Real estate investment trusts (REITs) may trade on major stock exchanges like any other publicly-traded company, but there are some key differences to understand when looking at a REIT's financial statement, such as funds from operations (FFO). Read further to learn how FFO is calculated, how this figure impacts your investment and what real estate investors need to know about the daily operation of their investments.

What Are Funds From Operations (FFO)?

Funds from operations are an important performance metric for real estate investment trusts (REITs). REITs and analysts calculate FFO to determine the amount of income, also known as cash flow, that is generated by the REIT in a given year.

Needless to say, the goal of every REIT is to have the highest FFO possible because the more cash flow a real estate investment generates, the more net income there will be to distribute to the equity owners (shareholders) of that investment. If the REIT is being properly managed, the FFO should be high enough that investors can receive the targeted dividends laid out in the investment prospectus.

Although FFO is a popular measuring stick for a REIT’s performance, it is not a generally accepted accounting principle (GAAP), so investors who want to figure out an individual REIT’s FFO may have to calculate it themselves. The good news is, all the information you need to figure out a REIT’s FFO is available in its quarterly or annual income statement.

Why Use FFO to Analyze REITs Instead of Net Income or EPS?

Even though FFO is not a generally accepted accounting principle, it can provide investors with a better idea of the potential returns a REIT may generate than just looking at the fund’s net income or earnings per share. Of several important reasons for this, the most important one is depreciation.

Depreciation is an investment principle that recognizes every tangible asset you buy will lose value and functionality over time. Newer, more modern assets come on to the market while your older asset continues to age.

So, even as the value of a given piece of real estate increases over time, the improvements made on the property (building, parking lot, fixtures) depreciate as they age. Because of this, property owners are allowed to take an annual depreciation write-off.

Specifically, REITs are allowed to write annual depreciation losses off against the net income generated by the REIT. Depreciation also means that capital gains and losses made by the fund through selling assets (property) aren’t a great predictor of how much income an investor can expect a given REIT portfolio to generate.

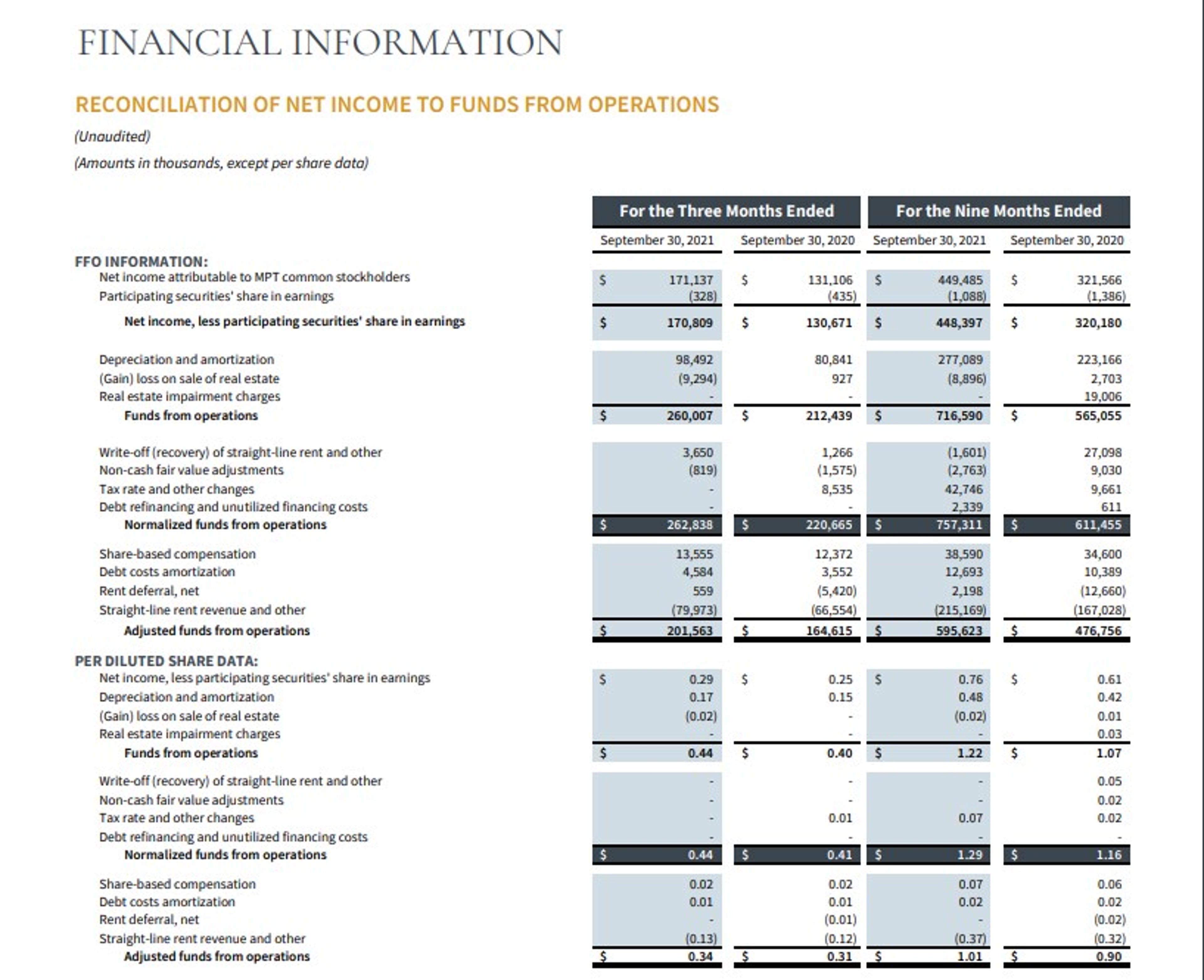

Take Medical Properties Trust (NYSE: MPW) Q3 Financials as an example. The fund reported over $170,000,000 in income but not before taking a depreciation write off of nearly $100,000,000.

What this means for investors is that just looking at the REIT’s net income and dividing it by the amount of shares won’t give them a complete picture of the REIT’s performance.

Earnings per share (EPS) is also not as effective a metric as FFO because a REIT’s EPS is reflective of the average earnings per share for all the investors. However, many REITs have shareholders with preferred equity.

Preferred equity shareholders get paid a higher dividend, usually as a result of making a much earlier or much larger investment in the REIT than average shareholders or retail investors. So, while a REIT’s annual EPS might be targeted in the 12% range, the EPS for non-preferred equity shareholders might be closer to 7% or 8%, which is a big difference.

You can use an FFO formula to take depreciation expense and other liabilities like EPS into account. That’s why it’s such a popular analytic tool for investors.

FFO Formula

Because FFO is not a generally accepted accounting principle, you may not see it listed on the prospectus or profit and loss sheet for a REIT. However, you can figure out a REIT’s FFO yourself by using some simple steps.

First, find the income statement from the REIT you want to analyze. Look for the REIT’s net income, which is usually at or near the bottom of the statement. Then subtract depreciation and any other expenses. These expenses are extremely important because you often pay for someone to manage the property, and that property is accumulating expenses throughout the year to ensure it’s a viable investment. In short, you’re not letting the property sit fallow and collecting money for the next 50 years.

The final net income, minus depreciation and remaining expenses, is the FFO.

So, for example, the Medical Properties Trust in Q3 of 2021 had a net income of $171,131,000. The fund wrote off $98,000,000 in depreciation.

Net Income $171,131,000.00

- Depreciation $ 98,000,000.00

FFO $ 73,131,000.00

Now you see why net income isn’t the best measure of a REIT’s performance. The net income number can be very high and still have a significant chunk of it taken out for depreciation. If you were to continue going down the Medical Properties Statement and subtracting other expenses, the FFO would get progressively smaller. As the FFO goes down, so does your dividend.

Interest Income

If you are analyzing a REIT’s financial statement to get its FFO and you see interest income, you should subtract that from the net income along with depreciation and other expenses. The reason for this is that interest income is not typically considered as having been derived from a REIT’s business operations, and that’s why you should not include it in your FFO calculations.

Using FFO When Analyzing a REIT

Once you have the FFO, you can use several different formulas to figure out the performance of a REIT. The most common formulas are listed below.

FFO per share: Divide the FFO by the number of outstanding shares.

FFO Pay-Out Ratio: This measures how much of a REIT’s FFO is being paid out in actual dividends. To get this number, first calculate the FFO per share. Then find the REIT’s dividend rate. Divide the dividend rate by the FFO per share, and you will have the FFO payout ratio.

Price/FFO: This formula compares the REIT’s share price to the FFO per share. Many analysts use it to compare the performance of one REIT to another. As a general rule, REITs with lower Price/FFO ratios are considered to be better value than REITs with a high Price/FFO ratio.

Adjusted Funds From Operations

Adjusted Funds From Operations (AFFO) is an even more advanced and accurate way to measure a REIT’s performance. There is no standard formula for AFFO; however, AFFO formulas usually have built-in adjustments to account for both additional revenue from rent increases and factors in the cost of anticipated capital expenditures and routine maintenance.

So, the AFFO is perhaps the most comprehensive method of analyzing a REIT’s long-term performance. Why? You’re truly planning for the future of the investment properties held by the REIT. Sure, there might have been some expenses this year, but what if the property must make green upgrades to satisfy Fannie Mae, causing it to spend that much more money on cap-ex expenditures.

Other FFO Variations

Different REITs own and operate a variety of different assets. Some may focus on residential properties while others may focus on office or industrial assets in filling out their portfolios. Each area of focus involves a different set of operating expenses and earning projections. Because of this, you may see other variations of FFO formulas, such as core FFO and normalized FFO on a REIT’s income statement or prospectus.

FFO: One of Many Measuring Sticks for REIT Investments

The old saying “the devil is in the details” applies to REIT calculations. When it comes to projecting dividends from long-term investments like REITs, it certainly is the case.

If you’re thinking about investing in a REIT or trying to choose between two REITs, you have to do a deep dive into the numbers.

Remember, expenses like depreciation, maintenance and capital improvements can eat up large chunks of a REIT’s net operating income in a given quarter or fiscal year. Just looking at the projected EPS that appears in the investment prospectus doesn’t take into account the differing splits for preferred equity shareholders and retail investors who are unlikely to hold preferred equity shares.

That’s why FFO is so important. If you execute the FFO calculation properly when analyzing a REIT, you’ll get a much better idea of the REIT’s performance than you would by just basing your decision on its net operating income or earnings per share.

Frequently Asked Questions

Are REITs a good investment?

Yes, REITs can be a very good investment because they allow you to invest in real estate without buying properties on your own.

Should you diversify with REITs?

Yes, you should diversify with REITs because they offer exposure to the real estate sector without worrying about holding cash to maintain the property.

About Eric McConnell

Eric McConnell is an alternative investment writer interested in rare collectibles, fine wines, art and sports memorabilia. He developed his love for sports during his childhood, where in addition to being an aspiring professional baseball player, he was an avid baseball card collector and reader of the Robb Report.

As is the case for many aspiring young sluggers, Eric’s baseball career came to an end the first time he encountered a pitcher capable of throwing 90 mph and a wicked curveball. However, his delight in the finer things of life never waned, and after a career in real estate, Eric branched out into writing, where he joined Benzinga as an alternative investment writer in 2021.

Although he covers breaking news in all areas of alternative investments, Eric’s favorite subjects harken back to his childhood days of reading the Robb Report and collecting baseball cards. He has a passion for writing about fine art sales, whiskey auctions and sports memorabilia.