We all have heard the horror stories accompanying those with bad credit, but did you know that having no credit can be just as bad? In some cases, creditors may issue leniency to applicants with bad credit if they recently lost a job or received an unexpected medical bill. However, applicants with no credit are a total mystery — there’s no way to tell if a consumer with no credit will pay bills on time or cause the need for a credit agency intervention due to ignoring the minimum payments.

It’s a classic catch-22; you need a credit card to pay bills and build credit, but creditors will be hesitant to issue credit if you have no credit history. Thankfully, there are a few ways for men and women with no credit to successfully sign up for a credit card. Read our guide to learn more about how to build credit and get your hands on your first credit card.

Why You Need Credit to Get a Credit Card

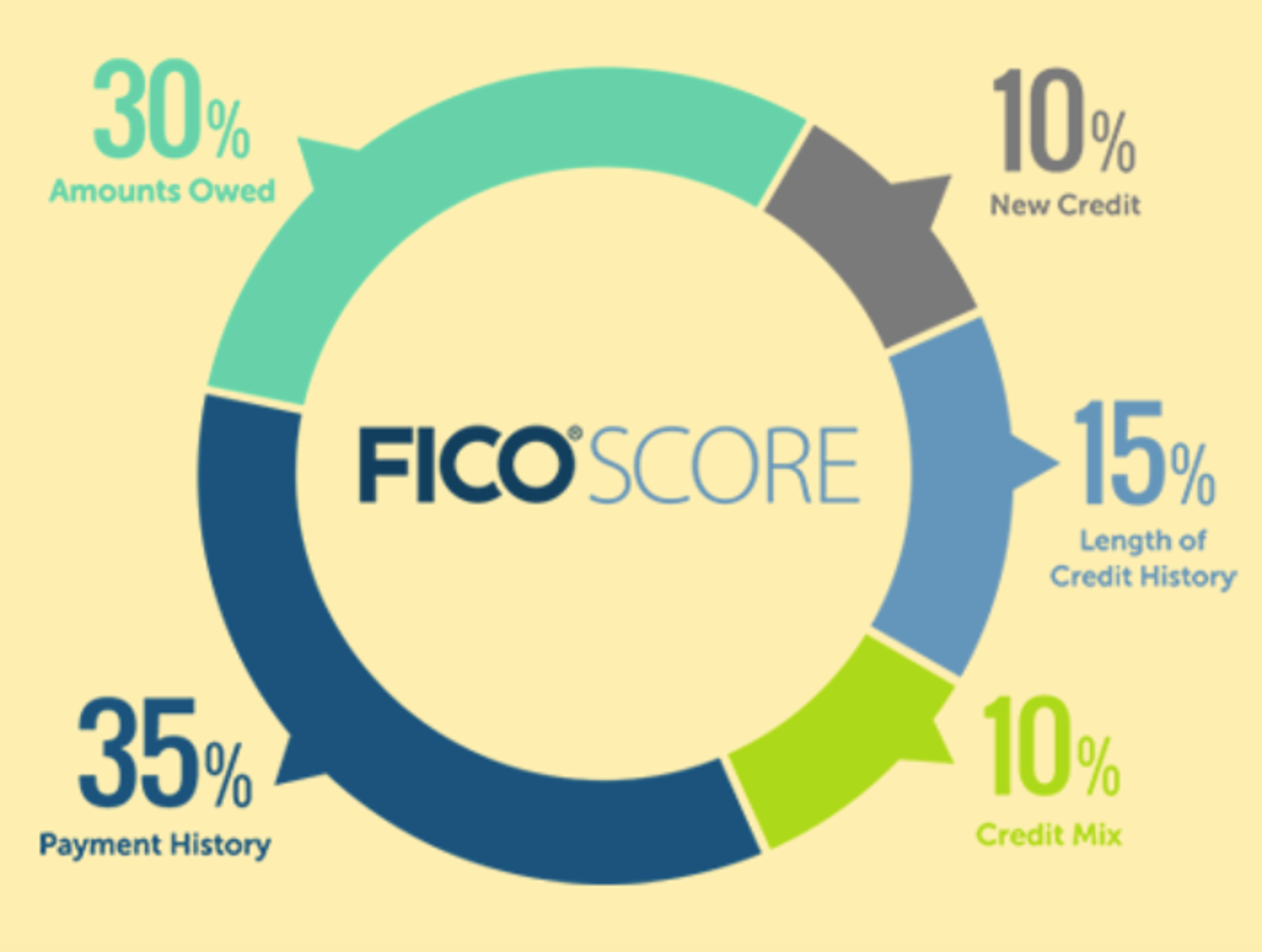

Your credit score is a numerical rating of how much you rely on credit to cover your expenses rather than money held in your debit or savings accounts. Your credit score is composed of factors like how often you pay bills late, how much credit you use a month, and how often you attempt to open new accounts. Extending credit to you is an inherent risk to a creditor.

When a credit card company extends you a line of credit, they bank on the hope that you’ll pay it back. If you don’t, the creditor will end up footing your bills. To get their money back, a creditor can sue you or sell your debt to a collection agency. However, these are both long, tedious, and expensive processes. It’s much less expensive for a credit card company to limit extending credit to consumers who have proven themselves to be fiscally responsible, as prevention is better than cure.

Your credit report offers creditors a peek into your past financial moves and is a good indicator for your future behavior. An applicant with a high credit score probably pays bills on time, doesn’t spend more than he or she can pay back, and splits financial responsibilities equally between savings and borrowed money. An applicant with poor credit probably got his score from multiple missed payments or credit extensions.

If you have no credit, you are a total risk to the credit card company, as they can’t tell which category you fall into. This is why many creditors have policies in place to deny or strictly limit credit requested for these types of accounts.

What to Consider Before You Apply for a Credit Card

If you think credit card payments are the only way to build credit, think again! If you don’t really want a credit card but you know you need to build credit for your future goals, consider employing one of these strategies for building credit without having to get a credit card:

Keep paying off old bills

Student loan payments and auto loan bills might be a pain, but both report your payment history to credit bureaus. However, each payment will not immediately show up on your credit report and will take time to be added to your record. If you are in the early stages of paying back a loan, keep making your timely payments. Once you have logged enough on-time payments, your credit score will begin to reflect this dedication.

Become an authorized user on someone else’s account

If you are on an account accompanied by someone with a proven credit history, this can be a fast-track way to building your personal credit. If you have a significant other or family member with a credit card, ask a significant other or family member if you can be added as an authorized user on their account. This will grant you full privileges to use the card, but you will be under no obligations to make any form of monthly payment or charge. You’ll build credit simply for being on the account.

However, changes in the way the card is used will also be reflected on your credit report, even if you aren’t doing any spending. For example, if you’re on an account with another irresponsible user who does not pay his or her bills on time, your credit score will suffer alongside theirs. You’ll want to choose someone who is trustworthy and who knows how to manage his or her finances.

Get a loan

One of the best ways to prove your ability to pay back debt is to make regular, on-time, and in-full payments on a loan ahead of schedule. Contact your bank or credit union and inquire about the process of getting a small personal loan. Many banks and credit unions will be willing to issue you a small, unsecured loan even if you do not have credit. If you do not qualify for a traditional unsecured loan, peer-to-peer lending services also report to credit bureaus and typically have higher approval rates.

Get credit for your rent payments

Even if you have no loans or have never owned a credit card, you are likely making utility and rent payments. While this payment information is usually not reported, adding it to your credit profile can help you build a positive payment history for long-standing bills. Unfortunately, you cannot report your rent payments yourself. Talk to your landlord and request that he or she begin reporting rent payments to the three major credit bureaus, or work with a third-party service (like Rental Kharma or RentTrack) who will report to credit institutions for them.

How to Apply for a Secured Credit Card

Follow these 3 steps for a seamless process.

Step 1: Sign Up for a Student Credit Card

If you are currently enrolled in college, you may qualify for a student credit card from Discover, Visa, or another major credit card company. These student cards are designed with young adults in mind, and their application process assumes students do not have enough credit or enough payment history to have a credit score. Student credit cards have strict limitations on spending.

Don’t be surprised if your card only allows you to charge $500 a month when you open it. However, for young men and women who are still building their credit profiles, charging a pizza or coffee once a month, and paying the full balance every month, is one of the fastest ways to see credit changes.

Step 2: Sign Up for a Secured Credit Card

A secured credit card is a card that is backed specifically by collateral on the account. This can then be seized in the event that you don’t pay off your debts. Unlike an unsecured card (which is only backed by legal responsibility), secured credit cards offer the creditor a safety net.

It ensures that they can recover some of the value of the credit extended if you fail to make your payments. Credit card companies are much more likely to approve a consumer with thin to no credit for a secured card when compared to an unsecured card.

Most major credit card companies offer secured credit cards. To get a one, start by comparing the major credit providers and put in an application for the company that best suits your needs. You’ll want to submit only one application because creditors will run a hard check on your credit before approving you, which will show up on your credit report. After you’ve applied, the credit card company will use your credit report, and their underwriting formula, to determine how much you’ll have to pay as a deposit to open your account.

Deposits usually begin at $200 but can be up to $1,000 if you’re looking for a larger line of credit. The amount of credit you get is typically equal to the deposit you’ve paid for six months to one year after opening the account.

For example, if you open a secured card with a $500 deposit, you will only be extended $500 worth of credit until you have built up a history of on-time payments. After this introductory period, the credit card company will reassess your payment history. They may offer to transfer your card into an unsecured account, refund your deposit, and extend your line of credit.

- No Credit History

Step 3: Register for the Extra Debit Card

When you want to avoid credit cards, there is an alternative. The Extra Debit Card works like a secured credit card, but it connects directly to your bank account. When you use the Extra Card, it pays for the transaction and reconciles it using your bank account.

You get rewards points for each purchase, and the card reports to the credit bureau once a month. You are both building your credit and enjoying the perks of a credit card at the same time.

Now that you’ve built your credit, you can obtain credit cards that will expand your spending power.

Final Thoughts

A credit card is a great financial tool that, when used responsibly, can help you budget more effectively and make larger purchases. It’s not difficult to get started building credit, but you’ll want to make sure the credit profile you are building is positive. Bad credit is more difficult to fix than an empty credit portfolio.

Making the minimum payments in a timely manner on all of your accounts, avoiding overexerting your spending, and keeping low balances on your cards are all great strategies to build credit quickly and be approved for higher and additional lines of credit.

About Sarah Horvath

Sarah is an expert in the insurance, investing for retirement and cryptocurrency space.