SECTIONS

Is CVIM safe? | Why South America? | Investment objective | AdvantagesPast performance | The bottom line | What to do next

Covestor offers a managed South-American stock portfolio with a $5K minimum investment, at a competitive cost

Covestor® Investment Management (CVIM) provides an approach to money management that was previously only available to high-net-worth customers. At their platform, a retail investor can select model stock portfolios that are crafted by proven investors (the model publishers), and have their trades be automatically mirrored in her or his own brokerage account. This empowers these customers with easy and cost-effective access to portfolio management based on the decisions of experienced individuals and registered investment advisors (RIA) of their choice, while they enjoy the transparency of the system and its community-like experience.

I am Andy Djordjalian, publisher of a South-American model at CVIM. In this article I will present you this model that, I believe, is an informed way to invest in Brazilian stock, as well as equity from other South-American countries. Please have in consideration that Covestor pays me a fee for each client that subscribes to this model. This page is for informational purposes only, all the disclaimers on the model's profile page apply, and please take appropriate professional advice in any investment decisions.

Is it safe to invest with CVIM?

Several facts support Covestor's claims regarding the transparency and responsibility of their service. An SEC-registered investment advisor themselves, they provide professional personalized advise to each customer, granting them access only to portfolios considered suitable for them. The company manages the mirroring process and summarizes each portfolio's data on individual profile pages. Stocks that trade in low volume, or have a market capitalization that is too small, are excluded from the system as an additional measure of protection. These mechanisms are further explained on CVIM's website and are commented on the extensive coverage that the company has received, with articles in Wall Street Journal, Barron's, Investment News, Financial Times, Wall Street & Technology, Business Wire, MarketWatch and other publications.

The trades that are executed in the customers accounts are those that the model publishers perform in their own brokerage accounts (though some trades are not replicated, as explained at CVIM's website). Publishers have their own money at stake in those accounts, and they are also putting their reputation in play. I have worked hard to achieve good past performance in terms of return and volatility. That history brings trust to my model, so I would not like to lose it as much as I would not like to lose money from my account.

Regarding the assets, each customer's shares are held in their own brokerage accounts with well-known brokers like Interactive Brokers and TD Ameritrade. You can verify that Covestor is properly regulated by using this tool and you can check the same for the brokerage firms with the use of this other one.

Why South America?

Image courtesy of NASA

Latin America is one of the most developing regions in the world. Rich in resources, with mature financial institutions, political stability and a thriving middle class, Brazil and much of the rest of South America have excelled financially in recent years. The region produces commodities that are in high demand because of the industrialization and urbanization of Asian emerging economies, like metals (e.g., iron ore, copper, zinc, silver, tantalum, palladium and lithium), petroleum and grains. As a consequence, it is receiving large inflows of capital. Foreign reserves at the Central Banks have been enlarged thanks to these, which, combined with a more responsible fiscal policy, configure a financial outlook that differs significantly from the crisis and debt problems of the past.

The Brazilian and South American potential is not limited to commodity exports driven by Chinese and Indian economies. The region has considerable domestic consumption, more per capita than average in emerging markets. Moreover, the consuming middle class is growing, thanks to the commodity boom and to the process of social change that these countries have been undergoing for many years. In addition, it has reserves of gold and other precious metals, plus some emerging world-class exports with significant value added. For example, aircraft from Brazil's Embraer, which has recently become the third-largest producer in the world in terms of yearly delivery, and wine from Argentina and Chile, countries that are its fifth and ninth producers, respectively. Thanks to these various opportunities for profit, investments in the region can be diversified.

Many renowned economists and investors recommend that US individuals have larger allocations in emerging markets, especially resource-rich ones. For example, Princeton's Burton Malkiel, author of one of the most influential investing books ever, A Random Walk Down Wall Street, in the following video from CBS MoneyWatch:

For these reasons, I believe that Brazilian stock, combined with equity from other countries in South America, are excellent components for the portfolios of US and global investors, that can spice those investments up with profit potential and diversification. I have lived in Argentina all my life, immersed in the regional environment and following business publications in Spanish and Portuguese for many years. When the people at Covestor invited me to publish a South American model, I agreed that it may result in an interesting product for their clients, and accepted. We started the South America Focus model in early December of 2009, and it has been working comparatively well since.

Investment objective

The model provides a means for U.S. citizens, and foreigners with accounts in the U.S., to invest in South America, because it is composed of ADR's that correspond to South-American stocks, plus stock traded in those exchanges that are not ADR's but belong to companies that have a majority of their operations in South America, plus Latin-America ETF's and closed-end funds (CEF's). All of these are traded in U.S. exchanges (i.e., NYSE, NYSE Arca and NASDAQ). The resulting portfolio is an alternative to state-of-the-art Latin-American investment vehicles, with their positive aspects but also some differences that are, hopefully, improvements. By “state-of-the-art vehicles”, I mean top Latin America mutual funds like Fidelity Latin America (FLATX), T. Rowe Price Latin America (PRLAX) and BlackRock Latin America (MDLTX), the largest Latin America ETF iShares S&P Latin America 40 Index (ILF), and the top Brazil ETF's iShares MSCI Brazil Index (EWZ) and Market Vectors Brazil Small-Cap ETF (BRF). These six funds add up to more than $20 billion in assets and are leading products for investors interested in the region.

The CVIM system has a critical advantage over those funds: the possibility to trade more flexibly. Successful funds manage so much money that their trading costs are quite high, unless they trade very liquid securities or do it in small portions. With the CVIM system we are much less restrained, because the assets of each model's subscribers do not add up to hundreds of millions of dollars.

My model is diversified, I do not trade very often and I stay fully invested as much as possible

That advantage creates opportunities. Some publishers at CVIM use it to offer interesting, speculative portfolios, focused on small caps, long and short, etc. But I decided to adopt a lower-risk approach, combining this flexibility with a good level of diversification, in an attempt to obtain a result that is somewhat better than that of the aforementioned state-of-the-art funds. I think a small outperformance is a healthy objective, because accumulated over time it can make a big difference, without having to resort to risk taking and good luck as much as more speculative investments require. The South-American theme offers enough profit potential by itself, there is no need to focus on few stock. Therefore, my model is diversified, I do not trade very often and I stay fully invested as much as possible and long only (meaning that I don't bet on shares going down, for the reasons explained in this four-part article).

Advantages

I will try to summarize the differences — hopefully, advantages — that South America Focus has compared to the portfolios of Latin America and Brazil ETF's and mutual funds:

Weighting based on top-down analysis, not constrained by market caps. To alleviate their trading costs, most big funds have the greater part of their portfolios in liquid companies with high market capitalizations. That often leads to questionable levels of diversification. For example, iShares MSCI Brazil Index (EWZ), the largest Brazil ETF, has currently a 37% of its portfolio tied to only two companies, Petroleo Brasilero (Petrobr?s) and Vale. Even though these are good companies that have done well, a Brazilian investment can be diversified much better. Moreover, let's consider that, when people pay fees for a passive fund instead of buying shares from a few companies, they do it to obtain diversification. I wonder if all of EWZ's investors are aware of the real value they are getting in exchange for the fees they pay. . .

Without going to that extreme, the big Latin-American stock funds are also heavily biased towards market-cap weighting. For example, Morningstar currently reports that FLATX, PRLAX, MDLTX and ILF have just a 13.4%, 8.5%, 6.7% and 15.8%, respectively, in stock from countries other than Brazil and Mexico (EWZ and BRF are Brazil-only funds), despite the profit and diversification potential offered by those other countries.

The CVIM system has a critical advantage over those funds: the possibility to trade more flexibly

For South America Focus, weighting is decided after a top-down analysis that uses market caps as one of many elements. Brazil is still dominant, and I give much consideration to Petrobr?s and Vale, but I aim at obtaining better diversification by making more extensive use of stock from other countries and from less-capitalized companies.

A fixed-income allocation. To diversify more, I allocate about a 15% to 20% of the model in fixed-income instruments. Emerging-market bonds have performed very well in the past decade, and even though the developing countries are in relatively-good financial standing, they are still paying higher interest than developed economies.

Closed-end funds (CEFs). I use CEFs for the fixed-income allocation (there are none for South-American debt only, so I use emerging-market debt funds, which have a portion of their portfolios in South-American bonds). As with all CEF investments, there is an additional potential for profit besides the increase in value of the underlying assets per share (also called Net Asset Value or NAV), which is the improvement of their market price relative to their NAV. With open-ended funds, like mutual funds and ETF's, the market price and the NAV are about equal all the time, but with CEFs they are not, which constitutes an additional opportunity to buy low and sell high.

Junior mining. Several junior mining-exploration companies, that search for precious and industrial metals, operate in Latin America, but they are not held by big funds because they are incorporated elsewhere and trade in volumes that are not large enough for them. South America Focus does include them. About a 9% of the portfolio is currently assigned to Canadian junior explorers, plus an 8% that is allocated to a larger miner from the same country. These holdings are an opportunity for profits and diversification that is absent in the funds mentioned before.

It is not necessarily an advantage, but Mexico is not included. The model covers South America only. Therefore, although it is not a one-country instrument like EWZ and BRF, it does not include Mexico like the Latin-America funds.

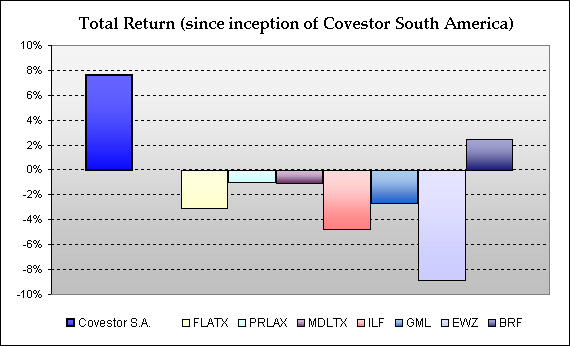

Past performance

This figure shows the performance of the first six months of the model portfolio, from December 3, 2009 to the day of this writing, June 3, 2010. It is compared to the top Latin-American mutual funds and ETF's that were mentioned before, displaying a noticeable outperformance. It has not been a good period at all for Latin-American equity, particularly for the Brazilian stock market (represented by EWZ and BRF). These funds lost between a 9.6% and a 16.1% of their original value, while our model lost very little.

Even though the model is more conservative than the other funds, it is not much so, and it has also over-performed during some positive periods included in these 6 months. Since early December it has been fully invested, with the exception of a very small cash allocation and occasional to-be-credited cash. Therefore, this result is not explained by excessive conservatism or lucky timing — the aforementioned advantages are a better explanation.

In future articles we will compare risk metrics and quarterly results, please subscribe to receive those updates in your email or news reader.

The reported performance of the CVIM portfolio was taken from its profile page, which does not include the fees collected by Covestor (1.50% annually) and the trading fees (which, as far as I know, are currently $1 per transaction on Interactive Brokers accounts or $8 with TD Ameritrade). It currently requires 15 purchases to enter the model and, besides those, we have been having 3.4 transactions per month, which should be about normal. BlackRock Latin America (MDLTX) has a 5.25% front load that has not been deducted from its return in the graph. Performance data for the funds were obtained from Morningstar and Yahoo Finance. For more information, you may visit the CVIM profile page. Please bear in mind that past performance is no guarantee of future results, and that this is just a 6-month comparison.

The bottom line

Portfolios offered through the CVIM system can have more flexible trading than big mutual funds and ETF's. This South-American portfolio makes use of that advantage, to reduce risk by better diversification, and to try to exploit mispricing that, presumably, occurs in some stocks that are not traded in massive volume, such as fixed-income closed-end funds and junior-mining shares.

For example, if we were to favor large-cap companies incorporated in Latin America as much as the regional mutual funds and ETF's do, we would have few choices to invest in precious-metal producers. Only Peruvian Minas Buenaventura (BVN) is worth mentioning, Latin-America funds typically have a 1% to 2% of their portfolios in this company. But it is disadvantageous to have so little and through only one company, because there is more precious-metal mining in Latin America and these companies are good diversifiers. On South America Focus, we are currently holding some Canadian miners that operate in the region, exploring for, and producing, precious and industrial metals. Namely, Silver Standard Resources (SSRI), Exeter Resource Corp. (XRA) and Solitario Exploration & Royalty (XPL). This allocation was created for its diversification potential, and it has been useful as such during the past months, explaining much of the outperformance of the model compared to its benchmarks.

MORE ABOUT SOUTH AMERICA FOCUS

If large-cap shares like the ones typically included in the big funds, like heavyweights Petr?leo Brasilero (PBR) and Vale (VALE), soar and outperform the allocations we have for diversification purposes, then those funds will probably return more than our portfolio. But in many probable scenarios, our model may offer better, more stable, returns. That makes it a good vehicle to invest in one of the most developing regions of the world, and to add diversification and profit potential to a U.S. or global investment portfolio, and this claim is supported by the first 6 months of history of the model, that have just elapsed as I am writing this.

What to do next

If you are interested, you can visit Covestor Investment Management and, particularly, this model's profile page at their site. Consider opening an account with them, there are many other models to subscribe to. This variety can be used to assemble a diversified investment that covers various themes.

Thank you for your interest. I wish you the best in your pursuit of financial success!

“Invest in Brazilian & Latin-American Stocks with Covestor Investment Management” was originally published at SimpleStockInvesting.com.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.