If you’re a digital nomad working in another country or if you’re out of the country for extended periods of time, it’s important to understand how your time abroad affects your U.S. taxes, and specifically, the foreign earned income exclusion. If you qualify, this exclusion can significantly reduce your IRS tax bill.

The key to understanding the foreign earned income exclusion lies in its name. The IRS looks at earned income for this exclusion as opposed to dividend income or capital gains. Of course, the earned income also has to be earned in another country. We’ll also explain how to determine where you earned the income in accordance with IRS rules.

What is Foreign Earned Income?

If you’re a U.S. citizen living abroad, part of your earned income may be subject to U.S. taxes and part of your earned income may be excluded from taxes. If you’ve been filing taxes on your own, not all income is classified as earned income.

Earned income includes the following:

- Salaries and wages

- Commissions

- Bonuses

- Professional fees

- Tips

You can think of earned income as payment for personal services you perform, which differentiates earned income from unearned income. Unearned income includes dividends, pensions, capital gains, Social Security and similar income sources. A third category of income, called variable income, includes income from rent, business profits or royalties.

Foreign earned income is earned income paid to you while you live in another country. There are some guidelines as to whether the IRS actually categorizes you as living in another country. In most cases, it depends on how long you’ve been staying in another country and whether you still maintain a home base in the U.S.

Earned income includes certain non-cash income and allowances. If your employer provides you with a car, for example, or reimburses you for education costs, the value of these items is considered earned income.

What is a Tax Home?

Your tax home is usually where you’re currently working — or it may be the location of your business. For example, if you’ve been living and working in Barcelona for the past year, then Barcelona, Spain is your tax home, which also means you might also pay taxes in Spain.

Your tax home may differ from your residence, however. If you live an hour outside of Barcelona but work in Barcelona, Barcelona is still your tax home. The same idea applies inside the U.S. Your tax home is where you earn your income.

What is the Foreign Earned Income Exclusion?

The foreign earned income exclusion (FEIE) allows you to exclude up to $105,900 in earned income without paying federal income tax on those earnings for the 2019 tax year. For 2018, the limit was $104,100.

Not every world-traveling worker will qualify for the exclusion. If you do have foreign earned income, you may want to research the best tax software to help guide you through the math and eligibility qualifications. Errors in calculating the foreign earned income exclusion or taking the exclusion when you’re not eligible can result in a tax bill with penalties and interest.

Who Qualifies for the Foreign Earned Income Exclusion?

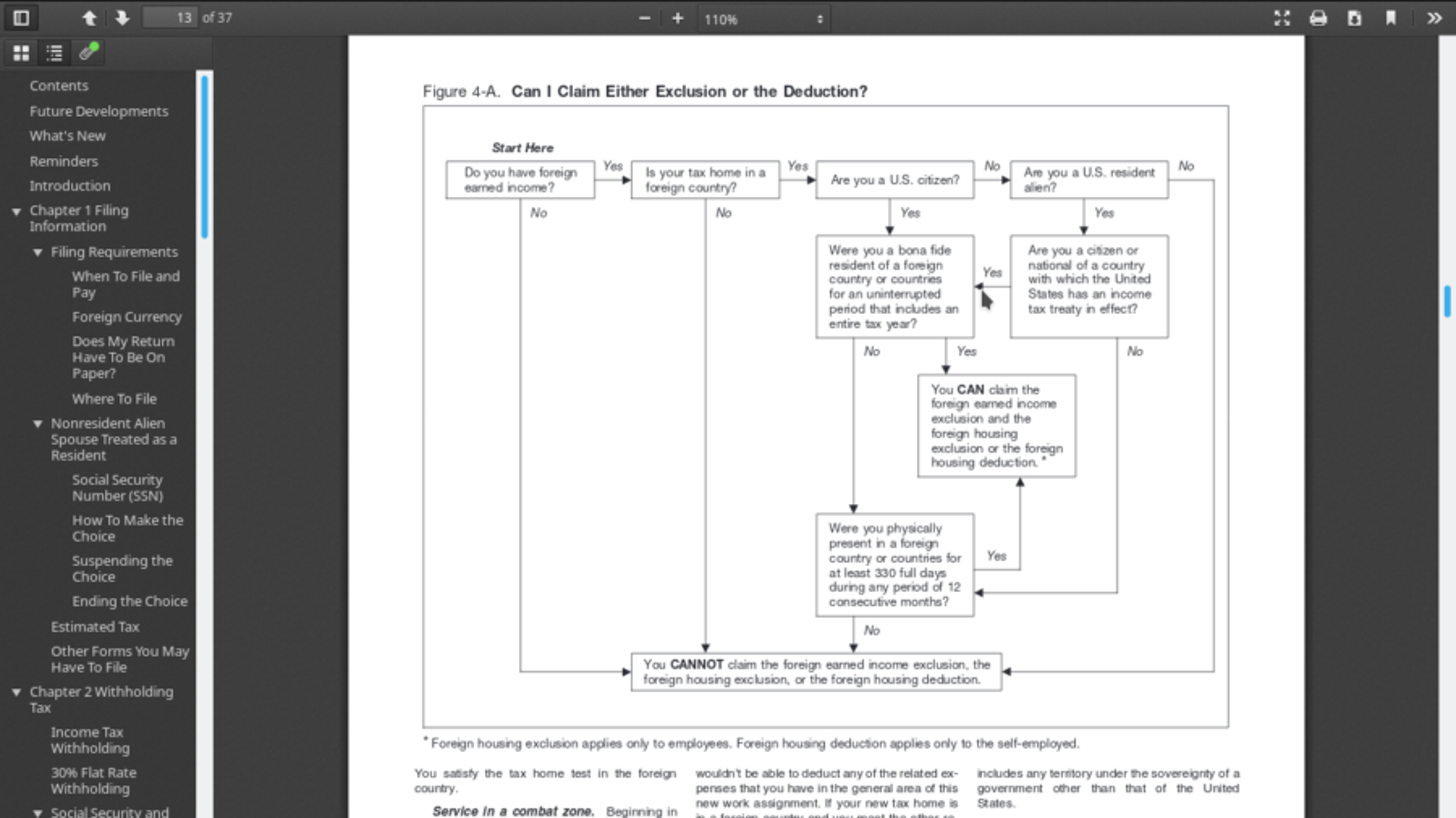

To determine eligibility for the foreign earned income exclusion, the IRS looks at two key tests. If you meet the conditions of either of these tests, it’s likely that you qualify for the foreign earned income exclusion.

Bona Fide Residence Test

The first of the two tests is the bona fide residence test, which examines how long you’ve lived in another country. If you live in a foreign country for an uninterrupted period that includes a full tax year, you meet the bona fide residence test. Bear in mind that a tax year spans from Jan. 1 to Dec. 31. You’ll also need to document your residence.

Physical Presence Test

The physical presence test is easier to meet but still requires a lengthy stay. In this case, you’ll need to be physically present for 330 full days during twelve consecutive months. The 330 days don’t have to be consecutive, which allows for travel and the calendar-based tax year isn’t considered, which may help you qualify.

There are some additional requirements as well.

To qualify for the foreign earned income exclusion, you have to be in your host country legally and you cannot have an abode in the U.S. The primary exception to the abode rule is if you are serving in the U.S. armed forces in an area designated as a combat zone.

The IRS definition of abode is based on where you maintain your family, economic and personal ties. Owning a home in the U.S. that’s rented out wouldn’t establish an abode by itself. The rules surrounding an abode can be complex, so maintaining an established life in the U.S. can disqualify you for the foreign earned income exclusion.

It’s important to note that income earned as an employee of the U.S. government while working abroad does not qualify you for the foreign earned income exclusion.

Which States Allow the Foreign Earned Income Exclusion?

In most cases, your state income tax liability is based on residence. Rules vary by state, and states like New Jersey and California are more aggressive about maintaining residency even if you’ve been away for a long time. Consider ties to a state like a driver’s license, owning property, or voter registration to be factors as to whether you’ll be liable for taxes in that state.

If you leave ties in a given state, the state may consider your time abroad to be transitory and still consider you to be a resident subject to income tax on foreign income earned. Invest some time in learning how to file state taxes for your home state if your state still considers you to be a resident while living abroad.

A small handful of states currently do not allow the foreign earned income exclusion, including Massachusetts, New Jersey, Pennsylvania, Alabama, Hawaii and California. If any of these states consider you to be a resident, expect to pay state taxes on all of your foreign earned income without exclusions.

How to Calculate the Foreign Earned Income Exclusion

If you’re a U.S. citizen working in another country, you’ll still need to file a U.S. tax return and may have state tax liabilities as well. The IRS provides Form 2555 and Form 2555-EZ to file taxes on foreign earned income. Form 2555-EZ can be used in simpler tax situations.

The foreign earned income exclusion doesn’t change your tax bracket. You still pay taxes at the rate that would have applied to your total foreign earned income, but a certain amount of foreign earned income is excluded from your final tax liability. The IRS provides worksheets to help guide your calculations when you use Form 2555 with your 1040 Form.

When you use the physical presence test to qualify for the foreign earned income exclusion, it’s likely that your time abroad spanned two tax years. In this case, the IRS allows you to prorate the exclusion based on the number of qualifying days in each tax year. You may also qualify for a prorated exclusion if your time abroad was interrupted due to civil unrest that forced you to leave your host country earlier than planned.

It’s important to note that the foreign earned income exclusion does not affect self-employment taxes, which are separate from income taxes and pay for Social Security and Medicare programs. Your tax liability for self-employment taxes is based on your total earned income without adjustment for excluded foreign earned income.

The foreign earned income exclusion is often used alongside the foreign housing exclusion or a foreign housing deduction. The foreign housing exclusion applies to amounts paid for housing expense paid by an employer — but the same earned income cannot be used twice in calculating exclusions. For 2019, the housing exclusion is 16% of the foreign earned income exclusion, or $16,944.

A separate foreign housing deduction may be used in some cases where housing expenses are paid with self-employment income. Generally, the foreign housing deduction is limited to 30% of the foreign earned income exclusion. As you might expect, both the foreign housing exclusion and foreign housing deduction are subject to qualification under the bona fide residence test or the physical presence test.

In some cases, you may also qualify for a foreign tax credit, which is intended to offset income taxes paid to a foreign government. Unlike a deduction, which can reduce your taxable income and can lower your bracket or reduce your taxes by a percentage, a tax credit has a dollar-for-dollar impact on your tax bill.

Final Thoughts

Taxes for expats or those working outside of the U.S. for extended periods can be complicated but you can structure your life abroad to comply with IRS requirements for the foreign earned income exclusion.

Note that a lot of people lose their eligibility when they maintain an abode in the U.S. If you want to take advantage of the foreign earned income exclusion and its related tax breaks, in most cases, you’ll have to make a clean break from the U.S for an extended time.

Expatriates and those working abroad are encouraged to read IRS Publication 54, Tax Guide for U.S. Citizens and Resident Aliens Abroad, which provides an overview of your tax responsibilities and tax treatment for foreign earned income.