Loading...

Loading...

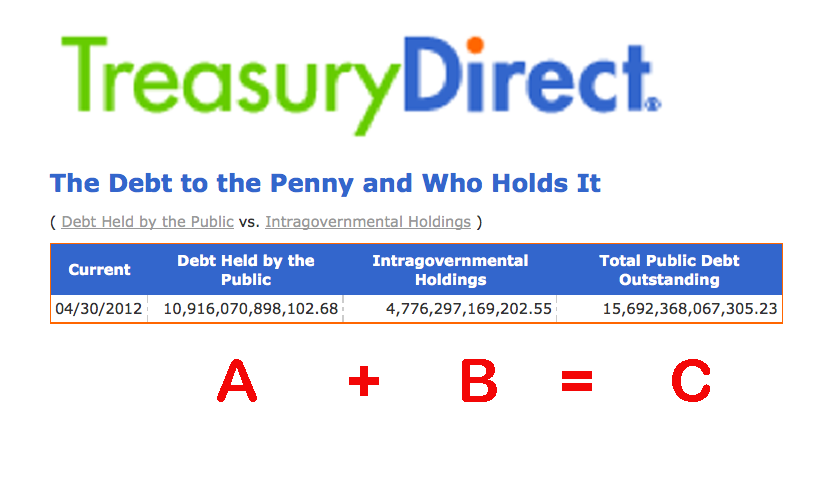

America has two classes of debt: Debt Owed to the Public (DP) and Intergovernmental Debt (IG).

The two components of debt as of April 30, 201:

The IG accounts consist of the Trust Funds (TF). The three largest funds are Social Security (SS), the Federal Employee Retirement Fund (FERS) and the Military Retirement Fund (MRF).

The Congressional Budget Office (CBO) provided projections for these retirement programs in its January 31, 2012 report, "The Budget and Economic Outlook" (

Link). The numbers that CBO uses are consistent with the projections provided by SS, FERS and MRF individually in their annual reports. The following discussion relies on the CBO's numbers.

The basic TF arithmetic is as follows:

The sum of

(a) Tax receipts (cash in) plus

(b) Interest (non cash), minus (

c) Benefit Payments (cash out), minus (

d) Overhead (cash out) equals Net Surplus/Benefit.

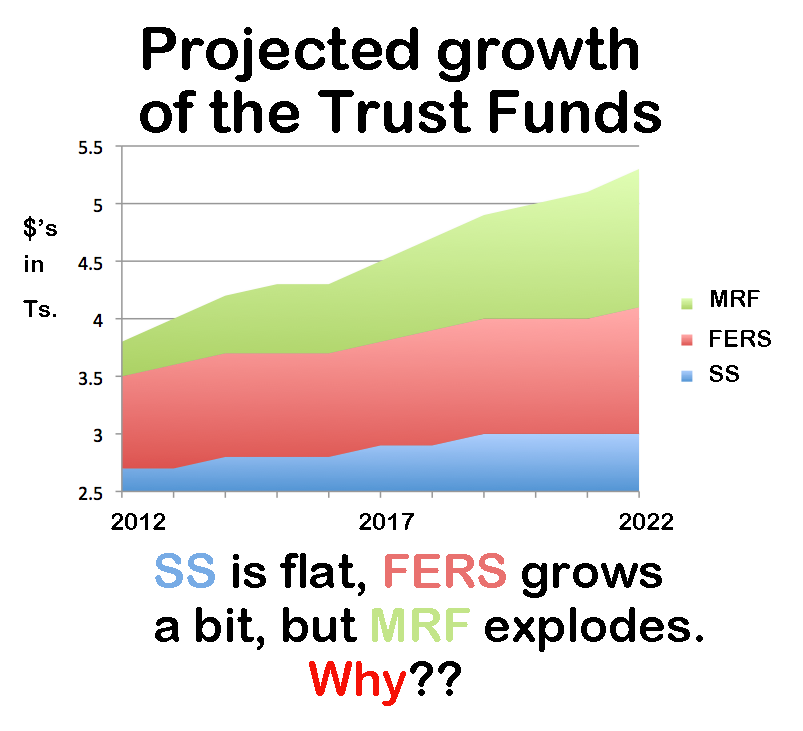

This slide looks at the CBO's projected growth of the retirement funds:

Loading...

Loading...

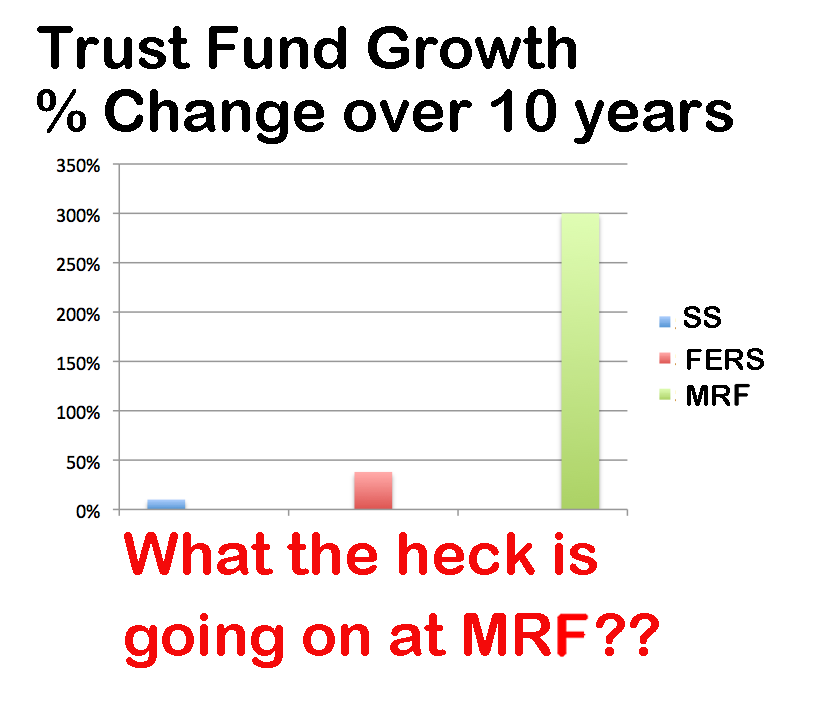

The chart above shows that the MRF is expected to grow while SS and FERS remain relatively flat. The following looks at the projected percent change in these funds.

The MRF's 300% increase jumps out at me, and I ask, “

What's that about”?

The answer is interesting.

MRF uniquely benefits from a special law that obligates the Treasury Department to pay MRF an annual amount equal to a portion of the unfunded obligations of MRF. The law requires the Treasury to make the payment in “Warrants” (

decidedly non-cash). The annual amount is calculated using a complex actuarial formula that is designed to eliminate 100% of the unfunded portion at MRS by 2026.

Over the past few years the actuarial assumptions used in the calculation have deteriorated. As a result, the annual cost of making the MRF whole is rising (up 6.5% YoY). In 2010 and 2011 "we" paid MRF $120B, but the amount of future payments we still owe fell by only $100B. The unpaid tab now sits at $1.3 Trillion.

These are the projected total payments to “cure” the unfunded portion from the prior reports produced by MRF:

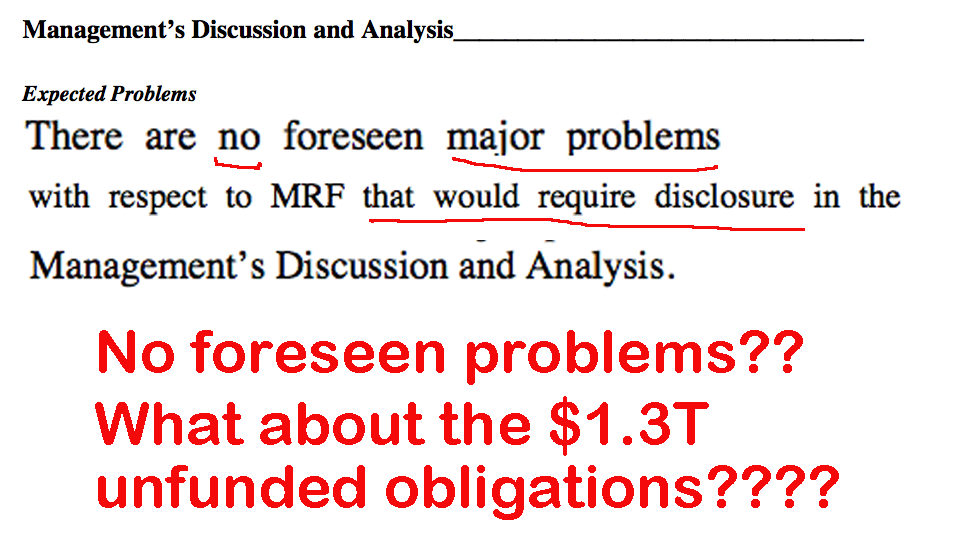

It gets worse. The folks at MRF are understating the future liability.

MRF invests its interest from Treasury securities. It needs a high return to offset costs. But it can't get a high return today, thanks to the Fed. The Board at MRF has set a ridiculous projected interest rate on its holdings of Treasury IOUs:

Consider the dog meat portfolio that MRF is sitting on:

There is no way in hell that MRF will get 5.75% in any year over the next five. I doubt it will realize that hurdle rate anytime over the next decade. This means that every year the unfunded portion grows and the annual warrant payment keeps getting larger. It could easily exceed $2 trillion over the next thirteen years.

The 5.75% hurdle rate is a significant flaw in the MRF's assumptions. They don't agree:

Some observations regarding the projected growth of the MRF and the asymmetrical treatment of the MRF versus FERS and SS:

+This is unfair.

Those dependent on SS or FERS do not have the legal protection that MRS has. How can this be? As the annual cost of protecting military pensions skyrockets over the next few years, there will have to be political fallout. This will be an interesting war: the Retired American People versus the US Military. Who will win?

+Turn this around.

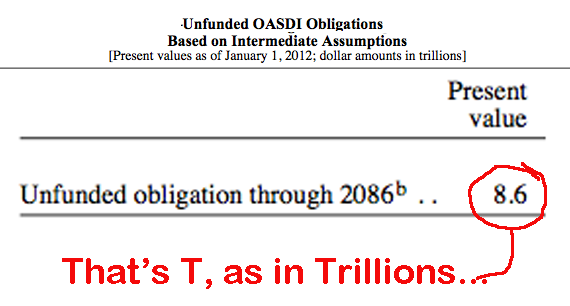

What if SS and FERS had the same deal that MRS has? The 2012 SS report to Congress established that the unfunded amount over the next 75 years is $8.6 trillion.

Assuming that FERS was in similar financial shape (it is), this would bring the combined unfunded amount to $10 trillion. If this number were resolved according to the MRF deal, the Treasury would need to issue $700B more warrants annually for the next fourteen years (not remotely possible). Total debt would race ahead faster then its current nosebleed trajectory. The USA would pass 150% Debt to GDP before 2020.

+Warrants are easy for Treasury to issue.

It doesn't have to find a new bond holder to make these payments. It just writes scrip IOUs. But the scrip comes due just the same as regular Treasury bonds. The IOUs owing to the TFs must be paid in cash. So the back end of the process hurts.

+The Disability Fund is cashing in its IOUs like mad.

The Old Age Fund started the process a few years ago, but an more modest rate. The retirment fund will have very big redemptions for the next twenty years. FERS will be hocking its IOUs at the same pace as SS. In about ten years, FERS and SS will be forcing the Treasury to issue mountains of extra Debt to the Public to meet the redemptions. At about that time, MRF will be sticking its hand out for another few trillion that the Treasury will have to borrow.

This is not about something that might happen in the distant future. It is written in stone, and coming in less than eight years.

.

Loading...

Loading...

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Posted In: Economics

Benzinga simplifies the market for smarter investing

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.

Join Now: Free!

Already a member?Sign in