Credit is one of those notoriously confusing financial vehicles. It's the bane of many people's existence, but it is also all-but essential for financially independent survival. It's a device that can hinder or help future financial investments, and the decisions made that have reciprocal influences can haunt or bless for years to come.

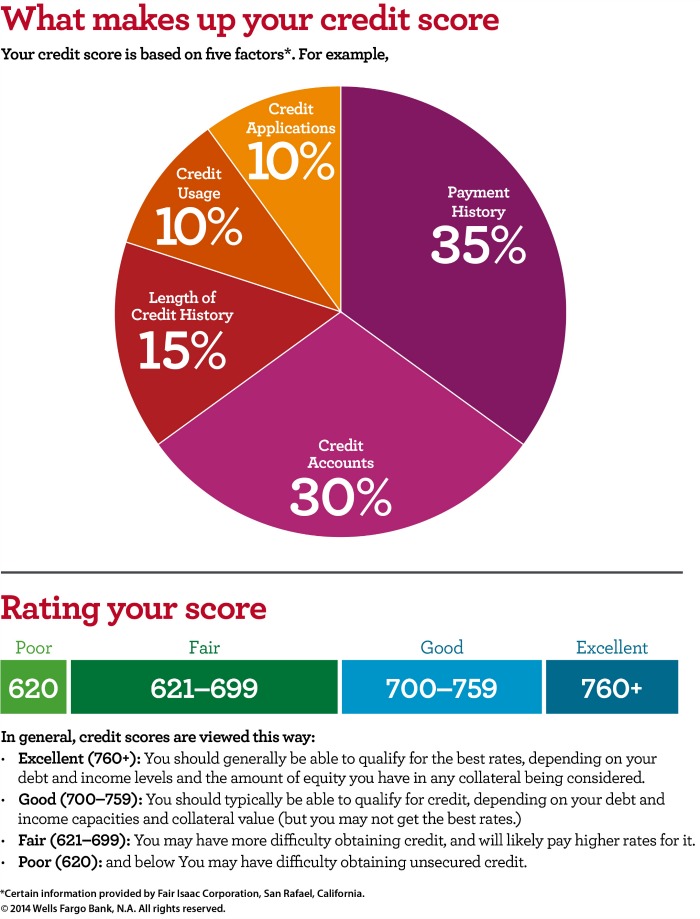

One frustrating aspect about credit is its longevity. The length of time one holds credit greatly influences the ability to receive additional credit. Extensive — good — credit history is one of the main elements of a credit report, and it is heavily weighted when calculating credit scores. As credit scores are used by lenders and other professionals to determine the responsibility of an individual both fiscally and personally, it would make logical sense to try and establish a shining credit history as early as possible.

However, based on a variety of reasons, establishing credit as a young person is exceedingly difficult. But, is there something parents can do to help their children get on the right path? How young is too young to have a credit card? Are there other ways of establishing credit for young children without giving them access to credit cards?

Kids And Credit

Perhaps the strongest argument against giving children their own credit cards is the inherent risk of misuse. If a 20-something has a proclivity to overspend, how much greater is the risk for a teenager?

The bottom line is that credit can be built without free access to unlimited cash.

While each circumstance will vary, as some kids are inherently more responsible or naturally money smart, there are steps that parents can take to help nudge their children on the right path to building credit.

Consider These Options

A Word Of Caution

Co-signing on a credit card is not the same as allowing your child to become an authorized user on one of your cards. While, if either is misused, you can find yourself responsible for their debt, co-signing has its own degree of risk. By co-signing, you are putting your own credit on the line for someone else, at the expense of your credit history without reaping the initial benefits of that line of credit. (It is true, however, that if the primary signee handles the co-signed loan impeccably, the co-signee may see the benefits.) Bottom line: Seriously consider the pros and cons before every co-signing any loans with anyone, regardless of their relationship to you.

One further note: Credit card companies are unlikely to approve credit for anyone under the age of 18; however, minors can be added to an adult's accounts at a much younger age. Do not be discouraged by the stages of financial freedom, embrace them and use them to your benefit.

If you have concerns or questions, reach out to those in your network who can help. Talk to a financial advisor or personal finance expert to make a game plan for your family. Invest in yourself today by taking the time to sow financial literacy in your family. You'll inevitably reap the rewards.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.