If you’re like most tax filers, you don’t want to pay more taxes than you absolutely must. The good news is that the Internal Revenue Service (IRS) offers several perfectly legal ways to reduce the amount of tax you pay. A standard deduction is one option you can use to reduce your tax liability.

What is the Standard Deduction?

There are two ways in which the IRS allows you to reduce your tax liability:

- You can reduce your amount of income on which tax is calculated.

- You can reduce the amount of tax calculated on that income.

Tax credits and tax deductions are the two vehicles available to taxpayers for maximizing return and lowering your tax liability. Tax credits reduce the amount of tax owed without impacting your taxable bracket. Deductions, on the other hand, reduce the amount of your taxable income on which you calculate income tax and can lead to significant tax reductions.

The standard deduction is a tax-reduction option that falls into a category that could potentially do both of the above. You can reduce your taxable income by claiming the standard deduction. Once you subtract the amount of standard deduction from your income, it reduces the amount of income on which you calculate tax and reduces your tax liability.

While a tax credit directly reduces the amount of tax calculated on your taxable income, the standard deduction can reduce your taxable income to put you into a lower tax bracket and reduce the amount of tax you owe.

According to IRS statistics, roughly two out of every three returns filed claim the standard deduction.

How Much is the Standard Deduction for the 2018 Tax Year?

When you file your 2018 tax return, your standard deduction can vary between $12,000 and $24,000, depending on your age and filing status. This table explains the amount of basic standard deduction you might be eligible to claim:

Your Filing Status | Eligible Amount of Standard Deduction |

Single | $12,000 |

Married, but filing separately | $12,000 |

Married, and filing jointly or as a surviving spouse | $24,000 |

Head of household | $18,000 |

Depending on other circumstances, you could be eligible to claim an additional standard deduction. For tax filers 65 years of age and older, or for those who are legally blind, the additional standard deduction amount for 2018 is $1,300. If both you and your spouse are 65 years of age or older, your combined standard deduction amount is $2,600. Single tax filers or those filing as head of household can claim $1,600 as the additional standard deduction for 2018.

If another tax filer claims you as a dependent, your 2018 standard deduction amount will be $1,050 or the sum of your earned income plus $350.

The standard deduction, in this case, cannot exceed the greater of the two above values.

How Does the Standard Deduction Work?

Whether you claim the standard deduction or choose to itemize your expenses depends on your individual tax situation. However, choosing the standard deduction can reduce the amount of tax you pay — sometimes significantly!

This can happen in either of two ways:

- The standard deduction sufficiently reduces your taxable income and pushes you into a lower tax bracket. A lower tax bracket reduces the amount of tax calculated on a reduced taxable income.

- While the standard deduction may not change your tax bracket, it can help to reduce your taxable income, leading to a lower tax payment.

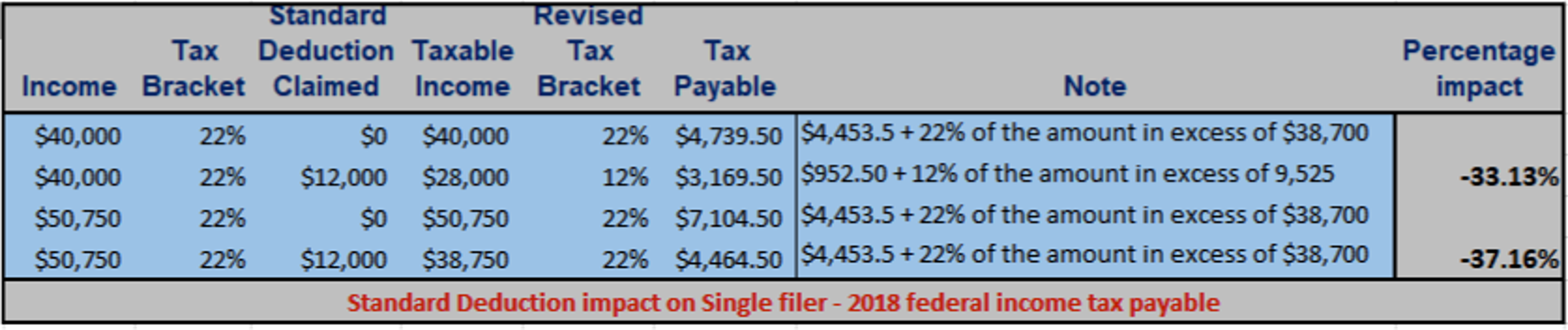

Let’s consider a couple of examples to see how the standard deduction works in both cases, highlighted above. These are hypothetical cases of how the standard deduction might impact an individual filer’s federal income tax liability on his or her 2018 returns. These examples only consider the standard deduction as a tax-reduction strategy. Realistically, there may be additional deductions, credits and refunds that may reduce a filer’s tax bill even further.

In our first example, a taxpayer has $40,000 of income, is in the 22% federal tax bracket, files as a single payer, and chooses not to use the standard deduction. As a result of this omission, she will owe $4,739.50 in federal income tax. If she were to take advantage of the $12,000 standard deduction eligibility, it would push her into the next lower tax bracket (12%), resulting in a tax payable of $3,169.50. That’s a total reduction of over 33%!

In our next example, a single tax filer has $50,750 in income and is in the 22% federal tax bracket. Not claiming the standard deduction would mean a federal tax liability of $7,104.50. However, by claiming the $12,000 standard deduction, he doesn’t move into a lower tax bracket but it still reduces his tax liability by over 37%, to $4,464.50.

Should You Itemize or Claim the Standard Deduction?

The IRS allows filers to take the standard deduction even if there are no other deductions or credits that you qualify for. Doing so reduces your taxable income by the amount of the standard deduction claimed. Claiming the standard deduction precludes you from deducting other popular expenses such as mortgage, charitable donations and medical bills from your income.

Whether you itemize or opt to claim the standard deduction will depend on your age, your taxable income, your filing status and the amount of other (nonstandard) deductions you’re eligible to claim. You may choose to either claim the standard deduction or itemize, but not both. While the standard deduction lowers your taxable income by a single fixed amount, itemized deductions do the same through a list of several applicable deductions.

While both strategies (itemizing and using standard deductions) can reduce your tax bill, it is possible that there are greater benefits for you from following one approach over the other. The general rule of thumb for deciding if you should itemize or go with the standard deduction is to choose whichever option reduces your tax liability the most.

When You Should Itemize

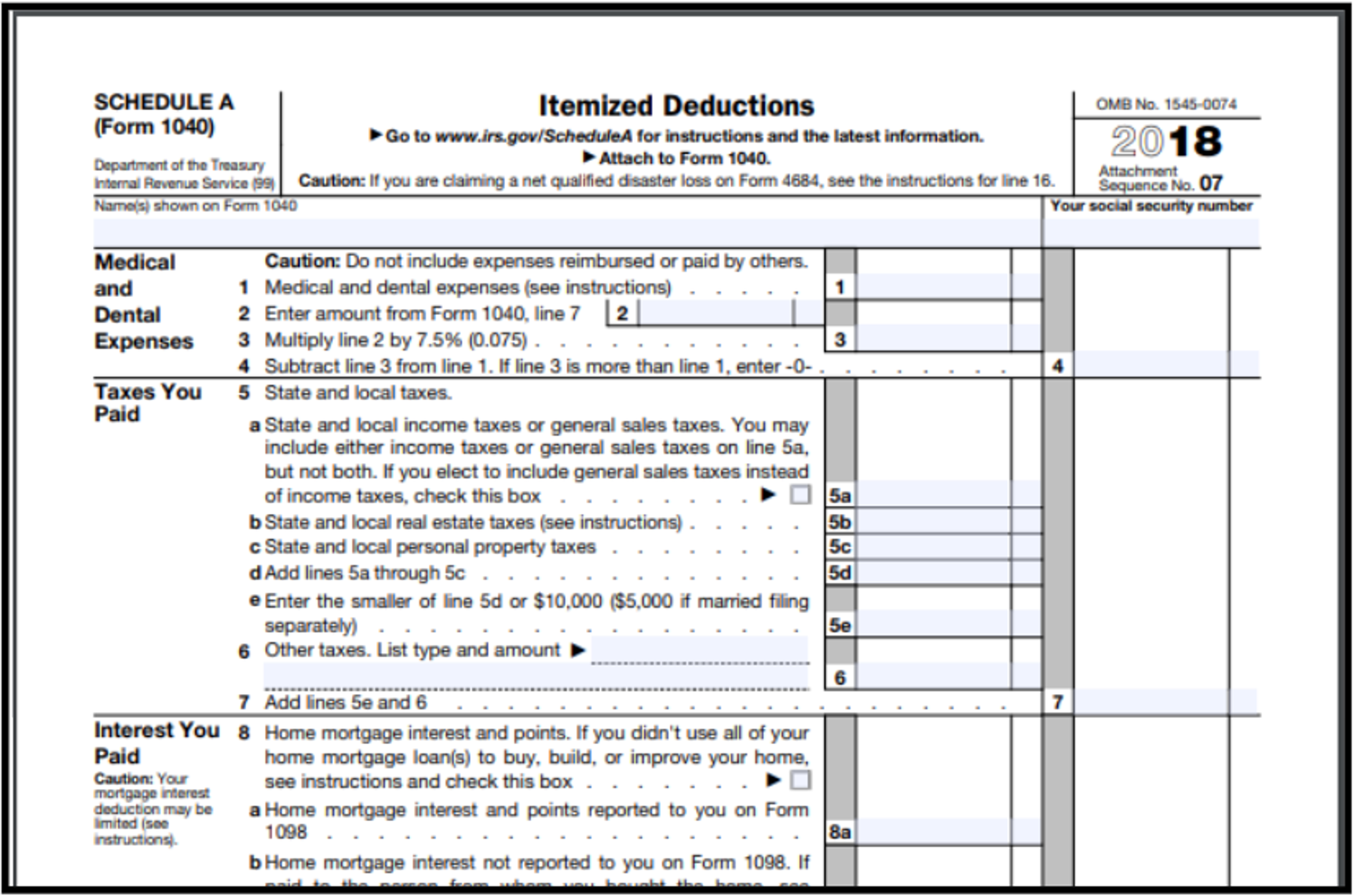

It is important to know how to itemize taxes in order to receive the maximum tax reduction. You itemize your deductions using Schedule A of Form 1040.

You might consider itemizing your deductions if:

- Your allowable itemized deductions exceed the amount of standard deduction you’re eligible to claim.

- You have appropriate documentation (receipts, canceled checks, statements, etc.) to support the itemized expenses you’re claiming.

- There are applicable circumstances under which you are not eligible to claim the standard deduction.

You should also consider itemizing if you:

- Have sizable qualified charitable contributions.

- Made large uninsured dental or other medical expense payments.

- Suffered significant uninsured theft or casualty damages from a federally declared disaster.

- Paid large sums as taxes or interest on your home.

- Have a substantial amount of “other deductions” listed on line 16 in your Form 1040, Schedule A.

If you are filing a tax return for a period less than 12 months, perhaps because your accounting period may have changed, the IRS only allows you to itemize your deductions. You cannot claim the standard deduction in such cases. The IRS also mandates that you itemize your deductions when filing as an estate or trust, partnership or common trust fund. In these situations, you can’t claim the standard deduction.

When You Should Claim the Standard Deduction

Keeping with the general rule of thumb discussed earlier, you should opt to claim the standard deduction if it’s greater than the sum of all your eligible itemized deductions. Typically, you would choose to claim the standard deduction because:

- It offers you an opportunity of a deduction even when you have no other expenses to itemize and reduce your taxable income.

- For whatever reason, you are unable, don’t have the time, or don’t wish to itemize your deductions.

- Even though you may have incurred eligible and itemizable expenses, your record-keeping isn’t precise enough to withstand an IRS audit. For example, if you claim an itemized expense but don’t have proper receipts or invoices, the IRS might disallow such expenses in the event of an audit.

Itemizing only make sense if you can do the math to determine that your itemized expenses are greater than the standard deductible amount. But it also means that you must be able to prove your expenses if/when the IRS asks for proof. If you’re unsure of either, then going with the standard deduction might make more sense. It’s simple, quicker and less complicated than itemizing.

Another reason to choose the standard deduction in any given year is because of the growth of the eligible amount available each year. In 2017, the standard deduction for a single filer was $6,350. For the 2018 tax year, that amount is $12,000. Filers filing under

Married filers filing separately might have another constraint for choosing the standard deduction over itemizing. If your spouse takes the standard deduction, then the IRS mandates that you must also opt for the same choice. Both spouses must follow the same strategy — standard deduction or itemizing. In this case, do the math to see which approach gives you the greatest tax liability reduction.

Generally, your status as a dual-status alien or nonresident alien may also preclude you from claiming the standard deduction. Alien or nonresident aliens can only itemize deductions. However, IRS Publication 519 does explain some circumstances under which you can claim the standard deduction even as a nonresident alien.

Making the Right Call on Standard Deduction

The IRS offers tax filers many ways to reduce their tax liability, including taking advantage of eligible credits or deductions. Standard deductions and itemizing expenses are just two such strategies provided in the tax code that can help you minimize the taxes you pay. However, you can only opt for one or the other — not both.

Whatever your tax filing status might be, you should run the numbers under both scenarios to determine what makes sense for your tax situation. Then, depending on the result, choose the option that gives you the biggest tax break.