As you may already know, the IRS imposes strict penalties if you blow off paying your required payment or filing your return. Though filing a late income tax return isn’t the end of the world, you might set yourself up for an additional bill from the IRS if you don’t take a few quick steps. If you’ve missed (or are going to miss) the April 15 deadline, use our guide to minimize the interest, fines, and fees you’ll have to pay.

What Happens if You File Your Tax Return Late?

The IRS may impose a number of penalties on you if you don’t file for an extension or pay your return by Tax Day, including:

A percentage penalty

If you fail to file your return by April 15, you will be charged 5% of your unpaid taxes for each month that your return is late. If you don’t file and you don’t make a payment, you will be charged 0.5% interest for each month that you don’t pay, in addition to your 5% penalty.

An additional penalty past 60 days

If your tax return is more than 60 days late, you will be charged a fee of either $135 or 100% of the unpaid taxes you owe, depending on which amount is lower. This penalty is applied to your account in addition to the percentage penalties you accrue for failing to file past April 15.

A return filed for you

If the IRS believes you’ve willingly refused to file a tax return, it may file a substitute return on your behalf. You will receive a Notice of Deficiency CP3219N in the mail along with the substitute return that the IRS has filed for you. The IRS has no obligation to make sure it has applied the maximum exemptions, credits, and deductions to your account. You’ll still have to pay fees and penalties for filing late, so a substitute return should never be thought of as a free filing service.

From the date that you receive your Notice of Deficiency, you will have 90 days to file a petition with the Tax Court if you would like to challenge the return. You also have to option to accept the substitute return and pay the proposed tax burden. If you ignore the Notice of Deficiency and don’t make a payment, you will trigger action from the Collections and Enforcement Agency. Penalties from here may include levies on your bank accounts, a notice of a federal tax lien on your property and even criminal prosecution.

These penalties all come in addition to any penalties your state may impose on you for failing to file your state taxes. Not sure if you have to pay state income tax? Check out our guide on how to pay state taxes to find out what you may owe on top of your federal dues.

How To File Late Taxes

If you find yourself in the position of needing to file your taxes late, follow our step-by-step guide for the proper process.

Step 1: Apply for an Extension Immediately

If Tax Day hasn’t passed, you can save yourself a significant amount of time and stress by filing for an extension as soon as possible. Filing for a tax extension isn’t a big deal. Every year, about 10 million taxpayers file a request for an extension and the vast majority of these requests are approved by the IRS. Requests for an extension are usually granted automatically and will not increase your chances of being audited. When your request is approved, you will receive an additional six months to file, which means you’ll need to submit your return on October 15 instead of April 15.

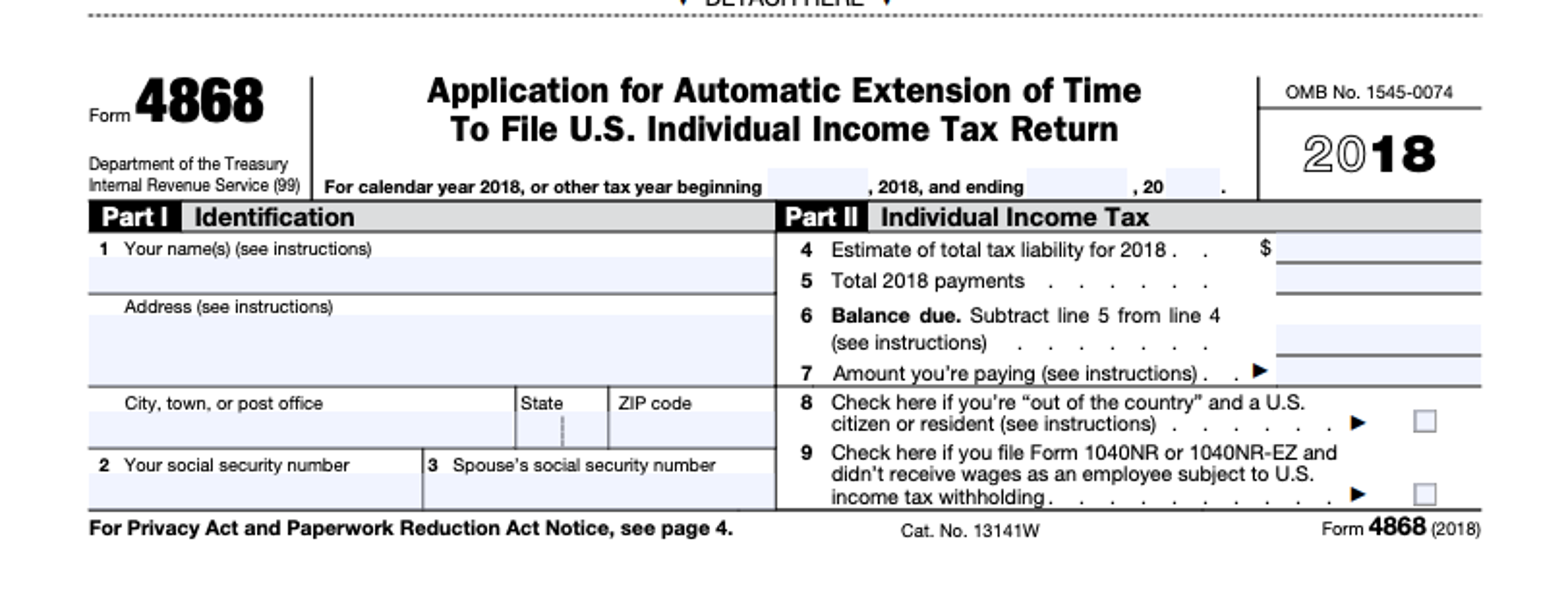

To file for an extension, you’ll need to download and fill out Form 4868. Form 4868 requires very little information and can be completed in five minutes. After you’ve filled out the form, you’ll need to mail it to the U.S. Treasury. If you file an extension for business taxes, you’ll need to download and fill out Form 7004 instead. Forms 4868 and 7004 are available to download for free at IRS.gov.

The best tax software packages incorporate Form 4868 into their programs. TurboTax includes the TurboTax Easy Extension application, which allows you to file for an extension without printing any forms or mailing anything to the IRS. Contrary to popular belief, filing an extension does not give you extra time to pay what you owe — it is only an extension to file your paperwork.

When mailing in your form, you’ll need to include a check for the estimated amount you owe. If you fail to pay, you can be charged up to 0.5% interest for each month you miss a payment. It’s imperative that your file your extension and include your payment as soon as possible. Otherwise, you may end up owing the IRS more money than you would have if you had filed earlier. While it is possible to file a request to pay your taxes late using Form 1127, these requests are not granted nearly as quickly or easily as requests to file late.

If you’d like to learn more about how and where you can file a tax extension, check out our crash course in tax extensions.

Step 2: Use a Tax Filing Software Program

If April 15 has already passed, focus on submitting your return as soon as you can. Though you have the option to file your taxes by hand even if you are late, you’re strongly encouraged to file using a tax preparation software program. When you file using tax software, your return is submitted instantly, which can reduce the amount you’ll have to pay in penalties.

When you mail in your tax return, you’ll have to wait through an extra processing period, which may contribute to more incurred interest. Tax software will also help you quickly locate and apply all credits, deductions and exemptions for which you qualify, which can help you save money and make paying easier.

Owe money to the IRS, but can’t afford to pay? You should still file your return as soon as possible. You may then choose to wait for the IRS to bill you (with late penalties) or you may negotiate a payment installment plan with the IRS. If you would like to begin an installment plan, attach a completed Form 9465 with your return. Form 9465 is a proposed installment plan that can help lessen your immediate financial burden. About 2.5 million taxpayers use installment plans to handle their back taxes.

Previous installment plan packages first require an in-depth audit of your finances and assets, but the IRS has removed this barricade for debts valued at less than $10,000. Paying the IRS immediately with a personal loan or credit card payment could be a much better option, as you’ll be charged a $52 fee to set up your installment plan and you are also subject to a fee series that equals out to 8% per year.

Step 3: Prepare for Next Year

The best way to avoid interest and penalties is to be ready to file on time next year. Keep a record of payments you make for business-related and childcare expenses (two common deductions) and keep records of taxes you’ve paid to help you avoid filing late next year. Mark next year’s Tax Day on your calendar so you give yourself plenty of time to gather your tax information.

Final Thoughts

Keep in mind that unlike credit card debt and some other types of debt, there is no statute of limitations on debt owed to the IRS. This means that if you don’t pay your tax debts for ten years, the outstanding bill will continue to accrue interest until you eventually pay what you owe. Penalties for paying late are relatively low but never underestimate the power of compound interest. If you try to pay your outstanding tax as soon as possible, you’ll probably find that filing late isn’t as big of a deal as you originally thought.

About Sarah Horvath

Sarah is an expert in the insurance, investing for retirement and cryptocurrency space.