Lights turned red today for the first time this year amid concerns that rising bond yields could put a brake on the long rally. Markets moved lower across most of Europe, and stocks fell sharply in U.S. pre-market trading.

Early Wednesday, Bloomberg News reported that China might consider slowing or halting its purchases of U.S. Treasuries. China is the world’s biggest foreign holder of U.S. Treasuries, and its purchases are one factor that have kept the bond market supported and yields low over the last decade. Remember, yields fall when bond prices rise. It’s unclear why China might adopt this strategy, and nothing is official, so panic isn’t warranted. Keep in mind that borrowing costs remain historically low both here and abroad, and U.S. bonds continue to offer foreign investors a better rate than they’d get in Europe or Japan. However, the situation is worth monitoring.

After the Bloomberg report, U.S. 10-year Treasury yields climbed five basis points to nearly 2.6% for the first time since last March, up about 15 basis points from the end of last year. Even before today’s news, yields had been climbing amid positive U.S. economic data, rising rates in Europe, and some market chatter this week that Europe and Japan might be inclined to take their feet off the stimulus gas pedal a bit earlier than expected due to economic growth. Yields now aren’t far from last year’s high of 2.63%, reached in March, and that might be a technical resistance level to watch today. The last time yields traded higher than that was in mid-2014.

Meanwhile, the two-year Treasury yield has been riding the elevator upward since October, and now trades at nearly 2%. As Briefing.com pointed out Tuesday, that’s above the average S&P 500 dividend yield of 1.91%, meaning that for some investors, bonds might start looking like a more lucrative place to park some money than they were, say, a year or two ago. This could ultimately start hurting some stocks, especially those in the telecom and utilities sectors where yields are one of the big draws. It looked like that might already be happening on Tuesday, as those two sectors were among the only ones to suffer losses. Telecom really took it on the chin, falling nearly 2%.

Another reason higher yields sometimes hurt the stock market is by potentially raising the cost of borrowing for companies and consumers. Though the Fed raised rates three times last year, borrowing costs remain pretty low by historic measures. This has helped companies invest in their operations and conduct mergers and acquisitions, among other things. Low rates also tend to keep borrowing costs down for consumers, allowing them to invest in big-ticket items that companies manufacture like cars, refrigerators, and homes.

Until this morning, the firm momentum from 2017 had continued to carry into the New Year, with little sign of the profit taking some market professionals had anticipated. There’s a “buy the dip” mentality, meaning even if the market falls 2%, buyers might come in because they’ve been rewarded for it in the past. In football, if running up the middle keeps working, a team is likely to keep doing it. The same is potentially true for traders and investors, because people tend to stick with what’s tried and true.

Tuesday was one of those days where just focusing on the Dow Jones Industrial Average ($DJI) might fool you. The $DJI rose more than 100 points, mustering much of that strength from just a handful of its components including Boeing Co BA, General Electric Company GE, United Technologies Corporation UTX, and Johnson & Johnson JNJ. The broader S&P 500 (SPX) and Nasdaq (COMP) also registered gains, but only modest ones. Both the SPX and COMP had been higher earlier in the day, but came under pressure as the session advanced.

Oil rose early Wednesday and the dollar fell sharply after yesterday’s gains, hurt in part by the Bank of Japan’s (BOJ) move yesterday to trim its purchases of Japanese government bonds. That BOJ move, which sparked rumors that the BOJ might start tapering its stimulus earlier than expected, sent the yen higher. Gold spiked early Wednesday as the stock market and dollar slumped.

Fed speakers are back on the prowl today, with several expected to talk. These include Chicago Fed President Charles Evans, St. Louis Fed President James Bullard, and Dallas Fed President Robert Kaplan. It’s unclear if any will take questions or speak on topics of the day, but if any do comment on the bond market, their views could be interesting to hear.

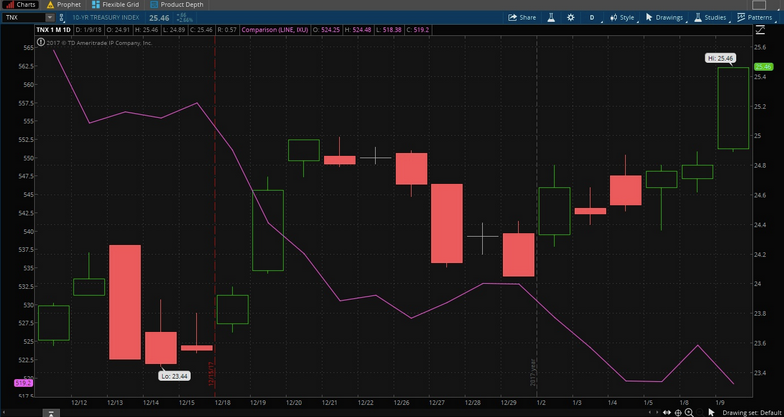

FIGURE 1: UP GO YIELDS, DOWN GO UTILITIES. The 10-year Treasury yield (candlestick chart) hit another 10-month high Tuesday above 2.5%. Meanwhile, the utilities sector (purple line) traditionally among the most rate-sensitive sectors, has been playing serious defense over the last month. Higher bond yields sometimes draw investors away from higher-yielding sectors. Data source: Standard & Poor’s, CME Group. Chart source: The thinkorswim® platform from TD Ameritrade. For illustrative purposes only. Past performance does not guarantee future results.

Oil Costs Keep Rising

Another potential barrier for the stock market could be steadily rising oil prices. Crude reached $63.60 a barrel early Thursday, the highest price since late 2014 for a front-month U.S. futures contract. The same concerns that lifted oil last week seem to remain in place, including less output from OPEC, falling U.S. supplies, unrest in Iran and Venezuela, and the recent spell of cold U.S. weather that raised demand for heating oil. Today brings the weekly U.S. government crude oil production and supply report, and analysts expect supplies to continue falling as they have for several weeks. This would potentially be a bit bullish, but some Wall Street analysts think the oil market has gotten over-heated, and U.S. production remains near record levels.

Inflation Watch

The Producer Price Index (PPI), due early Thursday for December, can sometimes give a sense of whether producers feel price pressure that they might pass along to consumers. November’s PPI might have made some people sit up and take note, as it rose 0.4% (with core PPI that strips out food and energy rising 0.3%). That was the third consecutive month of relatively strong PPI readings, and that could be read as positive because it might indicate strong underlying demand in the economy. On the other hand, PPI also could raise concerns about percolating inflation if it keeps rising at that level. Wall Street analysts look for December PPI to rise a little less than in November, with 0.2% the consensus estimate, according to Briefing.com.

Also on the inflation front, last week’s employment report showed a pretty solid 0.3% rise in wages in December, and wages are now up 2.5% year-over-year, compared with more like 2% a few years ago. The economy continues to crank out new positions at a pretty hefty rate, despite December’s surprising weakness in retail employment, and eventually employment becomes a case of diminishing returns and employers have to start competing on wages. That’s something the Fed would probably be happy to see from an inflationary point of view.

FOMO Part 2

Last year, we brought up the millennial concept “FOMO,” which means “Fear of Missing Out.” Many people who didn’t get into the markets over the last few years could be suffering a bad case of FOMO right now, considering the big gains. Maybe you’re one of those, and you’re wondering if it’s too late to get into the game with the market seemingly hitting new all-time highs every day. The answer is no, it’s not too late, but consider doing so in a way that doesn’t put you “all in” to the market at once, because you can’t expect to buy stocks and just see them rise immediately. A gradual approach could be useful at this point, and remember to keep careful track of the average price you pay for each stock. There’s a lot of talk right now about the high price of stocks and the length of the current rally, but even expert investors usually can’t time the market. What’s more important is finding a price you’re comfortable at for a particular stock and not putting all your money in right away.

Information from TDA is not intended to be investment advice or construed as a recommendation or endorsement of any particular investment or investment strategy, and is for illustrative purposes only. Be sure to understand all risks involved with each strategy, including commission costs, before attempting to place any trade.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.