John Canally is the Chief Economic Strategist for LPL Financial.

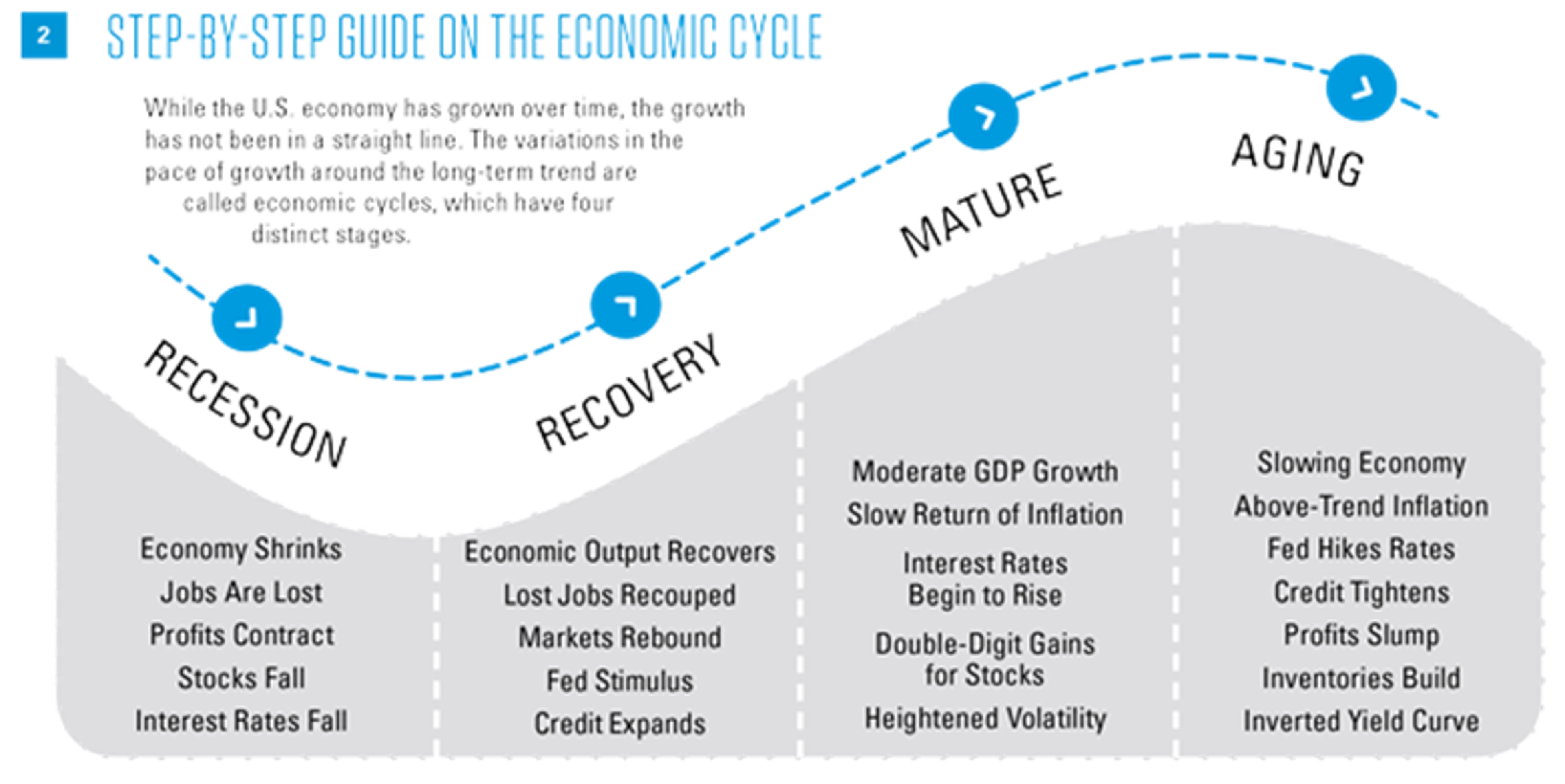

U.S. Economy Restarts Its Growth Climb

We continue to expect that the U.S. economy will expand at a rate of 3 percent or slightly higher over the remainder of 2015, once economic conditions recover from yet another harsh winter—and other transitory factors—that held back growth in the early part of 2015. This forecast matches the average growth rate over the past 50 years, and is based on contributions from consumer spending, business capital spending, and housing, which are poised to advance at historically average or better growth rates in 2015. Net exports and the government sector should trail be hind.

Overseas, ongoing quantitative easing (QE) by the European Central Bank (ECB) will help to anchor the nascent economic recovery in the Eurozone, while easing already put in place from the Bank of Japan (BOJ) should secure acceleration in Japan’s economy in the second half of the year. In China, growth has slowed from the unsustainable 10–12 percent pace seen in the first decade of the 2000s to around 7 percent this year, but we continue to expect Chinese policymakers to use all the tools in their toolbox (monetary, fiscal, and regulatory) to hit the 7 percent growth target. For more on our thoughts on the global economy, see our international discussion, “Be Careful Not to Overtighten.”

International and emerging markets investing involves special risks, such as currency fluctuation and political instability, and may not be suitable for all investors.

After the weather-induced slow start to 2014, the U.S. economy—as measured by growth in real gross domestic product (GDP)—pieced together a solid final three quarters, as annualized GDP growth averaged nearly 4.0 v.* As 2015 began, the economy appeared to have built up some much needed momentum, with GDP posting growth of 2.5 percent or more in 6 of the prior 10 quarters through the fourth quarter of 2014.

But another harsh winter, particularly in the eastern U.S., a major port strike that disrupted trade, and sizable cuts to business capital spending in the energy sector, along with the stronger dollar, combined to secure a decline in GDP growth in the first quarter of 2015.* These transitory factors have begun to fade, starting with improving weather and the end to the port strikes, and potentially extending to the stabilization of the U.S. dollar and oil prices.

* GDP data from Q1 2012 to Q1 2015 are subject to revision on July 30, 2015.

Outside of the Eurozone, China, and Japan, central banks that rushed to cut rates in early 2015 to get ahead of the ECB are likely to be more cautious with that tool in the second half of 2015. This may allow the surge in the dollar versus the currencies of its major trading partners to ease and even start to reverse some of the sharp rise seen between mid-2014 and mid-2015. The stabilization of the dollar, a pickup in global growth, and oil production cuts in the U.S. and elsewhere may lead to oil prices building on the gains made in the early spring of 2015, after a sharp 40 percent drop from June 2014 through March 2015.

Drivers Of Bounce Back

As temporary challenges from the first quarter fade, we expect the economy to reaccelerate. Key drivers of improvement include a bounce back in business capital spending, an acceleration in housing, improving exports (as overseas economies accelerate), and ongoing solid performance of the “good old American know-how” economy, which saw little or no impact from the factors listed above in the first quarter of 2015.

Since the beginning of the current economic expansion in the second quarter of 2009, the good old American know-how economy has outperformed the “old” economy by a sizable margin [Figure 1]. Looking ahead, the competitive advantage of the U.S. in the service sector, including good old American know-how, should help continue to drive economic activity and employment higher in this sector, especially in areas that require advanced skills. U.S. reliance on exports (and employment) in the less volatile service sector, which continues to be in high demand in fast-growing emerging markets worldwide, should help promote longer U.S. economic expansions. Less dependence on the boom-and-bust inventory cycles that accompany more goods-based, export-dependent economies around the world is an additional positive contributing factor for the U.S. economy. Good old American know-how is our most abundant resource and should continue to make the U.S. an attractive destination for the world’s capital.

If our forecast of 3.0 percent+ GDP growth over the remainder of 2015 is met, the economy will enter its seventh year of expansion in June 2015, and by the end of the year would become the fourth-longest economic expansion since World War II (WWII) at 78 months. The current recovery is already longer than the average economic recovery duration of 58 months.

Perhaps the best comparisons for the current expansion may be the three economic expansions since the end of the inflationary 1970s, a period that has seen the transformation of the U.S. economy from a domestically focused, manufacturing economy to a more import-heavy, services-based, “knowledge” economy.

The last three expansions, which began in 1982, 1991, and 2001, respectively, lasted an average of 95 months, or roughly eight years. By that measure, the current economic expansion still has room to build on the progress made so far, given the lack of economic imbalances that typically herald the end of an economic expansion. Regardless, this economic expansion has likely entered its latter half, which is not only marked by strong economic growth, but also the potential for rising inflation, accelerating wage growth, and eventual Fed rate hikes.

Wage Growth & Inflation Are On Back Order

The labor market is a lagging indicator of overall economic activity. The current economic expansion began in June 2009, but the private sector economy did not regularly begin creating jobs until early 2010. The economy has since added 12 million jobs, with more than 3 million created in the 12 months ending in May 2015 alone, or approximately 250,000 jobs per month. If GDP growth achieves our 3 percent forecast over the remainder of 2015, the economy should routinely create between 200,000 and 250,000 jobs per month—as it has during the middle of every business cycle over the past 30 years when economic growth was between 3 percent and 4 percent—with wage growth rising from around 2 percent in early 2015 to closer to 3 percent by the end of 2015. We expect jobs, and therefore economic growth, will be concentrated in the areas of the economy that focus on good old American know-how. In addition, the continued stabilization of oil prices in the second half of 2015 may provide some relief to labor markets and regional economies of the hard hit oil patch.

Although rising wages and inflation often begin to emerge as the business cycle ages, many more factors are still pushing down on inflation than lifting it higher, both in the U.S. and globally. Just as inflation traveled across the globe in the 1960s, 1970s, and early 1980s, the risk of deflation is doing the same in the 2010s. The tepid pace of the current economic expansion in the U.S.—combined with intermittent economic growth in Europe and Japan, and a decelerating Chinese economy—has maintained the threat of deflation. Furthermore, a rising dollar and a sharp drop in commodity prices over the past year have left many economies on the brink of deflation.

Inflationary pressures may nonetheless build over the second half of the year and beyond, supported by stronger U.S. economic growth, loose monetary policy, and normalizing commodity prices. Weak productivity growth over the first six years of the current expansion—influenced in part by the subpar pace of capital spending—may also increase the likelihood of inflation, as productivity growth determines how fast an economy can expand without creating inflationary pressures.

Beneath the surface of the disinflationary environment (a period characterized by rising prices, but at a slower rate than in the past), some inflation never disappeared. Service sector inflation has accelerated since 2010 and remains poised to potentially move even higher as the economy accelerates [Figure 3], even though goods inflation (commodities, clothing, food, etc.) decelerated sharply in recent years. We continue to expect a modest acceleration in inflation over the second half of 2015, enough to make the Fed “reasonably confident” that inflation will head back to its 2.0 percent target.

Based on the forward-looking economic data, the odds of a recession in the second half of 2015 or in 2016 are still low, but we remain vigilant for signs that the imbalances typically leading to recessions are beginning to build.

Be Careful Not To Overtighten

Overseas, monetary policies hammered out in early 2015, and what we expect to be enacted over the remainder of 2015, are big potential drivers of global growth, impacting most of the largest international economies. While the U.S. is close to tightening its monetary policy bolts following the recovery from the Great Recession, the majority of global central banks are not ready to pick up their screwdrivers and start tightening.

Rotate Counterclockwise: Monetary Policies Drive Global Growth

LPL Research’s Monetary Policy Impact Monitor measures changes in real GDP growth relative to other major economies (vertical axis) compared with a measure of each country’s monetary policy (horizontal axis) as of the end of 2014 [Figure 4]. The 2012 values were added for the U.S., Eurozone, China, and Japan to give a sense of the natural rotation of countries at different stages of recovery. The monitor helps show the interaction between monetary policy and economic growth and provides a quick visual of the current global landscape.

Countries generally move counterclockwise: A weaker economy with tighter policy typically leads to policy-loosening action. If the policy is effective it will lead to improved growth and eventual policy-tightening action until the economic cycle leads to renewed weakness. The policy impact monitor shows how this rotation takes place relative to the other countries. Countries with trailing growth tend to be relatively more aggressive about monetary policy. Ideally countries want to be able to sustain healthy growth with minimal central bank intervention.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.