Key Takeaways

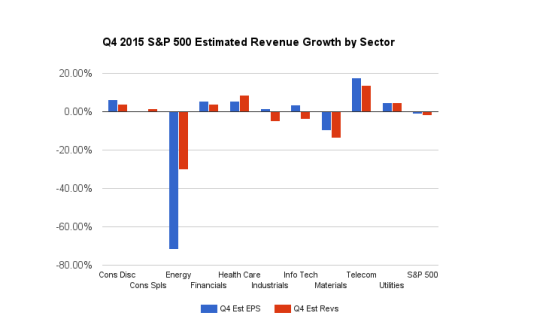

- The Estimize community expects the S&P 500 index to report Q4 2015 EPS growth of -1.4% and revenues of -2.2%

- The end of the third quarter officially marked a "revenue recession" for the S&P 500

- Themes this quarter will once again revolve around China and lower oil prices

- Q4 sector leaders: consumer discretionary and health care

- Q4 sector laggards: energy and materials

Call it the déjà vu quarter. Expectations for the fourth quarter are looking awfully familiar at this point to every other quarter reported in 2015. Once again we start out the season in the red, with S&P 500 EPS growth estimated to decline 1.4% year-over-year (YoY), and revenues to decline 2.2%. If these estimates turn out to be correct, this would be the fourth consecutive quarter of negative revenue growth, meaning we were officially in a "revenue recession" at the completion of the third quarter season. Many other themes from the third quarter have also carried over.

Revenue Recession

Much has been made over the last year of an impending "earnings recession," ie: three consecutive quarters of YoY profit declines for the S&P 500. However, we haven't seen a down quarter for EPS since 2009, just barely eeking out of the red last quarter with 0.6% growth. Revenues on the other hand are heading for their fourth consecutive quarter of negative growth, meaning sales growth was technically in recession territory at the completion of Q3 2015. Companies continue to manipulate EPS numbers, but don't have that same ability on the sales front. It's a trend that we've seen since Q3 2012, meager revenue growth in the low single digits or worse, and it's certainly cause for concern.

The China Impact

There is no doubt China will be heavily mentioned in Q4 and full year 2015 press releases. The weakening Chinese economy will continue to have a crushing impact on commodities, as it is the largest importer worldwide. Comps for the energy and materials sectors continue to dip lower as a result. However, the China impact will affect more than those two sectors. Many consumer discretionary companies, specifically retailers and restaurants, now also count on the world's second largest economy for a large chunk of their sales each quarter.

Lower Oil Prices

Lower oil prices will continue to impact a number of sectors, both negatively and positively. Just as analysts thought oil couldn't get any lower, Brent Crude tumbled an additional 31% in Q4, and WTI fell 19%. A heavy oversupply of oil can be thanked for pushing prices further downward during the quarter. This of course is not good for energy companies which are expected to show the biggest declines this season. However, other sectors such as consumer discretionary, and even some industrials (airlines and transports & logistics) may get a boost. The positive potential impact hasn't fully been recognized yet, as consumers are not necessarily reallocating gasoline savings back into the economy, and transports have missed out on fuel surcharges.

Sector Leaders

The fourth quarter will present many of the same winners as the prior 3 quarters of 2015. But this time around those growth expectations are more muted; don't expect any double-digit growth leaders.

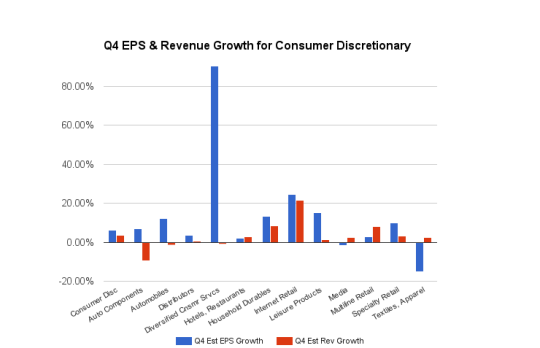

Consumer discretionary is currently at the top of the leaderboard, but only expected to put up EPS growth of 6.3%. While the expectation is not terrible, we typically look for more robust results in the fourth quarter due to the inclusion of the holiday shopping season. As mentioned above, for the past year many have been waiting for oil savings to be passed on through to the retailers. Instead, many consumers have taken lower prices at the pump as an opportunity to save money after years of not having that ability. They are also allocating discretionary income to other places outside of traditional retail, such as tech and health care. The industry winners within this sector continue to be internet retail, household durables and automobiles. The latter two point to a newer trend that emerged in 2015, where consumers were confident enough in their financial position to start making large ticket purchases again. This lead to an increase in the sales of homes, cars and appliances.

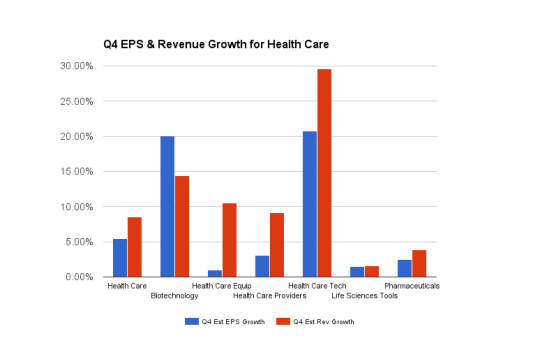

After leading all 10 sectors for the entire year, health care takes a bit of a back seat in Q4, with analysts calling for EPS growth of 5.5% and higher revenues of 8.5%. This would mark the first quarter that health care puts up single-digit growth after six consecutive quarters of posting double-digits. Once again, biotechnology leads the way with EPS expected to increase 20.1% and revenues up 14.4%. Health care technology is even a tad higher, with EPS growth anticipated to come in at 20.8% and revenues of 29.6%, however, only Cerner is contained in that industry.

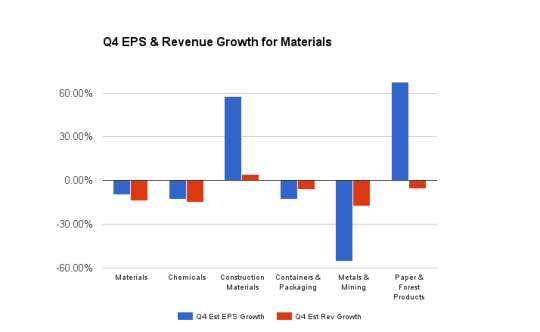

Sector Laggards

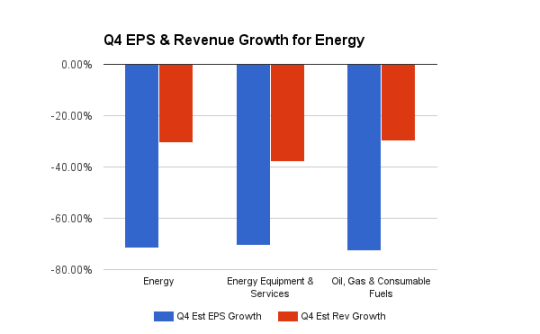

As hinted to earlier, the laggards this season are energy and materials. At present, estimates for energy call for a -71.6% decline on earnings and -30.4% on revenues. Meanwhile, materials are expected to worsen to -10% and -13.7%, respectively. The main culprit here is of course the metals & mining industry, with profits expected to crater 55%, and revenues anticipated to decline 17.3%. Alcoa, the only aluminum company within the index and the one that unofficially marks the start of the season, is expecting EPS of $0.05 as compared to $0.33 in the year-ago quarter, suggesting a YoY decline of 85%.

Q4 Scorecard

Of the 21 companies that have reported thus far for Q4, 57% have managed to beat the Estimize EPS consensus, with 33% missing and 10% matching. While it's still early on in the season, revenues are already off to a bad start. A meager 19% of companies that have reported for the quarter have beaten the Estimize revenue consensus, continuing the trend of weak sales figures.

This week starts out light, with only 11 S&P 500 companies scheduled to report, including many of the banks such as JPMorgan Chase, Wells Fargo and Citigroup.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.