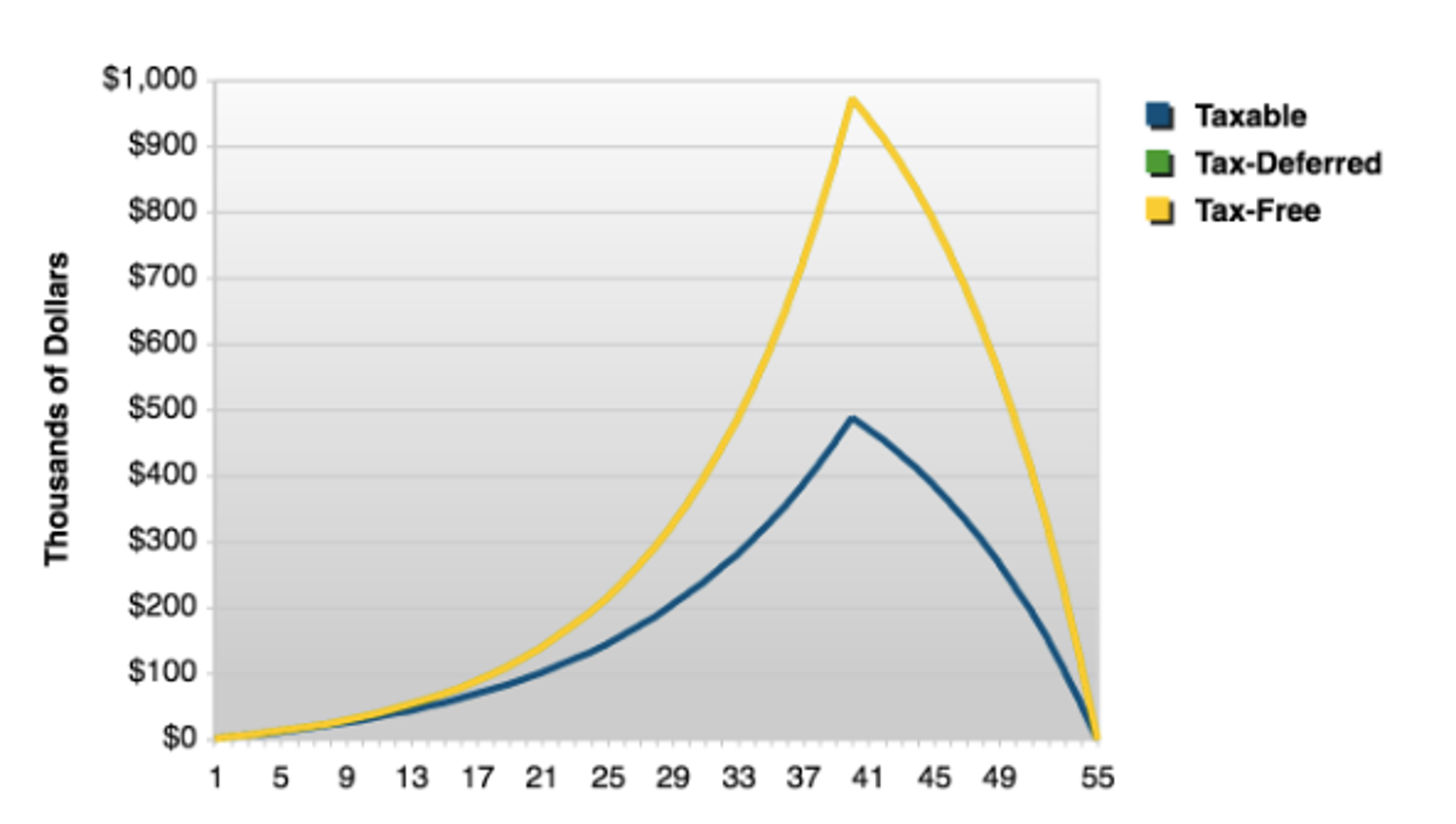

A Baby Boomer born in 1946 who deposited $2,000 per year into an IRA account earning an average 10% would have amassed over $973,000 when the required minimum distribution (RMD) activated at age 70½ in 2016.

The account holder would then be required to withdraw at least 5% or over $48,000 per year. But an investor using a taxable account would have accumulated under $490,000 and a first annual payment of less than $25,000.

IRAs: Tax Distribution

A withdrawal from an IRA by an investor who is younger than 59½ is subject to a 10% tax penalty in addition to ordinary income tax. A distribution taken from an IRA or other ERISA-qualified account and re-deposited into another or the same qualified account within 60 days of the distribution date qualifies as a tax-free “rollover” of those retirement assets.

A Rollover IRA is an Individual Retirement Account that has been established to receive a distribution from another ERISA-qualified account. Retirement accounts can be consolidated using a Rollover IRA as the collection point. Consolidation limits investment expenses and simplifies management for the individual investor.

How to Choose Where to Rollover Your IRA

A Rollover IRA should allow you to efficiently change investments and strategy as lifestyle and physical needs change and should offer a wide variety of quality mutual funds in the early asset-building years. As you accumulate more assets and experience, common stocks may become more attractive when moving rollover assets from one plan account to another.

Because there are so many investing options, you should do a good bit of research before diving into a new administrator or fund manager.

But when you, as an IRA investor, are nearing retirement, bonds may be more appropriate securities for safety and income. Passive investment management by an algorithmic investment manager may be more appropriate if you’re uninterested in the vagaries of the market.

- Best For:Comparing AdvisorsVIEW PROS & CONS:securely through SmartAsset Financial Advisors's website

- Best For:Virtual Financial PlanningVIEW PROS & CONS:securely through Money Pickle's website

Choose the Right Rollover IRA for Your Situation

Every individual who prepares for retirement must take advantage of tax-deferred saving wherever possible. Accumulated retirement funds are most efficiently managed in one flexible, accessible and trusted account. An individual retirement account, then, is more flexible than you might have believed. Speak to an investment advisor, research with Benzinga and learn more how to optimize your retirement savings.

Frequently Asked Questions

Are rollover IRAs a good idea?

Rollover IRAs can be a very good idea for you, depending on your financial situation. You can gain access to your money much earlier, but there are loopholes that may make withdrawals more difficult.

When should I do an IRA rollover?

You have 60 days from the time you receive your IRA distribution to rollover into a new IRA account.

Do you earn money with a rollover IRA?

When you use a rollover IRA, you can avoid immediate taxation on those funds and ensure that your money is earning as soon as it enters a new account with a new investment manager.