As the NASDAQ approaches historic highs, Apple's market cap exceeds that of the Bovespa (the Brazilian equity index) and young social media companies like Snapchat have nosebleed valuations, there is talk of a tech bubble again. It is human nature to group or classify individuals or entities and assign common characteristics to the group and we tend to do the same, when investing. Specifically, we categorize stocks into sectors or groups and assume that many or most stocks in each group share commonalities. Thus, we assume that utility stocks have little growth and pay large dividends and commodity and cyclical stocks have volatile earnings largely because of macroeconomic factors. With "tech" stocks, the common characteristics that come to mind for many investors are high growth, high risk and low cash payout. While that would have been true for the typical tech stock in the 1980s, is it still true? More specifically, what does the typical tech company look like, how is it priced and is its pricing put it in a bubble? As I hope to argue in the section below, the answers depend upon which segment of the tech sector you look at.

A Short History of Tech Stocks

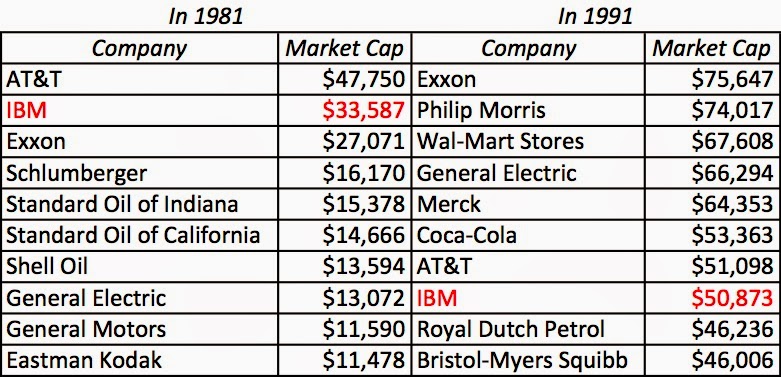

My first foray into investing was in the early 1980s, as the market started its long bull market run that lasted for almost two decades. In 1981, the technology stocks in the market were mainframe computer manufacturers, led by IBM and a group of smaller companies lumped together as the seven dwarves (Burroughs, Univac, NCR, Honeywell etc.). Not only were they collectively a small proportion of the entire market, but of the list of top ten companies, in market capitalization terms, in 1981, only one (IBM) could have been categorized as a technology stock (though GE had a small stake in computer-related businesses then):

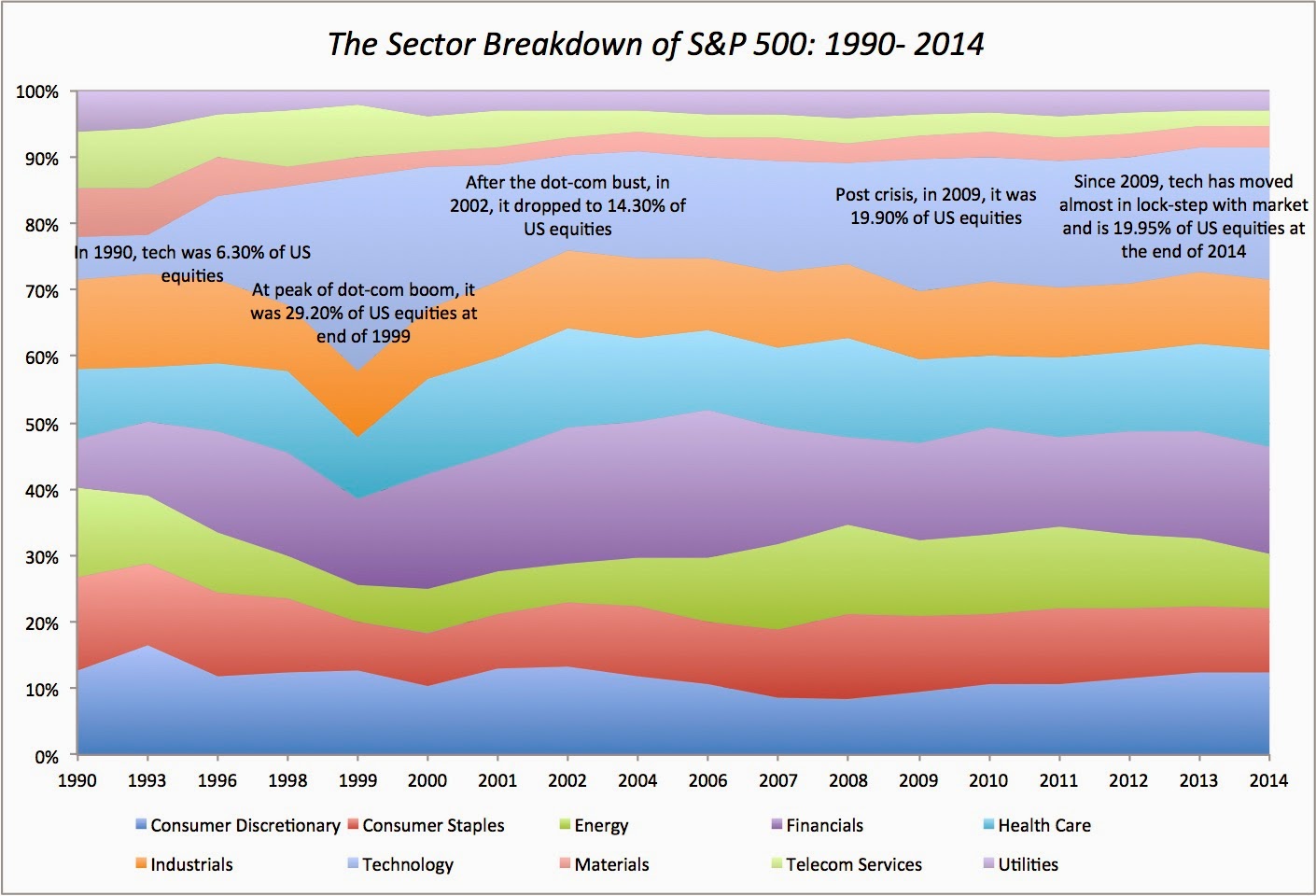

During the 1980s, the personal computer revolution created a new wave of technology companies and while IBM fell from grace, companies catering to the PC business such as Microsoft, Compaq and Dell rose up the market cap ranks. By 1991, the top ten stocks still included only one technology company, IBM, and it had slipped in the rankings. However even in 1991, technology stocks remained a small portion of the market, comprising less than 7% of the S&P 500. During the 1990s, the dot-com boom created a surge in technology companies and their valuations, and while the busting of that boom in 2000 caused a reassessment, technology has become a larger piece of the overall market, as evidenced by this graph that describes the breakdown, by sector, for the S&P 500 from 1991 to 2014:

|

| Market Capitalization at the end of each year (S&P Capital IQ) |

There are two things to note in this graph.

- The first is that technology as a percentage of the market has remained stable since 2009, which calls into question the notion that technology stocks have powered the bull market of the last five years.

- The second is that technology is now the largest single slice of the equity market in the United States and close to the second largest in the global market. So what? Just as growth becomes more difficult for a company as it gets larger and becomes a larger part of the economy, technology collectively is running into a scaling problem, where its growth rate is converging on the growth rate for the economy. While this convergence is sometimes obscured by the focus on earnings per share growth, the growth rate in revenues at technology companies collectively has been moving towards the growth rate of the economy.

The Diversity of Technology

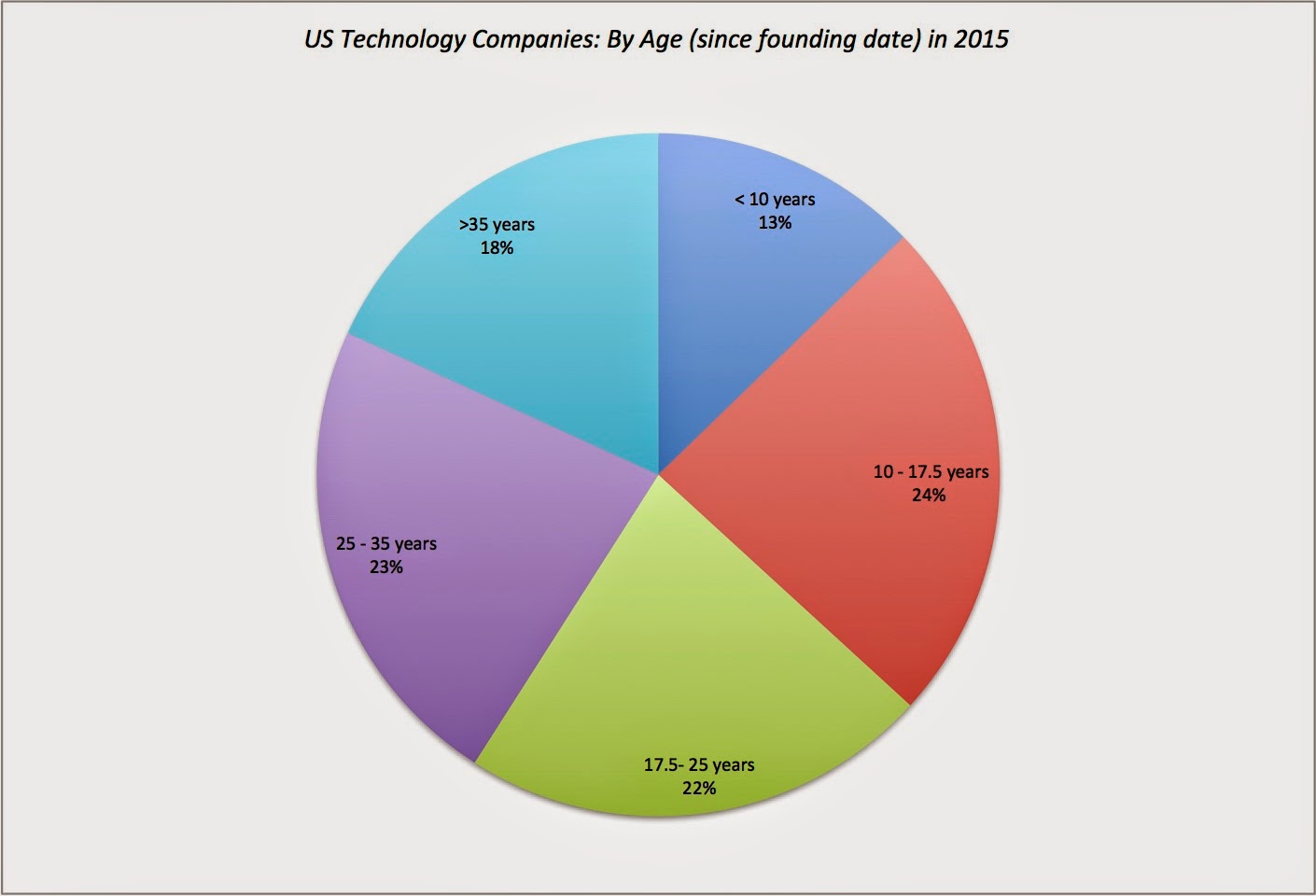

As technology ages and becomes a larger part of the economy, a second phenomenon is occurring. Companies within the sector are becoming much more heterogeneous not only in the businesses that they operate in, but also in their growth and operating characteristics. To see these differences, let's start by looking at the sector and its composition in terms of age at the start of 2015. In February 2015, there were 2816 firms that were classified as technology companies, just in the United States, accounting for 31.7% for all publicly traded companies in the US market. Some of these companies have been listed for only a few years but others have been around for decades. Using the year of their founding as the birth year, I estimated the age for each company and came up with the following breakdown of tech stocks, by age:

|

| Age: Number of years from founding of company to 2015 |

Note that 341 technology companies have been in existence for more than 35 years and an additional 427 firms have been in existence between 25 and 35 years, and they collectively comprise about 41% of the firms that we had founding years available in the database. While being in existence more than 25 years may sound unexceptional, given that there are manufacturing and consumer product companies that have been around a century or longer, tech companies age in dog years, as the life cycles tend to be more intense and compressed. Put differently, IBM may not be as old as Coca Cola in calendar time but it is a corporate Methuselah, in tech years.

The Pricing of Technology

The speedy rise of social media companies like Facebook, Twitter and Linkedin from nothing to large market cap companies, priced richly relative to revenues and earnings, has led some to the conclusion that this rich pricing must be across the entire sector. To see if this is true, I look at common pricing metrics across companies in the technology sector, broken down by age.

|

| Pricing as of February 2015, Trailing 12 month values for earnings and book value |

To adjust for the fact that cash holdings at some companies are substantial, I computed a non-cash PE, by netting cash out of the market capitalization and the income from cash holdings from the net income. While it is true that the youngest tech companies look highly priced, the pricing becomes more reasonable, as you look across the age scale. For instance, while the youngest companies in the tech sector trade at 4.34 times revenues (based upon enterprise value), the oldest companies trade at 2.44 times revenues.

How do tech companies measure up against non-tech companies? After all, any story that is built on the presumption that tech companies are the sources of a market bubble has to backed up by data that indicates that tech companies are over priced relative to the rest of the market. To answer this question, I looked at the youngest (<10 and="" companies="" oldest="" tech="" years="">35 years) relative to the youngest (<10 and="" companies:="" div="" non-tech="" oldest="" years="">

</10></10>

|

| Based on February 2015 Pricing & Trailing 12 month numbers: 2807 US technology and 6076 non-technology companies. |

The assessment depends upon what part of the technology sector you are focused on. While the youngest tech companies trade at much higher multiples of revenues, earnings and book value than the rest of the market, the oldest tech companies actually look under priced (rather than over priced) relative to both the rest of the market and to the oldest non-tech companies. In fact, even focusing just on the youngest companies, it is interesting that while young tech companies trade at higher multiples of earnings (EBITDA, for instance) than young non-tech companies, the difference is negligible if you add back R&D, an expense that accountants mis-categorize as an operating expense.

Does this mean that you should be selling your young tech companies and buying old tech companies? I am not quite ready to make that leap yet, because the differences in these pricing multiples can be partially or fully explained by differences in fundamentals, i.e., young tech companies may be highly priced because they have high growth and old tech companies may trade at lower multiples because they have more risk and tech companies collectively may differ fundamentally from non-tech companies.

The Fundamentals of Tech Companies

There are three key fundamentals that determine value: the cash flows that you generate from your existing assets, the value generated by expected growth in these cash flows and the risk in these cash flows. Again, rather than look at tech stocks collectively, I will break them down by age and compare them to non-tech stocks.

a. Cash Flows and Profitability

To measure profitability, I looked at two statistics, the percentage of money making companies in each group and the aggregate profit margins (using EBITDA, operating income and net income):

Young technology companies are far more likely to be losing money and have lower profit margins that young non-technology companies, even if you capitalize R&D expenses and restate both operating and net income (which I did). At the other end of the spectrum, old technology companies are much more profitable, both in terms of margins and accounting returns, than old non-technology companies, adding to their investment allure, since they are also priced cheaper than non-technology companies.

b. Growth – Level and Quality

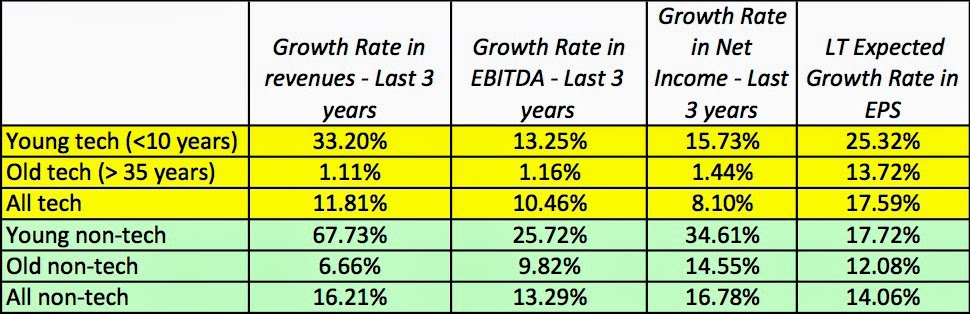

To test the conventional wisdom that technology companies have higher growth potential than non-technology companies, I looked at both past and expected future growth in different operating measures starting with revenues and working down the income statement:

The results are surprising and cut against the conventional wisdom, on most measures of growth. Young non-technology companies have grown both revenues and income faster than young technology companies, though analyst estimates of expected growth in earnings per share remains higher for young tech companies. With old tech companies, the contrast is jarring, with historic growth at anemic levels for technology companies but at much healthier levels for non-tech companies, perhaps explaining some of the lower pricing for the former. It is true, again, that the expected growth in earnings per share is higher at tech companies than non-tech companies, reflecting perhaps an optimistic bias on the part of analysts as well as more active share buyback programs at tech companies.

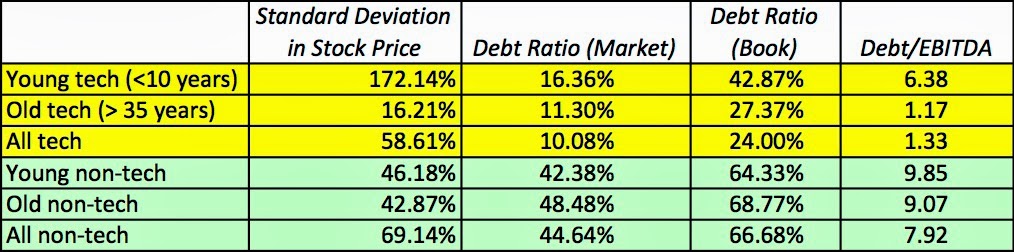

c. Risk – Financial and Market

Are tech companies riskier than non-tech companies? Again, the conventional wisdom would say they are, but I look at two measures of risk in the table below: standard deviation in stock prices and debt ratios across groups:

I get a split verdict, with much higher volatility in stock prices in tech companies, young and old, than non-tech companies, accompanied by much lower financial leverage at tech companies, again across the board, than non-tech companies. As we noted in the earlier table, young tech companies are more likely to be losing money and that may explain why they borrow less, but I think that the high price volatility has less to do with fundamentals and more to do with the fact the investors in young tech companies are too busy playing the price and momentum game to even think about fundamentals.

d. Cash Return – Dividends, Buybacks and FCFE

In the final comparison, I look at how much cash is being returned in the form of dividends and buybacks by companies in each group, as well as how much cash is being held back in the company as a percent of overall firm value (in market value terms):

|

| FCFE = Cash left over after taxes, debt payments and reinvestment; Firm value = Market Cap + Total Debt; Cash Return = Dividends + Buybacks - Stock Issues |

Note that both young tech and young non-tech companies have raised more new equity than they return in the form of dividends and buybacks, giving them a negative cash return yield. Old tech companies return more cash to stockholders both in dividends and collectively, with buybacks, than old non-tech companies. Finally, notwithstanding the attention paid to Apple's cash balance, old tech companies hold less cash than old non-tech companies do.

In summary, here is what the numbers are saying. Young technology companies are less profitable, have higher growth, higher price risk and are priced more richly than the young non-tech companies. Old technology companies are more profitable, have less top line growth and are priced more reasonably than old non-tech companies.

Bottom line

The size of the technology sector and the diversity of companies in the sector makes it difficult to categorize the entire sector. In my view, the data suggests that we should be doing the following:

- Truth in labeling: We are far too casual in our classifications of companies as being in technology. In my book, Tesla is an automobile company, Uber is a car service (or transportation) company and The Lending Club is a financial services company, and none of them should be categorized as technology companies. The fact that these firms use technology innovatively or to their advantage cannot be used as justification for treating them as technology companies, since technology is now part and parcel of even the most mundane businesses. Both companies and investors are complicit in this loose labeling, companies because they like the "technology" label, since it seems to release them from the obligation of explaining how much they need to invest to scale up, and investors, because it allows them to pay multiples of revenues or earnings that would be difficult (if not impossible) to justify in the actual businesses that these firms are in.

- Age classes: We should start classifying technology companies by age, perhaps in four groups: baby tech (start up), young tech (product/service generating revenues but not profits), middle-aged tech (profits generated on significant revenues) and old tech (low top line growth, though sometimes accompanied by high profitability), without any negative connotations to any of these groupings. If we want to point to mispricing, we should be specific about which group the mispricing is occurring. In this market, for instance, if there is a finger to be pointed towards a group, it is not technology collectively that looks like it is richly priced, but baby and young technology companies. By the same token, if you follow rigid value investing advice, where you are told to stay away from technology on the grounds that it is high growth, high risk and highly priced, that may have been solid advice in 1985 but you will be missing your best "value" opportunities, if you follow it now.

- Youth or Sector: When we think of start-ups and young firms, we tend to assume that they are technology-based and that presumption, for the most part, is backed up by the numbers. However, there are start-ups in other businesses as well, and it is worth examining when mispricing occurs, whether it is sector or age-driven. It is true that young social media companies have gone public to rapturous responses over the last few years but Shake Shack, which is definitely not a technology company (unless you can have a virtual burger and an online shake) also saw its stock price double on its offering day and biotechnology companies had their moment in the limelight in 2014, as well.

- Life Cycle dynamics: I have talked about the corporate life cycles in prior posts and as I have noted in this one, there is evidence that the life cycle for a technology company may be both shorter and more intense than the life cycle for a non-technology company. That has implications for how we value and price these companies. In valuation, we may have to revisit the assumptions we make about long lives (perpetual) and positive growth that we routinely attach in discounted cash flow models to arrive at terminal value, when valuing technology companies, and perhaps replace them with finite period, negative growth terminal value models for fading technologies. In pricing, we should expect to see a much quicker drop off in the multiples of earnings that we are willing to pay, as tech companies age, relative to non-tech companies. I will save that for a future post.

I am under no illusions that this post will change the conversation about technology companies, but it will give me an escape hatch the next time I am asked about whether there is a technology bubble. If nothing else, I can point the questioner to this post and save myself the trouble of saying the same thing over and over again.

Loading...

Loading...

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Benzinga simplifies the market for smarter investing

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.

Join Now: Free!

Already a member?Sign in