Valero Makes New High Amid High Gasoline Prices

As shares of Valero Energy Corporation VLO traded near a new 52-week high Monday, David Berman noted in D.C. newspaper The Hill that, according to Energy Information Agency data, 2012 tied 2008 in terms of the share of household income consumed by gasoline costs. The comparison to 2008 is instructive in appreciating why gasoline refiner Valero has done so well recently.

Refiners such as Valero profit from the "crack spread" -- the difference in prices between what they pay for crude oil and what they sell refined products (e.g., gasoline, diesel) for. In the summer of 2008, when gasoline prices were nearly as high as they are now, oil prices were much higher -- peaking at about $145 that July. On Monday, according to Bloomberg data, March-dated West Texas Intermediate (WTI) crude oil contracts traded at $96.05 (this is nearly $20 less than the current price of Brent crude, as new North American supplies have lowered the cost of WTI). High gasoline prices and lower domestic oil prices mean a bigger crack spread for U.S. refiners such as VLO.

Crack Spread Works Both Ways

Just as a widening crack spread is tailwind for refiners such as Valero, a narrowing crack spread -- an increase in oil prices relative to the prices of refined products -- can be a major headwind for them. For VLO investors considering adding downside protection in the event of a narrowing of the crack spread -- or the advent of other potential headwinds -- over the next several months, in this post, we'll look at three different ways of hedging VLO against a greater-than-20% drop.

Why Consider Hedging Against A >20% Drop

A twenty percent decline threshold is worth considering here, because it lowers the cost of hedging somewhat (all things equal, the larger the potential loss you are looking to hedge against, the less expensive it is to hedge), and because a 20% decline is not necessarily an insurmountable one. To recover from a 20% loss, an investor would need a 25% rebound in his stock. But to recover from, say, a 35% drop, would require a rebound of nearly 54%.

Three Ways To Hedge VLO

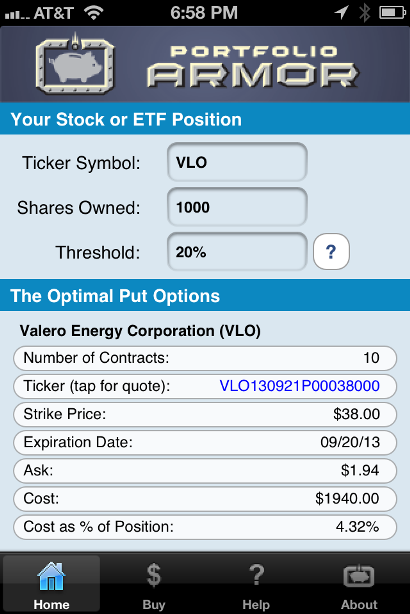

The first way uses optimal puts*; this way has a higher cost, but allows uncapped upside. These are the optimal puts, as of Friday's close, for an investor looking to hedge 1,000 shares of VLO against a greater-than-20% drop between now and September 20th:

As you can see in the screen capture above, the cost of those optimal puts, as a percentage of position, is 4.32%. By way of comparison, the current cost of hedging the SPDR S&P 500 ETF SPY against the same decline, over the same time frame, is 1.07% of position value.

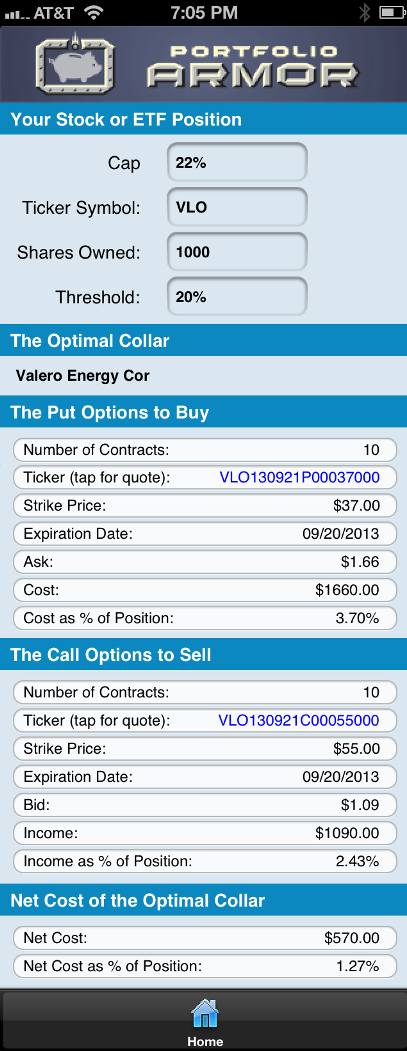

A VLO investor interested in hedging against the same, greater-than-20% decline between now and September 20th, but also willing to cap his potential upside at 22% over that time frame, could use the optimal collar** below to hedge instead.

As you can see at the bottom of the screen capture above, the net cost of this optimal collar is 1.27%.

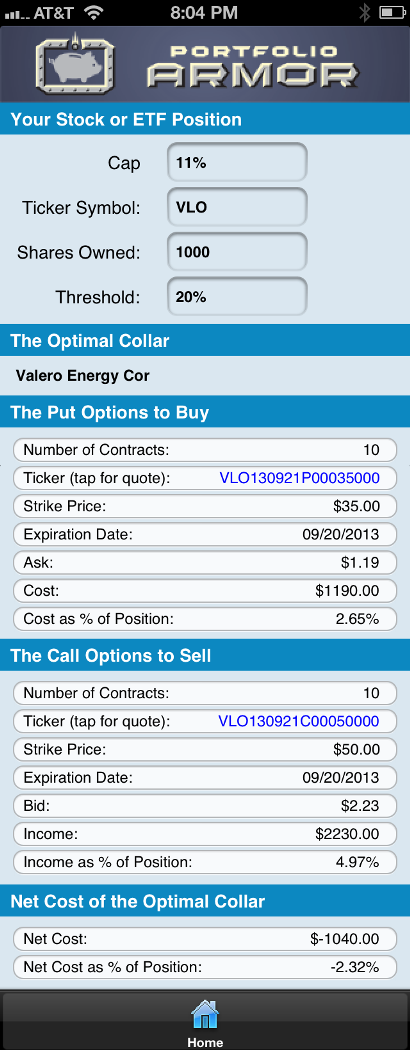

Finally, an investor who wanted to hedge against the same decline threshold over the same time frame, but who was willing to accept a tighter cap on his potential upside -- 11%, in this case -- could use the optimal collar below to hedge.

As you can see at the bottom of the screen capture above, the net cost of this optimal collar is negative -- that means that the VLO investor would be getting paid to hedge in this case.

*Optimal puts are the ones that will give you the level of protection you want at the lowest possible cost. Portfolio Armor uses an algorithm developed by a finance Ph.D to sort through and analyze all of the available puts for your stocks and ETFs, scanning for the optimal ones.

**The algorithm to scan for optimal collars was developed in conjunction with a post-doctoral fellow in the financial engineering department at Princeton University, and is currently available on the web version of Portfolio Armor.

The screen captures above come from the latest build of the soon-to-come 2.0 version of the Portfolio Armor iOS app. Optimal collar capability will be available as an in-app subscription in the 2.0 version of the app.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Comments

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.