The recent sell-off in the small and micro-cap biotech market has created some rather compelling buying opportunities for long-term focused investors. One name that I believe represents an attractive value at this level is Can-Fite Biopharma Ltd (ADR) CANF. Can-Fite is currently trading at just over $2.00 per share, equating to a market capitalization based on the NASDAQ-listed American Depository Shares of only $28 million on a basic count or $34 million fully-diluted. This level vastly undervalues the pipeline at Can-Fite in my opinion, which includes three drugs for a total of six different indications. And what makes the story even more compelling is that Can-Fite likely exited 2015 with over $17 million in cash and investments and no debt, putting the net enterprise value at only $11 million.

I believe Can-Fite is worth multiples of its current valuation. Below I provide a summary of the company's key pipeline assets and provide context and modeling support to justify my belief as to why I see the shares trading at a compelling value today.

CF101 For Rheumatoid Arthritis & Psoriasis

Can-Fite has three different drug candidates that progressive through various stages of development. One such candidate is CF101 (piclidenoson), an orally bioavailable A3 adenosine receptor (A3AR) agonist. A3AR is a Gi protein-associated cell surface receptor found to be overexpressed in both inflammatory and cancer cells vs. low expression in normal cells (1). The mechanism of action of adenosine agonism in inflammatory conditions involves the inhibition of the formation of cAMP and its downstream effectors, PKA and protein kinase B/Akt (PKB/Akt). The reduction in the activity of these two kinases results in the deregulation of the Wnt and the nuclear factor kappa-B (NF-κB) signal transduction pathways, leading to the inhibition of tumor necrosis factor α (TNF-α), interleukin-6 and -12, macrophage inflammatory proteins and receptor activator of NF-κB ligand (RANKL) (2, 3).

Given this mechanism of action and demonstrated excellent safety and tolerability seen in previous clinical programs, Can-Fite is currently preparing to initiate registration studies with CF101 in both rheumatoid arthritis (RA) and psoriasis in 2016. Specifically, management plans to file a Phase 3 protocol with the European Medicines Agency (EMA) for CF101 in the treatment of RA here in the first quarter 2016. Initiation of patient enrollment is anticipated in the second or third quarter of 2016. Can-Fite recently filed a trial protocol with the institutional review board (IRB) of Barzilai Medical Center in Israel, one of the planned clinical sites for the international trial to be conducted in Israel, Europe, Canada and the U.S. The Phase 3, multicenter, randomized, double-blind, placebo-controlled, parallel group study will investigate the efficacy and safety of CF101 administered orally twice daily for 16 weeks to patients with active RA treated with conventional (non-biologic) drugs. The study will have three arms, 1 mg CF101, 2 mg CF101, and placebo, given orally twice daily in the form of tablets. Approximately 456 patients are expected to be enrolled in the study.

For investors not familiar with CF101 as a treatment for RA, I prepared a detailed article in December 2015 comparing the drug to the market leader in this category and the world's current number one best-selling drug, the anti-TNF-alpha biologic, AbbVie's Humira® (adalimumab), as well as Pfizer's FDA-approved orally available Xeljanz® (tofacitinib) and Eli Lilly's baricitinib, which is currently under FDA review. I encourage investors to view the article, because what I found is that CF101 (piclidenoson) compares quite well to both Xeljanz® and baricitinib. CF101 also looks superior to methotrexate (MTX), a drug that is part of the standard of care and used by roughly 90% of RA patients (4). The graphs I built comparing CF101 to these drugs can be seen below, with the raw data found in the aforementioned article.

RA is an enormous market opportunity. According to Visiongain, the global rheumatoid arthritis market is forecasted to reach $38.5 billion by 2017. Pfizer reported Xeljanz® sales of $523 million in 2015, with $172 million coming in the fourth quarter alone. The consensus according to Capital-IQ is for approximately $1.5 billion in sales in 2020. Can-Fite will need to partner CF101 to compete with industry behemoths like AbbVie, Pfizer, and Eli Lilly, but given some of the recent deals we have seen in this area like Gilead-Galapagos, Celgene-Receptos, and Lilly-Incyte, big pharma is clearly looking to biotech for anti-inflammatory drugs and CF101 has a number of unique characteristics that make it a potential attractive in-licensing candidate.

Below is a snapshot of my CF101-RA model. I believe CF101 is a potential $500 million drug for the treatment of RA in the U.S., EU, Canada, and Israel. On a net present value (NPV) basis, I believe CF101 for the treatment of RA is worth $50 million in value, almost double what Can-Fite is trading at today.

Beyond RA, CF101 also has significant potential as a treatment for psoriasis. This is not surprising, considering AbbVie's generates over 50% of its $14 billion in global sales for Humira® from dermatology. Other anti-TNF drugs like Enbrel® and Remicade® are also major players in both RA and psoriasis. Pfizer is attempting to gain approval for Xeljanz® in psoriasis but received a complete response letter from the U.S. FDA in the fourth quarter last year. Can-Fite is currently working to complete the design of a Phase 3 study for CF101 in the treatment of psoriasis, with a goal to file with the EMA in the first half of 2016. Patient enrollment is targeted to begin in the fourth quarter of 2016.

Perhaps the drug that makes the most sense to compare CF101 to is Celgene's Otezla® (apremilast), a drug that generated $472 million in global sales in 2015. Otezla® is a small molecule inhibitor of PDE4, an enzyme responsible for the degradation of cAMP. The inhibition of PDE4 results in an increase in cAMP, which in turn regulates a number of pro-inflammatory and anti-inflammatory mediators including TNF-α, IL-23, and IL-10 (5). The downstream mechanism is very similar to CF101, and thus a direct comparison of the two drugs can be made. This is an analysis that I conducted in August 2015, and I encourage investors to view that article.

The chart below is that direct comparison of CF101 and Otezla®. Investors should take notice of the standardized the Y-axis of PASI responder scores and the X-axis of time-on-drug. Although Otezla® outperforms CF101 at week 16 on both PASI-50 and PASI-75, the Otezla® efficacy quickly begins to wain, declining by week 32 (5). On the contrary, CF101 efficacy continues to improve at week 32, far outperforming Otezla® with an upward trajectory at the end of the study.

According to Capital-IQ, analysts believe Otezla® will post sales of approximately $2.5 billion for Celgene in 2020. Celgene is seeking approval for the drug in RA as well. As noted above, Otezla® looks like the best direct comparator for CF101 given the similar downstream mechanism of action. Similarly to RA, I expect Can-Fite to seek a commercialization partner for the drug in psoriasis. It is likely that the company will look to strike one deal for CF101 in both indications. Nevertheless, psoriasis alone is another potential $500 million indication for the drug, and NPV analysis suggests another $25 million in value for label expansion into psoriasis.

CF102 For Liver Cancer & NASH

In September 2015, Can-Fite received U.S. FDA Fast Track designation for CF102, another A3AR agonist, as a second-line treatment for hepatocellular carcinoma (HCC), the most common form of primary liver cancer. This is an indication for which Can-Fite has also been granted Orphan Drug status given the high unmet medical need and lack of effective treatment options for patients failing first-line therapy.

Can-Fite is currently conducting a Phase 2 trial with CF102 in patients with advanced HCC and Child-Pugh B cirrhosis (NCT02128958). Child-Pugh is a scoring system proposed as a way to predict the outcome of liver cancer patients following surgical resection. The scale looks at variables of liver function, including bilirubin and albumin levels, as well as incidences of ascites, encephalopathy, and prothrombin (clotting) time. The scale is highly correlated with overall survival, with median overall survival of Child-Pugh A, B and C patients with HCC approximately 9.8 months (range 6.4-13), 6.1 months (range 4.9-7.3), and 3.7 months (range 1.5-6), respectively (6).

In Can-Fite's Phase 2 trial, a total of 78 patients randomized 2:1 to receive 25 mg of CF102 or placebo twice a day for consecutive 28-day cycles. The study is currently ongoing in Israel and Europe. The primary outcome of the study is overall survival, which will not be evaluated until after 75 deaths have occurred. The first patient was dosed in December 2014 and management anticipates data from the study in mid-2016.

The primary market for CF102 is in liver cancer patients failing Bayer's Nexavar® (sorafenib), a drug that generated just over $1 billion in global sales in 2015. Clinical data suggests that the Child-Pugh B Nexavar-failure market is rather large, estimated at over 90% of the eligible patients that take the drug (7). Can-Fite previously completed an open-label Phase 1/2 study with CF102 in 18 HCC patients that yielded encouraging results (NCT00790218). According to the 2013 publication, median overall survival in the study population, 67% of whom had received prior Nexavar®, was 7.8 months, and for Child-Pugh B patients (28%) it was 8.1 months. Stable disease by RECIST was observed in four patients for at least four months. CF102 also helped maintain liver function over a six month period (8).

With a minimum of 25,000 targetable patients in the U.S. and EU, the peak opportunity to Can-Fite looks like approximately $250 million. Based on Nexavar® sales, Onyx has been able to penetrate about 30% of the addressable market. If Can-Fite, through a commercial partnership similar to the one Onyx signed with Bayer/Amgen, can accomplish a similar level of penetration, the U.S. revenue opportunity for CF102 is $150 million. The opportunity in Europe is likely another $100 million in my view.

However, the interesting opportunity for Can-Fite is in countries in Southeast Asia where the rates of primary liver cancer are significantly higher due to epidemic-like infection rates of hepatitis B and C. The World Cancer Research Fund International estimates that 80% of the global primary liver cancer patients on earth are found in less developed countries outside the U.S. and EU. For example, the highest incidence rates can be found in Mongolia, Lao, Gambia, Vietnam, Korea, Thailand, Cambodia, and China. CF102 approval in these regions easily doubles my peak sales forecast.

I believe there is a meaningful opportunity for Can-Fite to sign licensing and distribution agreements in areas like China and Korea. Management has already out-licensed its other clinical-stage candidate, CF101, to Kwang Dong Pharmaceutical in Korea, so this management team has experience partnering with large Korean pharmaceutical companies. They also have experience negotiating term sheets with companies in China and Japan. Licensing deals that provide upfront cash to Can-Fite for CF102 in Asia will help support the U.S. and EU development plans. NPV analysis suggests that CF102 in HCC is worth another $20 million in value (see below). I expect this number to increase dramatically if the ongoing Phase 2 trial is positive; however, the even larger potential for CF102 may be in the earlier progression of liver disease, starting with non-alcoholic steatohepatitis (NASH).

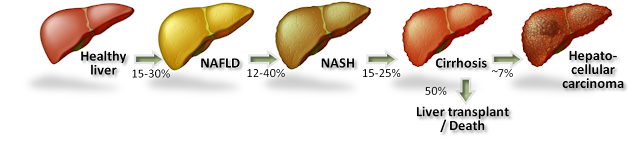

On November 23, 2015, Can-Fite announced the development of CF102 will be expanded into NASH based on compelling preclinical data. NASH, also called "fatty liver", is a condition in which fat builds up inside the liver causing inflammation. Prior to the presence of inflammation, the disease is simply referred to as non-alcoholic fatty liver disease (NAFLD), the most common form of liver disorder in the U.S. The accumulation of macroglobular fat inside the liver causes oxidative stress that reduces the efficiency of the liver and can lead to increased liver enzymes such as alanine aminotransferase (ALT) and aspartate aminotransferase (AST). Loss of liver efficiency and oxidative stress leads to inflammation, liver cell ballooning, and the development of NASH. Prolonged inflammation results in cirrhosis (scar tissue), liver failure, or liver cancer.

Rates of NAFLD and NASH are increasing in the U.S. in concert with increasing rates of obesity and diabetes. In fact, NASH is now the third leading cause of liver transplant in the U.S. According to the U.S. National Institutes of Health, an estimated 15-30% of Americans have fatty liver, with approximately 20% going on to develop NASH. The American College of Gastroenterology estimates 2-5% of adult Americans and up to 20% of those who are obese may suffer from NASH, putting the target population in the country between 5 and 10 million individuals. Despite the progression of several interesting clinical-stage candidates by companies such as Gilead, Genfit, and Intercept, there are currently no U.S. FDA approved treatment options for NASH.

New preclinical data studying CF102 in a mouse model of liver disease revealed the drug's capability to improve liver pathology in NAFLD and NASH. The data showed:

- CF102 had a statistically significant reduction in NAFLD Activity Score (NAS) compared to placebo. NAS was developed to provide a numerical score for patients who most likely have NASH. Accordingly, NAS is the sum of the separate scores for steatosis (0–3), hepatocellular ballooning (0–2), and lobular inflammation (0–3), with the majority of patients with NASH having a NAS score of ≥ 5. This system was developed as a tool to quantify changes in NAFLD during therapeutic trials. The CF102 preclinical data shows statistical significance for both the high and low doses.

- CF102 reduced liver-to-body weight compared to placebo. Because of the excess accumulation of globular fat and inflammation of the liver, a NASH liver becomes enlarged and heavier than a normal healthy liver. A reduction in liver-to-body weight is evidence of reduced fat and inflammation in the liver and a sign that the drug is the improving disease condition.

- Liver sections from the placebo group exhibited severe micro- and macrovesicular fat deposits, hepatocellular ballooning and inflammatory cell infiltration, whereas the CF102 treated group showed a significant decrease in steatosis, ballooning and lobular inflammation compared to the placebo group.

- CF102 decreased plasma ALT and triglycerides levels in the livers of NASH-model compared to placebo. This is a sign of improved liver function and efficiency. Separate studies with CF102 demonstrated efficacy in the treatment of liver regeneration and function following liver surgery.

- Representative photomicrographs of H&E-stained liver sections showed improved pathology in animals receiving CF102 vs. placebo.

NASH is believed to be the next big global pandemic given the soaring rates of obesity, diabetes, and metabolic syndrome all over the world. The mechanism of action for CF102 looks like a pan-hepatic improver of liver pathology, applicable to earlier-stage liver diseases such as NAFLD and NASH. I have yet to model sales of CF102 in NASH. The preclinical data above are impressive, but I believe that human proof-of-concept data must be generated before any monetary value to the asset should be ascribed. That being said, the value of CF102 in NASH could dwarf the value in HCC, or even what I have modeled above for CF101 in RA and psoriasis. The NASH market is enormous and wide-open at this stage, so CF102 in NASH represents nice upside to investors in my view. A Phase 2 study is expected to start in 2016.

Other Important Programs

I'm not going to spend a lot of time talking about CF602 for the treatment of erectile dysfunction (ED). CF602 has yet to enter the clinic; the investigational new drug (IND) application is planned in the fourth quarter 2016. That being said, I do think that CF602 could address a big missing piece of the ED market. I wrote a short article on the subject in October 2015. It was a rather fun article to do background research on, specifically with respect to the marketing practices of Pfizer with Viagra® and Lilly with Cialis®, so I hope investors will check it out. The takeaway on CF602 is that the drug does seem to have an interesting niche and could become a major driver of valuation for Can-Fite in the coming years; but as of today, I believe it is safer to assume a value of zero until we see human data.

Similarly, I'm not going to spend a lot of time talking about CF101 as a treatment for glaucoma, currently in Phase 2 trials with data expected in the second quarter 2016. Can-Fite's subsidiary, OphthaliX Inc. (OPLI) is conducting this trial. Can-Fite owns approximately 82% of OphthaliX Inc., a company listed on the OTC exchange with a market capitalization of $10.4 million. The potential for an oral medication for the treatment of glaucoma is quite intriguing. According to GlobalData, the glaucoma market is estimated at $3 billion in value, with the majority of treatment options consisting primarily of generic eye drop drugs. Oral administration may vastly improve patient compliance. Results from the 88-person Phase 2 trial should give investors a better sense of the opportunity here for Can-Fite and OphthaliX Inc. For the purpose of my valuation, I've assigned $5 million in value to the program, half of the market capitalization of publicly-traded OphthaliX Inc.

Valuation

I believe there exists a considerable investment opportunity in shares of Can-Fite at this level. CF101 and CF102 are targeting large market opportunities and the existing data looks favorable when compared to commercially validated drugs like Otezla®, Xeljanz®, and Nexavar®. My NPV analysis incorporates peak sales projections for these drugs, an appropriate discount rate, and probability adjustment based on odds of success stemming from the stage of development and my analysis of the existing clinical data generated by the company to date. My work leads me to believe that Can-Fite's pipeline is worth approximately $100 million in value.

Can-Fite likely exited 2015 with approximately $17.5 million in cash on the books, strengthened by capital raised in September and October last year. This number seems sufficient to fund operations until the second half of 2017, with the potential to move beyond this target should the company out-license or partner any of its assets in the next 12-18 months. At some point, Can-Fite is going to have to raise more money, but I do not see this as a near-term risk. Operating burn is relatively low for a company at this stage. Nevertheless, I am not including the cash balance in my final valuation number to account for the expected burn over the next 18 months. As such, I believe Can-Fite is worth approximately $100 million in value, which equates to roughly $6.00 per fully-diluted ADS.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Comments

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.