A few months ago, I tagged along with my wife and daughter as they went on a tour of the Federal Reserve Building in downtown New York. While the highlight of the tour is that you get to see large stacks of US dollars in the basement of the building, I considered making myself persona non grata with my immediate family by asking the guide (a very nice Fed employee) about the location of the interest rate room.

That, of course, is the room where Janet Yellen comes in every morning and sets interest rates.

I am sure that you can visualize her pulling the levers that sets T.Bond rates, mortgage rates and corporate rates and the power that comes with that act. If that sounds over the top, that is the impression you are left with, not only from reading news stories about central banks, but also from opinion pieces from some economists and investment advisors. I know that investors, analysts and CFOs are all rendered off balance by low interest rates, but I will argue that the techniques that they use to compensate are more likely to get them in trouble than solve their problems.

The what: Interest rates are at historic lows across the globe

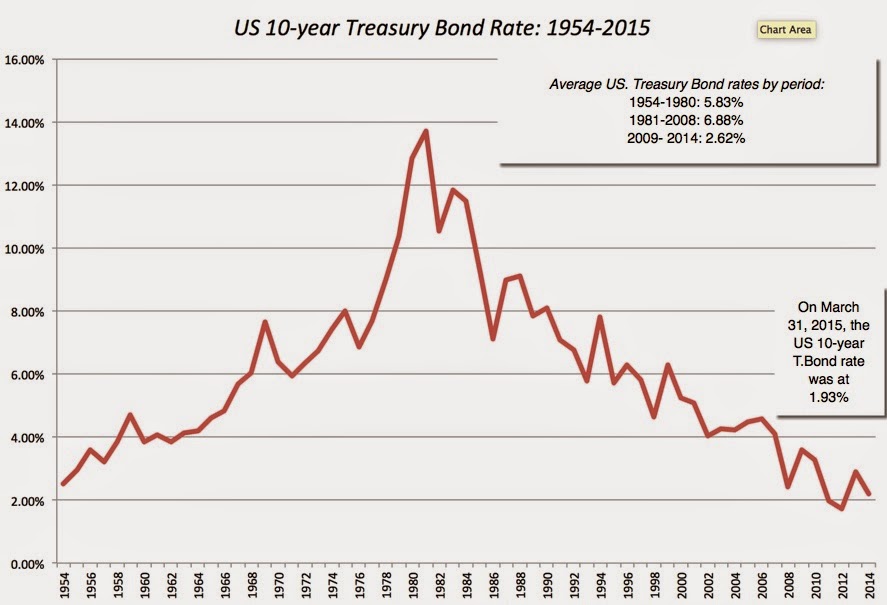

There is little to debate. Interest rates are lower than they have been in a generation and you can see it in this graph of the US 10-year treasury bond rate going back several decades:

|

| US 10-year T.Bond rates at the end of each year |

|

| Ten-year Government Bond Rates: End of each period |

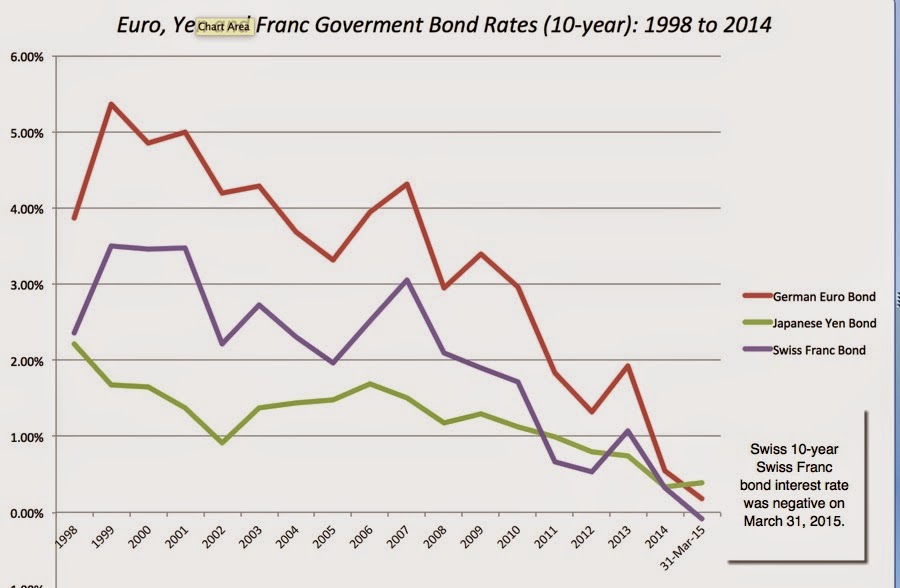

In fact, on the Swiss Franc, the 10-year bond rates rates have not just dropped but have hit zero and kept going to -0.09%, leading to the almost unfathomable phenomenon of negative interest rates on long term borrowing.

A world where savers have to pay banks to keep their savings and borrowers are paid money to borrow turns everything that we have learned in economics on its head and it is therefore no surprise that even seasoned investors and analysts are unsure of what to do next.

The why: Its not just central banks

The Fundamentals

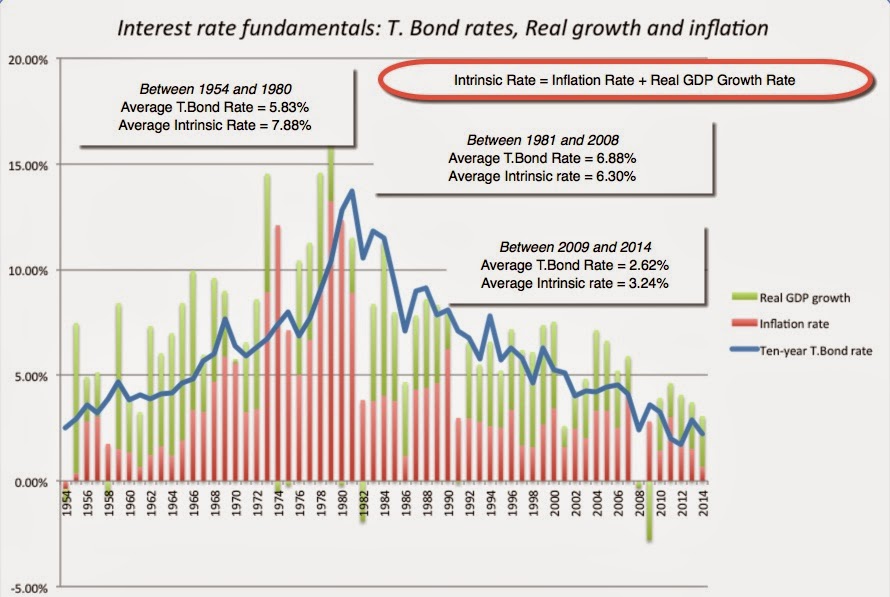

Interest rate on a guaranteed investment = Expected inflation + Expected real interest rate

This is the simplified version of the classic Fisher equation and it is true by construction. In fact, many analysts use it to decompose market interest rates; thus if the US treasury bond rate is at 2.00% and expected inflation is 1.25%, the real interest rate is backed out at 0.75%. In the long term, I would argue that a real interest rate has to be backed up by a real growth rate in the economy.

After all, you cannot deliver a 2% real interest rate in an economy growing at only 1% a year in the long term, though you can get short term deviations between the two numbers. Thus, in the long term, the interest rate on a guaranteed investment can be rewritten as:

Interest rate on a guaranteed investment = Expected inflation + Expected real growth rate

How well does this simplistic equation hold up in practice? Testing it is hard, especially when you can observe only actual inflation and real growth but not expected inflation and real growth. However, we also know that expectations for inflation and real growth are driven, for better or worse, by recent history; thus expected inflation increases after periods of high inflation and decreases after periods of low inflation, thus making actual inflation and real growth reasonable proxies for expected values.

The final number we need to test out this relationship is the interest rate on a guaranteed investment, and we use the US 10-year treasury bond rate as the stand in for that number, with the concession that the last 5 years have shaken investor faith in the guarantee.

|

| Source: FRED (Federal Reserve in St. Louis) |

Even if you take issue with my proxies for expected inflation (the actual inflation rate in the US each year, as measured by the CPI), real growth (the real growth rate in US GDP and the interest rate on a guaranteed investment, the graph sends a powerful message that risk free rates are driven by inflation and real growth expectations.

If expected inflation is low and real growth is anemic, as has been the case since 2008, interest rates will be low as well and they would have been low, with or without central bank intervention.

The Central Bank Effect

|

| Source: FRED |

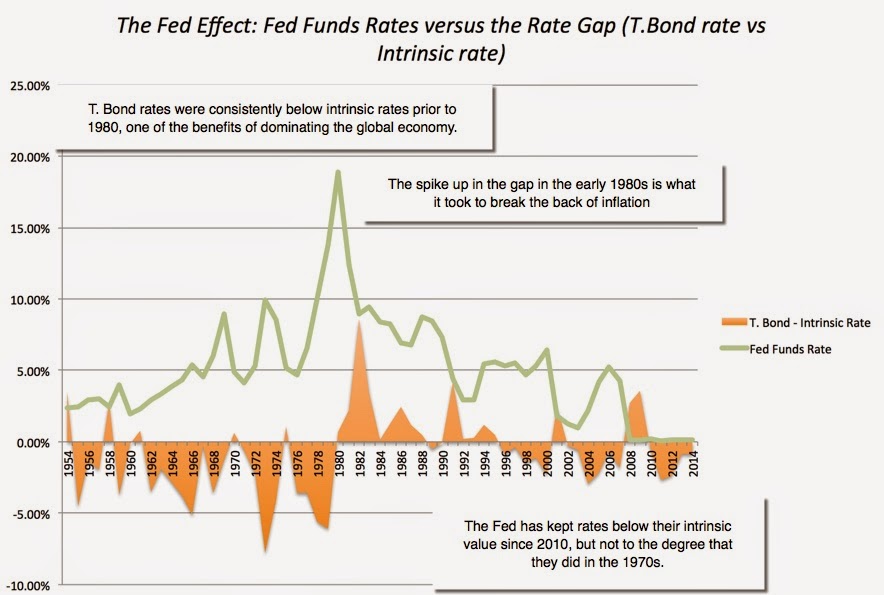

Note that the Fed Funds rate hit zero in 2009 and has stayed there for the last five years, effectively eliminating it as a tool for controlling rates.

Perhaps driven by desperation and partly motivated by the savior complex, the Fed has turned to a relatively unused tool in its arsenal and bought large quantities of US treasury bond in the market for the last five years, the much-talked about Quantitative Easing (QE). While it is true that T.Bond rates have stayed below intrinsic interest rates over the last 5 years, the effect of QE (at least to my eyes) seems to modest.

As the economy comes back to life, all eyes have turned towards Janet Yellen and the Fed and Fed-watching has become the central focus for many investors. While that is understandable, it is worth remembering that in today's economic environment, with low inflation and real growth, the removal of the Fed prop will not cause interest rates to pop to 5% or 6%.

In fact, based upon the numbers in the most recent year, the intrinsic interest rate is 3.08% and if the central banking props disappear, that would be the number towards which US treasury bond rates move.

Given the evidence to the contrary, it is puzzling that investors continue to hold on to the belief that central banks set interest rates and can change them on whim, but I think that the delusion serves both sides (investors and central banks) well. Investors, whipsawed by market and economic forces that are uncontrollable, feel comfort in attributing the power to set interest rates to central banks.

It also allows investors to attribute every phenomenon that they have trouble explaining to central banking machinations and interest rates that are either "too high" or "too low".

Quantitative Easing in all its forms has proved to be absolutely indispensable as a bogey man that you can blame for the failure of active investing, the rise and fall of gold, and bubbles of every type. Central banks, which are really more akin to the Wizard of Oz, in their powers, than Masters of the Universe, are glad to play along, since their power comes from the illusion that they have real power.

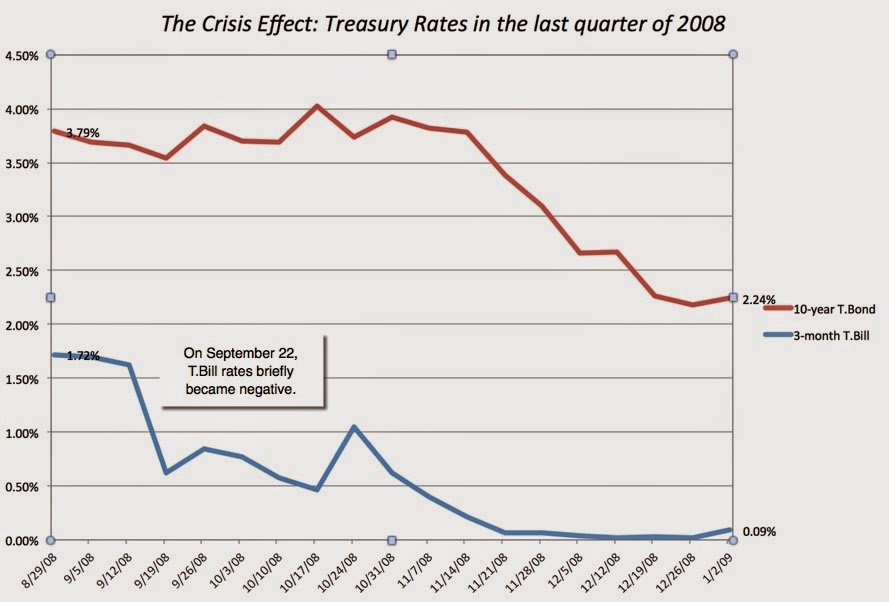

The Crisis Effect

There is another factor at play that may be more powerful than central banks, at least over short periods, and that is the perception of a crisis. Whatever the origins or form of the crisis, investors respond with fear, and flee to safety. That "flight to quality" often manifests itself in declining interest rates on bonds issued by governments that are perceived as "higher quality", and may push those rates well below intrinsic levels.

Looking at the chart where we outline the gap between the T.Bond rate and its intrinsic value, the quarter where we saw the US 10-year treasury bond rate drop the most, relative to its intrinsic value, was the last quarter of 2008, where the crisis in financial markets led to a rush into US treasuries. That translated into a precipitous drop in treasury rates across the board, with the 10-year rate dropping from 3.66% on September 12, 2008, to 2.2% at the end of 2008, and the T. Bill rate declining from 1.62% to 0.02% over the same period.

|

| Source: FRED- Constant Maturity Rates on 3-month and 10-year treasuries |

One of the few constants over the last six years has been that we lurch from one crisis to another, with local problems quickly going global. While there are some who may argue that this is a passing phase, I believe that this is part and parcel of globalization, one of the negatives that need to get offset against its positives.

As economies and markets become increasingly interconnected, I think that the recurring crisis mode will be a permanent feature of market. One consequence of that may be that market interest rates on government bonds will settle below their intrinsic values, a permanent "crisis discount", with or without central banking intervention.

The Interest Rate Effect

Expected Return (r) = Interest rate on a risk free investment + Risk Premium

That expected return then determines what we will be willing to pay for a risky asset, with lower expected returns translating into higher prices.

For businesses, these expected return becomes hurdle rates (costs of equity and capital) that they use to decide not only whether and where they should invest their money but plays a role in how much they borrow and how much to return to stockholders (as dividends or buybacks).

If the risk free rate drops and you leave the risk premiums and cash flows unchanged, the effect on value is unambiguously positive, with value rising as risk free rates drop.

Thus, if you have a business that has $100 million in expected cash flows next year, with a growth rate of 4% a year in perpetuity and an equity risk premium of 4%, changing the risk free rate from 6% down to 2% will have profound effects on value. It is this value effect that has led some to blame the Fed for creating a "stock market bubble" and analysts across the world to wonder whether they should be doing something to counter that effect, in their search for intrinsic value.

While the mathematics that show the link between value and interest rates is simple, it is misleading because it does not tell the whole story. As I argued in the last section, interest rate movements, up or down, almost never happen in a vacuum.

The same forces that cause significant shifts in interest rates affect other inputs into the valuation and those changes can reduce or even reverse the interest rate effect:

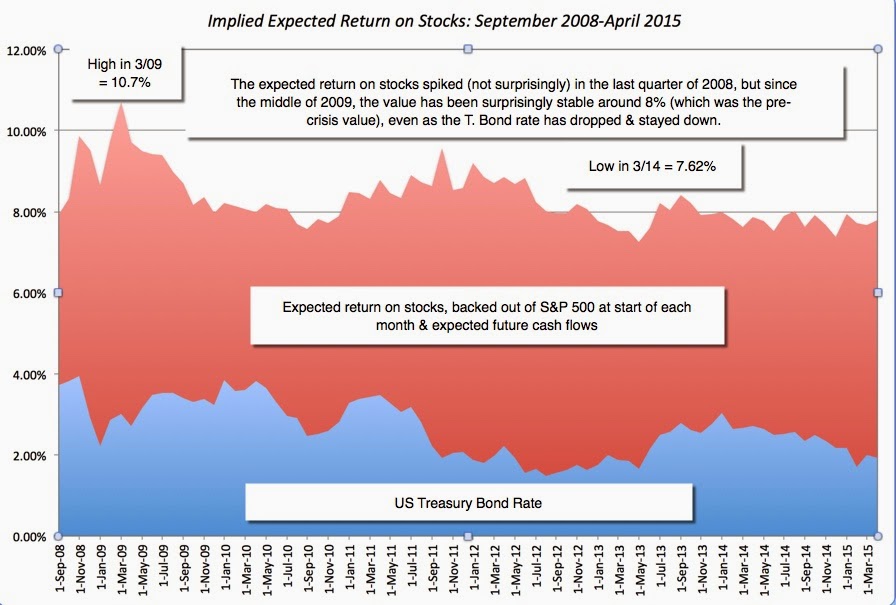

To illustrate, the 2008 crisis that caused the T.Bond rate to plummet in the last quarter of the year also caused equity risk premiums to surge from 4.37% on September 12, 2008 to 6.43% on December 31, 2008. In the figure below, I back out the expected return on stocks and the equity risk premium from the index level each day and the expected future cash flows for each month from September 2008 to April 2015. Note that the cost of equity for the median US company rose in the last quarter of 2008, even as risk free rates declined.

|

| Source: Damodaran.com (Implied ERP) |

The expected return on equities has stayed surprisingly stable (around 8%) for much of the last 5 years, nullifying the impact of lower interest rates and casting doubt on the "Fed Bubble" story. As the crisis has receded, investor concerns have shifted to real growth, as the developed market economies (US, Euro Zone and Japan) have been slow to recover and inflation has not only stayed tame but turned to deflation in the EU and Japan. Thus, looking just at lower interest rates and making judgments on value misses the big picture.

Reacting to Low Interest Rates

Given that low interest rates have shaken up the equation, what should we do to respond? Broadly speaking, there are four responses to low interest rates:

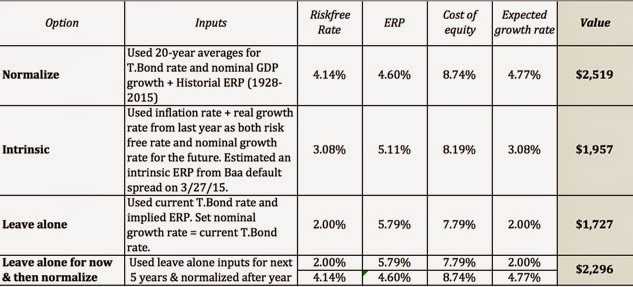

- Normalize: In valuation, it is common practice to replace unusual numbers (earnings, capital expenditures and working capital) with more normalized values. Some analysts extend that lesson to risk free rates, replacing today's "too low" rates with more normalized values. While I understand the impulse, I think it is dangerous for three reasons.

- The first is that "normal" is a subjective judgment. I argue, only half in jest, that you can tell how long an analyst has been in markets by looking at what he or she views as a normal riskfree rate, since normal requires a time frame and the longer that time frame, the higher normal interest rates become. The second is that if you decide to normalize the risk free rate, you have no choice but to normalize all your other macro variables as well.

- Consequently, you have to replace today's equity risk premium with the premium that fits best with your normalized risk free rate and do the same with growth rates. Put differently, if you want to act like it is 2007, 1997 or 1987, when estimating the risk free rate, your risk premiums and growth rates will have to be adjusted accordingly.

- The third is that unlike earnings, cash flows or other company-specific variables, where you are free to make your judgment calls, the risk free rate is what you can earn on your money today, if you don't invest in risky assets. Consequently, if you do your valuation, using a normalized risk free rate of 4% (instead of the actual risk free rate of 2%), and decide that stocks are over valued, I wish you the very best of luck putting your money in that normalized treasury bond, since it exists only in your estimation.

- Go intrinsic: The second option, if you believe that the market interest rate on government bonds is being skewed by central banking action to abnormally low or high levels is to replace that rate with an intrinsic interest rate. If you buy into my estimates for inflation and real growth in the last section, that would translate into using a 3.08% "intrinsic" US treasury bond rate.

- To preserve consistency, you should continue to use the same inflation rate and real growth as your basis for forecasting earnings and cash flow growth in your company and going the distance, you should estimate an intrinsic ERP, perhaps tying it to fundamentals.

- Leave it alone: The third option is to leave the risk free rate at its current levels, notwithstanding concerns that you might have about it being too low or too high. To keep your valuation in balance, though, your other inputs have to be consistent with that risk free rate. That implies using forward-looking prices for risk (equity risk premiums and default spreads) that reflect the market today and economy-wide growth and inflation rates that are consistent with the current risk free rate.

- Thus, if you decide to use 0.21% as the risk free rate in Euros, the combination of inflation and real growth rates you have to assume in the Euro economy have to combine to be less than 0.21%. Doing so does not imply that you believe that nominal growth will be that low but ensures that you are making the same assumptions about nominal growth in the numerator (cash flows) as you are in the denominator (through the risk free rate).

- Leave it alone (for now) : The last option is to leave the risk free rate at current levels for now but adjust the rate in the future (perhaps at the end of your high growth period) to your normalized or intrinsic levels. Here again, the key is to make sure that your other valuation inputs are consistent with your assumption.

- Thus, for the period you use the current risk free rate, you have to use equity risk premiums, growth rates and inflation expectations consistent with that rate, and as you adjust the risk free rate to its normalized or intrinsic levels, you have to adjust the rest of your inputs.

To illustrate the four options when it comes to risk free rates, I value a hypothetical average-risk company with an expected cash flow of $100 million next year, using all four options. The inputs I use for the company under each option are summarized below, with the value computed in the last column:

The four choices yield different values but the most interesting finding is that the value that I get with the "leave alone" option is lower than the values that I obtain with my other options. Consequently, those who argue that we need to replace the current risk free rate with more normalized versions because it is the "conservative" path may be ending up with estimates of value that are too high (not too low).

Note that while each input into these mismatched valuations may be defensible, it is the combination that skews the value vastly downwards or upwards. If you use or do intrinsic valuations, checking for input consistency is more critical than ever before.

Bottom line

So, what is the bottom line? Like almost everyone else, I find myself in uncharted territory, with interest rates approaching zero in many currencies and like most others, I feel the urge to "fix" the problem.

There are three broad lessons that I take away from looking at the data.

Central banks tweak interest rates. They don't set them. Consequently, I am going to spend less time worrying about what Janet Yellen does in the interest rate room and more on the fundamentals that drive rates. I will also grant short shrift to anyone who uses central banks as either an excuse or looks to them as a savior in their investing.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Comments

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.